Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the wordpress-seo domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /home/bcm/src/dev/www/wp-includes/functions.php on line 6121 pension | Zikoko!

One of the worst things you can experience as a Nigerian is trying to access the funds of a relative who died without a legal will.

I speak from experience.

My aunt passed away in 2020, and we’re still struggling to access her pension. It’s one reason I now advise anyone going for even the smallest medical procedure to get a probate-stamped document from a high court so someone else can access your money, at the very least.

But back to our struggle.

My aunt first became ill in 2017. She’d had a medical procedure which led to complications, leaving her bedridden and unable to feed without a stomach tube. She basically lived in the hospital for the three years that she was ill. And the bills? They ran into ₦1.2m weekly.

The illness took her job at a government parastatal, where she’d worked for 16 years. The government didn’t pay her hospital bills, and they made her resign after the first year. When the parastatal’s medical team visited and saw her condition, they decided they couldn’t keep paying someone who couldn’t work. The salary in question was just a little over ₦100k/month.

At my aunt’s place of work, you don’t just resign and go home. You have to submit clearance documents at several offices to update your employment status. I helped her husband with this clearance process — which took months. I thought that was stressful, until the real stress came.

When she passed away in 2020, we assumed accessing her pension of almost ₦6m would be straightforward. She and her husband kept no secrets; that’s how we knew about the pension in the first place. He also knew her passwords, and they even had joint properties. But there was no will, and that was the problem. Although he was the next of kin, he couldn’t access the funds unless a court gave him a document called a Letter of Administration. That was the first hurdle.

Getting a Letter of Administration in Nigeria can take as much as five years. You’ll need to hire a lawyer, pay them 10% of whatever property you want to claim, and then try to survive the many court delays.

You’ll also need two administrators for court approval: a spouse and another family member.

So, I stood in with her husband, as they didn’t have children. Fortunately, we had a well-known lawyer who fast-tracked the process, and we got the Letter of Administration after one year.

The next step was getting cleared to receive pension benefits from the government parastatal where my aunt worked. We had to provide pay slips, show evidence that she didn’t owe anything and meet several other requirements. At one point, we heard that the place where they kept some documents we needed for clearance got burnt. Again, we had people on the inside who helped fast-track the process, but even with that, it took another year to complete the clearance.

The bank runs came next.

The deceased’s account had to be changed to an estate account, so the administrators (her husband and I) would be signatories and be able to access the funds in it. This was the account where the pension fund would go. It took another couple of weeks to update the account.

With that done, we could now move to the pension fund administrator (PFA). But there was one thing standing in our way: The Nigerian government.

For individuals who work with private organisations, pension payment is straightforward. Your employer deducts the monthly pension from your salary and remits it to the PFA. For government workers, however, the pension is deducted from the salary but isn’t remitted to the PFA for years. So, you could have a pension account with a PFA, but there wouldn’t be money inside.

That was what happened to my aunty. When we arrived at the PFA in March 2023, they told us that PENCOM, the regulatory body for pensions in Nigeria, hadn’t remitted any pension fund to her account for the entire number of years she’d worked. The money was essentially in the air.

The only thing the PFA could do was write PENCOM, requesting the funds so they could pay us. They also told us that the payment could take as much as three years to come in. Apparently, PENCOM gives preference to retirees over the family of deceased pensioners.

At this point, we can only keep disturbing the PFA to send reminders to PENCOM. We’ve spent so much money and time on this in the last three years, and it looks like we have one or two more years to go. I’m tired and have accepted the possibility that it might even take longer.

I’ll say it again: Please go to any high court and get a probate-stamped document, indicating who you want your money to go to if something happens to you. The last I checked, it cost about ₦10k. Save your family the stress.

We’re celebrating the Nigerian culture of meat and barbecue with Burning Ram on November 11. Get tickets here.

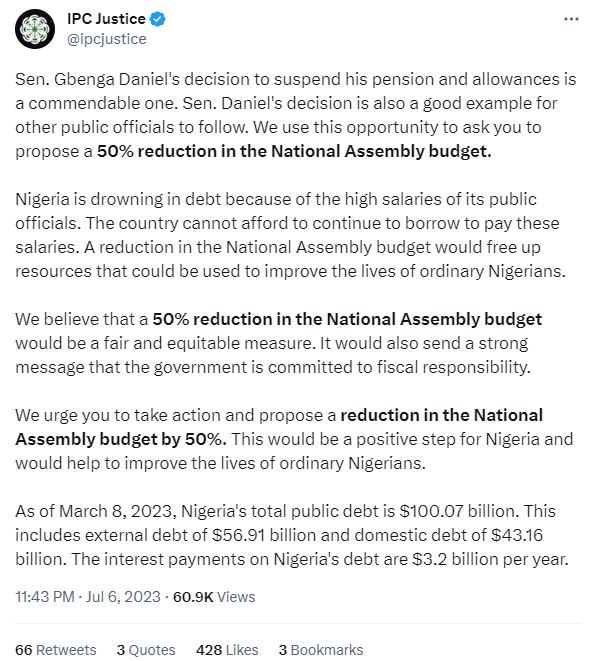

Last week, former Ogun state governor, Gbenga Daniels, made the news when he disclosed that he had written to his state government demanding that his allowances and pension as a former governor be suspended now that he’s a senator representing Ogun East district.

We’re always happy to call out Nigerian politicians when they misbehave. We are equally happy to commend them when they do the right thing. In a letter Daniels shared on his Twitter page on July 6, he revealed that his monthly payment was ₦676,376.95k.

What did the letter say?

The letter, addressed to the Ogun state governor, Dapo Abiodun, read in part:

“I write to request for the suspension of my monthly pension/allowances of 676,376.95 (gross) (Six Hundred and Seventy-Six Thousand, Three Hundred Seventy-Six Naira, Ninety-Five Kobo) being paid as a former Executive Governor of Ogun State.

The request is in compliance with my conscience, moral principle and ethical code against double emoluments that a serving Senator of the Federal Republic of Nigeria who hitherto was a former State Governor shall not be entitled to the payment of pension and allowances from such state.”

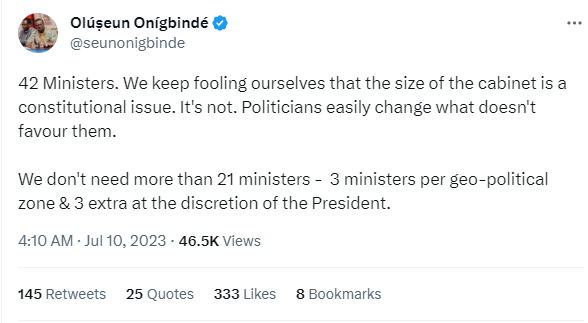

That said, there have been reports in the news that President Tinubu’s ministerial cabinet would have at least 42 ministers and 20 special advisers. This points to a bloated cabinet, which is sure to put a drain on the government’s finances.

Naturally, the current administration would argue that it is within the president’s right to appoint many ministers from across the federation, keeping with the federal character principle. Not many Nigerians agree.

It may be a long shot to ask the president to trim down his cabinet. However, he can consider cutting his wages and asking his appointees to make that sacrifice. According to the Revenue Mobilization Allocation and Fiscal Commission (RMAFC), ministers and cabinet members, such as the Secretary to the Government of the Federation, earn at least ₦650,136.65k every month. Ministers of state get ₦628,056.91k. However, this may not account for all of their allowances.

As a matter of urgency, the government should look to downsize. If others like Daniels are on double remuneration, it is unconscionable. Those politicians should toe the honourable path and have the extra emoluments terminated. The RMFAC should also be up and about plugging these leakages.

Kudos to Daniels, who has done an arguably decent thing. Other Nigerian politicians should take a cue from him. As citizens, you can tweet at your elected leaders asking them to move a motion to cut out double remuneration for former governors now in the National Assembly or reduce total pensions for ex-Governors.

During his presidential campaign, the president-elect, Bola Ahmed Tinubu (BAT), famously promised, among other things, that “farmers will make more money“. While he’s yet to be sworn in, another group of people — pensioners — have come to cash in early on that promise. Because what’s good for the farmer is good for the pensioner.

Pensioners in the South West of Nigeria under their union, the Nigerian Union of Pensioners (NUP), are demanding a 35% increase in their pensions. They’ve made this demand known to BAT and governors in the South West.

[Nigerian pensioners / The Cable]

What’s the gist?

At a meeting in Abeokuta on April 3, chairpersons and secretaries of NUP from Ogun, Oyo, Ondo, Osun, Lagos and Ekiti states said they want BAT to “show them love”. The SW NUP zone’s public relations officer (PRO), Olusegun Abatan, said the outgoing president Muhammadu Buhari “has done quite a lot for pensioners.”

In December 2022, the National Pension Commission approved the increase of retirees’ monthly pension to take effect in February 2023. However, the NUP alleges that governors in the SW still owe retirees huge sums in pensions and gratuities.

What else do pensioners want from BAT?

An increase in pension isn’t all the pensioners are asking. They also want BAT to create a separate ministry dedicated to pension-related matters.

What’s the FG’s latest response concerning pensioners?

On March 30, in an unprecedented turn of events, the federal government, through the director-general of the National Senior Citizens Centre (NSCC) Emem Omokaro, said the FG would “create a portal to engage older persons who wish to continue offering services after retirement.”

The portal will go live this month, April. Omokaro said, “The aim of the collaboration is also to assist the centre to create an online portal that would engage older persons who are professionals in their different fields of endeavour to tap into their wealth of experiences.” There’s no rest for the wicked and the elderly.

As seen from their Twitter responses, Nigerians have not taken this news kindly.

For a generation that claims we are disrespectful, see what they want to do to their elders https://t.co/DfiUwJFdgl

With Buhari already set to leave office, the burden of responsibility on this matter falls on BAT. Will he create a new ministry for pensioners? Will he send retirees back to work to “make more money”? These are questions only time can answer.

The topic of how young Nigerians navigate romantic relationships with their earnings is a minefield of hot takes. In ourLove Currency series, we get into what relationships across income brackets look like in different Nigerian cities.

Image Source: Unsplash (Actual interview subjects are anon*)

After 30 years at the bank, Mr Patrick* retired in 2014 and moved into his house in Warri, Delta state. He shares what led to his early retirement, how his friend ghosted him after an investment deal and putting his children through school on an epileptic pension supply.

Occupation and location

Fabric trader in Warri, Delta State

Average monthly income

It’s hard to say because the market isn’t fixed. But he gets about ₦30k in a bad month — which has been the case for most of 2022 — just enough to reinvest in the business. The only money he’s sure of is the ₦51k pension he receives every month and ₦588k in rent per annum.

Monthly bills and recurring expenses

Feeding: ₦40k on average. His wife assists with this most times.

Fuel: About ₦20k, subject to the frequent hikes in fuel prices.

Data: ₦5k

Transportation: ₦13k

Electricity: ₦6k. His two tenants jointly contribute ₦4k to the bill sometimes.

Savings: ₦15k

How did you meet your wife?

It was in 1992. I was ready to settle down, and a relative knew someone they thought I’d be interested in. I reached out to her. After a year of talking and getting to know each other, we got married. We’ve been married for over 27 years now.

How were your finances at the time?

I was a bank worker for a long time, in different roles with different pay, so I can’t remember. I do know that in 2008, my salary was about ₦135k. The naira was still good then, so I had enough savings from that to buy land in three different areas.

How much did the lands cost?

I got one for ₦1.8m and the others for about ₦350k each in 2008. But I’ve had to sell two of them — one in 2015 for over ₦2m, and the other for ₦3.5m in 2017. Oh, I forgot about the land on which I built the house we currently live in. I got that for ₦600k.

Why did you sell the other two?

In this Buhari’s Nigeria? I had three kids in the university, and with the bank retiring me two years early, I had to look for a means to survive. Retirement age is supposed to be 60 years, but mine came at 58 as punishment for a fraud case I was associated with in 2014.

I was the operations manager, and the head of funds transfer embezzled a lot of money using my password. We were close — family friends even, so it would never have crossed my mind to suspect him. It wasn’t until the internal department in charge of records went through the books that they discovered ₦4.4m was missing. The money had been taken in bits stretched over a year. When they traced it, the evidence led to us. They arrested both of us, but I was let go after he confessed that he did it on his own.

Why were you still retired?

For allowing someone else use my password. So while he was sacked and had to refund everything he stole, I was retired early and stripped of ₦3m worth of incentives.

How did your wife react?

I’m blessed to have a partner as understanding as her. And my kids are really great too. Everyone understood money wasn’t as available and adjusted. My wife is a businesswoman — she sells clothes — so she had to heavily support the family during the two years that followed. When our second child gained admission into the university in 2015, things were really hard, and she had to sell her gold necklace to assist with the fees.

How was life post-retirement?

It came with its challenges. In May 2014, I decided to invest ₦2m in my friend’s fuel station, and he was supposed to pay me ₦150k monthly for three years. Less than two years after we started, he fell ill and had to travel out of the country for treatment. I understand it cost him a lot of money. But the money stopped coming in even after he came back.

Ah. Why?

He kept saying business was bad and there was no money. When I noticed he was avoiding my calls, I travelled to meet him in Edo state. Sometimes, after plenty begging and chasing, he’d send some money. He became a prayer point in my house.

Did you have a contract?

Yes, we did. But I couldn’t involve a lawyer because everyone knows going to court costs money I didn’t have. So I let it go. I don’t hold any grudges. Like a few months after the bank incident, my former colleague reached out to ask for forgiveness.

What do you do now?

I run a fabric business. When I started in 2016, business was good, but with how bad the economy has been, my business has suffered greatly. People are working hard just to make ends meet, so they’re not thinking of getting new fabric. Sometimes, I go a week without selling a thing. Still, I open shop Monday to Saturday just in case a customer comes. Some months, I could get orders to supply a friend for an event, and the profit would be about ₦50k – ₦70k. Part of the money goes back to the business and shop rent at the end of the year.

And your wife?

She still sells women’s clothes from home. Most of her customers are either regulars turned friends or are referred by friends, so they meet up at our house when she has new stock. When they’re not buying on credit, they pay the money in small bits like they’re paying for crayfish. According to her, she makes about ₦80k – ₦100k profit on ₦200k stock. She used to get a ₦28k monthly pension, but that stopped coming about two months ago.

Why?

Do we know? When the money comes, we rejoice; when it doesn’t, we’ll be fine.

Besides housekeeping, how do you spend on relationship sturvs with your wife?

I buy her catfish barbecue. It costs about ₦3k, and she really enjoys it. So I get it on birthdays or give her between ₦5k – ₦20k to buy something for herself when I make good sales at the shop or whenever money enters my hand from rent or cash gifts. We go out sometimes, but it’s mostly with other married friends, so I spend less than ₦15k.

That’s nice. What does your wife do for you?

On birthdays, she cooks like it’s Christmas — rice, chicken, drinks for the house. My 60th birthday though, she also got a cake and invited our friends over. When I asked how she funded everything, she said the kids helped.

So you don’t really buy gifts for each other?

When things were better, she’d buy me perfume, a watch, clothes or whatever she thought I needed. Even then, I mostly gave her money because she’d rather buy what she wants by herself.

Do you have joint investments or accounts?

We’re very transparent with our finances, but we’ve never tried to put our money in the same place. The only thing we do that’s close to a joint account is our monthly osusu with a couple of other people. We contribute ₦15k each.

What about your kids?

They’ve long graduated from school and are working now. They don’t ask for money. Maybe it’s because they’re doing okay for themselves, or they don’t want to stress us. But they even send us money. This year, they put us on some sort of monthly allowance — sometimes ₦30k, sometimes ₦50k. It helps around the house.

Do you have a financial safety net?

Not exactly. I still have two plots of land in Warri and family land in my village. But that’s all.

What’s your ideal financial future?

Future? At 63 years old, it’s hard to have plans for the future. I hope both our businesses pick up, my children become successful in their careers, and the economy becomes favourable for us to afford more land, vehicles, and investments.

If you’re interested in talking about how money moves in your relationship, this is a good place to start.

Parents relying on their kids for money is a regular thing, but we don’t really talk about the effects of having such a responsibility.

In this article, seven Nigerians speak about what it feels like to be the ones providing for their families while also trying to take care of themselves.

“I’m happy to help, but I sometimes feel resentful”

— Amaka, 30

Sometimes it feels like the only thing I’m useful for in my family is sending money. I’ve been paying black tax since I started NYSC in 2014.

My mum used to work in a federal government parastatal but got retrenched in 2007. She managed to put me through secondary school somehow till I finished university.

Now, I send money to my mum, two siblings and cousins who stay with us for their upkeep every month. Asides from that, my mum also randomly calls and asks for money. It got so bad that almost all my income was going to family expenses, both necessary and unnecessary. Having to spend my money on family consistently sometimes makes me feel resentful. Other times, I’m happy to help.

My mum has a pension, but the money she gets is very small. The pension fund administrator has even refused to pay them for the longest time. So I’m all she has.

“I feel some financial strain, but it’s a privilege”

—Ebuka, 29

I come from a large family of seven children, and we collectively cater to our parents’ needs.

My dad lost his job in 1992 and couldn’t get stable work afterwards. My mum worked for over twenty years in a Chinese firm until the entire family was forced to flee the north during the Sharia crisis in 2000. So we returned to our village in Imo state.

As time passed, we kids got different opportunities that took us out of the village. My oldest brother made enough money to build my parents a six-bedroom house.

My siblings and I stopped my parents from doing any work three years ago [2019] so that they could rest. Now they depend wholly on us. We’re a large family, so the financial burden isn’t that much. We pool funds together to send to them.

I feel the financial strain once in a while, especially when we have to contribute towards paying for my dad’s medical bills. But I shrug it off. If my parents had a pension, it’d have given us less to worry about and more to spend on ourselves. However, we consider it a privilege to do what we do.

“How am I paying for someone else’s mistake? It’s so frustrating.”

— Aduke*, 56

I’m retired, but instead of me enjoying my money, I spend it taking care of my also retired younger sister.

The difference between both of us is that I have investments and a pension, and she doesn’t. This is because she finished her money on jaiye lifestyle. My sister was a woman of enjoyment; she was either always attending a party or throwing one. And each time, she had to sew an outfit for each party. She liked the finer things of life, and she wasn’t afraid of spending money on them. Now, look at what that has caused. She’s broke and relying on my money to survive. She has a child but can’t ask him for money because he’s in secondary school. I pay his school fees.

How am I paying for someone else’s mistake? It’s so frustrating. And I’m stuck with this for the rest of my life.

“Maybe it’s the pressure of being the firstborn son, but I feel the need not to let my parents work”

— Anthony, 31

As the firstborn son, I feel a certain responsibility to take care of my family. My parents don’t ask for money, but they expect it. Very subtle signs show that they rely on me to provide for them.

I get paid decently as a logistics manager for a start-up oil and gas firm. It allows me to send money to my parents monthly. My youngest brother, the last born, is now in university, and I send him pocket money too. There are times when I’ve had to come through in significant ways. There was a time my mum had surgery, and I contributed 80% of the money. My dad recently fell seriously ill, and I had to buy drugs that cost ₦53K every month for six months.

Maybe it’s the pressure of being the firstborn son, but I feel the need not to let my parents work. They sacrificed so much to send me to the best schools. The best I could do is spend part of my money on them.

You have no idea how many times I’ve asked God, “Why me?’”

— Shelia*, 35

My mum has chronic heart disease. This means my salary is spent on consistent hospital bills and drugs. Since my mum is sick, she obviously can’t work, and she doesn’t have investments or any other source of income that could, to some extent, make things financially easier for us, it’s all on me.

My dad passed ten years ago, and I’m the only child. So I’m the only one handling such a huge responsibility. My extended family tries to help out once in a while, but that’s not enough. You have no idea how many times I’ve asked God, “Why me?” Why did I have to get stuck with a sick mum? Why does all my money go to her sickness? I’m tired of it all.

Right now, I just want a higher-paying job so that I can at least be able to get myself some nice things.

“I rarely do things for myself because I earn the most in my family. It’s tiring.”

— Abraham, 27

I get paid about ₦350,000 per month, and I barely get to enjoy any of the money because I’m spending it on providing for my family.

Both my parents are retired, which means I’m responsible for their upkeep and that of my siblings. I’m currently paying the school fees of the last child who’s still in uni. My two older siblings can’t contribute as much because they don’t earn enough. I’m the one my parents call whenever they need money for one thing or the other. Sometimes my older siblings call me too.

I need a break from it all. I wish I could just travel to a really far destination and not think that I’m financially responsible for my family at such a young age.

Having your family members rely on you financially can be a lot of pressure. It can also be emotionally and physically exhausting. But what if you didn’t have to do it all on your own?

Leadway offers simple financial services products that protect you and everything you care about. From your personal belongings to your health, your life, and your future. Sign up on Leadway to learn more and get started.

With the 2023 elections drawing closer, I wonder what it was like to live in a time without democracy. In this article, a police officer who lived through the first military coup in 1966 shares the moments that led up to joining the force at 18 and the moment that reminded him there was more to life after 35 years of service.

The life of an Igbo police officer in the ‘90s, as told to Ortega

Life before the first military coup in 1966

I was a restless child born in 1937. I grew up as the only son of my father, and his brothers expected me to take up his role as our village’s chief priest. But my father wanted something more for me. He wanted me to go to school and live outside the cage tradition had built for our lineage as its custodians.

My father was convinced living together would make it easier for my uncles to persuade me. So he kept me away for as long as he could. When I was five years old, I had to live with different people in my village and depend on them to put me through school. They called me Nwali, son of the soil. It meant I belonged to everyone in my village but to no one at the same time. The villagers were in charge of taking care of me while my father kept my uncles at bay. Their generosity got me a secondary school education. But that was as far as I could go with the resources they had.

“They called me Nwali, son of the soil”

Everyone expected me to become a teacher, but I found the role quite stuffy and boring. I spent the two years after secondary school working odd jobs instead. I tapped palm trees and helped families build houses — I did anything I could get my hands on. I saw my father once in a while, but he expected me to figure things out on my own.

At 17, I decided to leave my village in Delta for Benin. My cousin promised to teach me to drive and offered me work as one of his cab boys. The first three months were okay, but I couldn’t bear the long hours of driving just to have my cousin take most of the profit I made. I couldn’t tell him that because I had to be grateful to him for trying to help.

After another three months of yelling for passengers under the hot sun, I decided to take a break and go back to Delta. That’s when I found a bit of luck in my life.

On my way to the park, I met a friend who was coming in from Delta. We exchanged pleasantries and I explained why I was heading home. His response to my complaints of driving taxis for hours under the sun was an odd demand for me to follow him on an errand in Benin. He offered to cover the two pence it would cost to get a bus back to my village, so I decided to go with him. There was nothing to lose.

The errand turned out to be recruitment at the police college for new constables in 1955. Of course, I was surprised my friend wasn’t just upfront about it, but I was more interested in how to get in as well. So while he queued up, I rode a bicycle back home to get my documents. Hundreds of people were in the queue when I got back. Every young man wanted a chance to wear fancy uniforms and work with white men. I just needed money.

“I refused to learn Yoruba. I felt it was easier to handle thieves that pleaded for mercy if I didn’t hear anything after e jo”

When it finally got to my turn, the constable took one look at my file and asked me to leave. Apparently, 18 was too young to serve. But then, luck was on my side. One of the senior officers asked him to consider me because I looked strong. And that’s how I got into the ranks.

There were only four police colleges in Nigeria at the time. Benin was just a point of recruitment, so I was moved to the one in Kaduna for a while before I was relocated with other southern officers to Lagos in 1956. I can’t remember how much I earned, but we were paid in pounds until 1973 when naira notes were introduced. What I loved about my job was the respect it gave me. No matter the rank, there was some kind of honour you felt putting on a police uniform in the ‘60s. There was also a lot more investment in the force. I attended the Police Colleges in Paris and Britain for short courses, and in a year, I rose to the rank of cadet.

I worked in Lagos until 1959. A senior officer decided it was best to experience other parts of the west. And in 1959, the country was still at a point when a mid-western Igbo (Igbos from the Bendel region) man transferred to Lagos or Abeokuta wasn’t odd. Nobody cared where I was from or that I refused to learn Yoruba. I felt it was easier to handle thieves who pleaded for mercy if I didn’t hear anything after “E jo”. I didn’t believe Yoruba people were open to learning my dialect. But it didn’t matter. No one bothered too deeply.

Abeokuta was a lot calmer than Lagos. I was stationed there to monitor the railway stations. We derailed passengers coming in from the north and monitored the day-to-day running. But after two years, I got bored. I liked the rush of Lagos more, where things like welcoming renowned leaders happened. For instance, in 1956, I got to see the Israeli prime minister, David Ben-Gurion.

“It wasn’t until the first military coup in 1966 things changed. The attack happened the day I got married in the village.”

Working at the police station in Lagos let me meet people from different works of life. And that made my work interesting. Like the time I met a gambler who was brought in from Obalende back in 1956. He was charged as a thief, but he didn’t seem like one to me. I was in charge of the evidence desk, so I could probe a bit more when criminals came in.

When we spoke, he mentioned that he ran away from home and was trying to win bets to make more money. But the men who arrested him didn’t believe it. He confessed to stealing clothes the morning of his arrest, but that was it. For some reason, he seemed genuine, and I believed his story. I spoke to my colleagues and we got him off on a two-week sentence rather than a year for petty theft. Those were the moments that made me feel like my job mattered; even the bible says blessed are the peacemakers.

The year everything changed

It wasn’t until the first military coup in January 1966 that things slowly began to change. The attack happened the day I got married in the village. For the most part, civilians were safe. But because the attack was by southern soldiers, Chukwuma Kaduna Nzeogwu and Emmanuel Ifeajuna, it looked like the Igbos were trying to disrupt peace. I knew better than to share my thoughts with colleagues; people were upset.

I was moved to Lagos to serve later that year. They began to look at me as a police officer who was Igbo rather than just a police officer.

As a corporal and the only breadwinner of my home, I knew better than to get involved in the messiness of politics. My main priority was keeping my family safe while my wife was expecting our first child.

The second attempt at taking over the government took away the last shred of peace. It was in August 1966, and officers called it the revenge coup. Unlike the first coup, which was handled mainly by southern officers, this operation seemed like retaliation from northerners because it was led by Lt. Colonel Murtala Muhammed.

Unlike the first, this takeover was successful, and for the first time, we lived under military rule. It was a very difficult time depending on your tribe. For me, it suddenly meant something to be an Igbo man serving with the Lagos police force. Some superior officers checked our badges and their countenance changed when they found out I was from the south. But I wasn’t going to buckle under the sudden pressure.

“When we lost the war in 1970, Nigeria went into a long period of discrimination”

Back home, people were being slaughtered. Trains were loaded with dead bodies in the east, and when Lieutenant Colonel Ojukwu decided to push back in 1967, so did the ruling officers. It was a bloodbath, and I still don’t know how Lagos maintained some sense of sanity. Still, by 1968, I had to send my family back to Delta state from Lagos.

I’d become a sergeant by the end of 1966, and it was business as usual at the force, which meant always being away from home. But I’d had my second daughter and wasn’t comfortable with working all the time when things were so unsafe. I also couldn’t get any of my wife’s sisters to travel from Delta to Lagos because of their safety.

It was better to take my wife and kids to Delta dressed in my police uniform, which was the only thing keeping me from being harassed or outrightly killed. It was a hard decision, but keeping them away was for the best. Our village didn’t experience the attacks going on in the eastern towns.

Between 1967 and 1970, Nigeria was at war with itself. But I didn’t have the time to process what it meant at 30 years old. I had to focus on my task of training police officers, assisting to keep some level of sanity in Lagos.

When we lost the war in 1970, Nigeria went into a long period of discrimination. Rising to the top of the force suddenly became difficult. I should’ve officially been promoted to sergeant, but the results for the exams I took weren’t released until after a year. Most people had theirs a few weeks after the exams. That’s when I knew a lot was about to change for me.

By 1975, I’d made a life for myself in the Ikeja barracks. My marriage was what you’d call successful because my wife and I had five children at that point. What hadn’t been so successful was my ability to support my family on my salary. I was earning less than ₦20k as a sergeant, and a family of seven wasn’t exactly cheap. But I wasn’t the only one experiencing the economic challenge.

“When my friend, a fellow officer, died from high blood pressure, I realised there was more to life than chasing ranks”

Leaving behind the police force

With the political instability, getting goods was hard and prices went up. I could get Omo for less than ₦5 before the coup, but after, we were spending almost ₦20 per sachet. Rice was also a luxury because importing was difficult. My wife eventually had to open a store to sell drinks so she didn’t have to depend on my salary for foodstuff. But I didn’t care about the money. I wouldn’t have enjoyed any other job as much.

As the years went by, I began to feel like my work as an officer didn’t matter. My family joined me in Lagos again in 1971. The Civil War was over, and I missed seeing my family. I’d had my second child in 1968, and we only saw a few times a year because of the state of things. So I brought them to join me at my flat in Ikeja barracks.

I spent years leading up to the final coup in 1975 as a sergeant. I was in the office with a few personnel who talked about setting a village close to mine on fire. I’m sure they didn’t have a clue where I was from. But that’s how ruined we were as a country after 1965. At least, the failed 1966 coup was just a power struggle, but the rest were about personal dislikes amongst ourselves.

As long as the ruling party preferred a certain ethnic group over mine, even as an Assistant Commissioner of Police (ACP) in 1983, I dealt with unwarranted questioning and didn’t get the recognition I deserved. But I was convinced I needed to rise the ranks to be a commissioner because it would make a difference.

Then one of my friends, a fellow officer, died from high blood pressure, and I realised there was a lot more to life than chasing ranks. I was earning around ₦80k as an ACP in 1986. I decided to start putting money aside to build a home for my family in Delta. As the only son, my father left over 500 hectares of land to me. That was enough for a farm and properties to rent out over time.

“I don’t regret my time on the police force”

Major General Babangida was still in power and the force was dominated by western and northern men. I could count the officers in my rank who were from the south on one hand. But I didn’t have the time to feel bitter. I put in my notice for retirement in 1989 and was approved for pension within six months. I left in 1990 at 53 without looking back.

It’s been 32 years since and my monthly pension hasn’t changed. Less than ₦80k per month is all I’ve gotten since 1990 while my retired colleagues from the army receive a minimum of ₦150k per month. I was one step away from the highest rank in the force, but I can’t get decent money for 35 years of work. That’s the biggest pain for me. It shows policemen aren’t as valued as we were in 1955.

But I don’t regret my time there. I’d do it all over again if I could because being on the police force gave me some of my greatest memories. Being an officer was a time I got to see the real side of human nature because of the amount of history I saw unfold. And now that I spend most of my time alone, it’s nice to remember what life was like when I was a young man.

Now that we know what life was like for a Nigerian police officer in the ‘60s, imagine what would’ve happened if Abacha Never Died.

Brands tend to reward customers occasionally or show appreciation to loyal customers every now and then. This is not the case with the good people of Stanbic IBTC Pension Managers as they never miss an opportunity to appreciate their customers.

The brand believes that loyal customers should be appreciated at every given opportunity, hence the recently launched “UMatter”, a customer loyalty campaign aimed at providing customers with the opportunity of getting discounts when they shop at partner-merchant locations.

The Umatter initiative described by Olumide Oyetan, Chief Executive, Stanbic IBTC Pension Managers as one of many to come, is geared towards rewarding loyal customers of Stanbic IBTC Pension Managers for their patronage over the years as well as support their lifestyles. Olumide stated that the Pension Fund Administrator (PFA) has over the years remained committed to ensuring the wellbeing of its customers through the provision of bespoke products and services that meet not just their pension needs but also their financial and lifestyle needs.

“Right from our entry into the Nigerian pension industry, our customers have continued to demonstrate unimaginable level of loyalty which has contributed to our success today. It is only fair that we express our profound gratitude to them by appreciating them for their long-standing support through this loyalty programme.

With over 1.8 million customers, we remain committed to supporting and rewarding every customer, as they remain the centre of our business. With UMatter, customers stand a chance of getting discounts ranging from five to twelve percent at various merchant stores, using their e-loyalty card. These merchants include Maybrands, Café Royale, Addide, Chocolate Royale, La Campagne Tropicana, Physio Centers of Africa, Medplus, iStore, Launderland Drycleaners, Artdey, Skit stores, HOG furniture, Oriki Spa and Active Leisure”, he said. “The list keeps growing as we continue to partner with more stores” he added.

The UMatter loyalty programme is open to all customers who have their retirement savings account with Stanbic IBTC Pension Managers. These discounts can be accessed by presenting your ‘E-loyalty card’ at the checkout point of the store. The card is accessible to all customers via the Pensions portal of the PFA’s mobile app.

For prospective customers missing out on these rewarding benefits, they can take advantage of the transfer window to sign up with Stanbic IBTC Pension Managers for eligibility to enjoy these discounts as well.

The Transfer Window provides the opportunity for customers who have retirement savings accounts with other pension fund administrators to make a switch to Stanbic IBTC Pension Managers where the safety of their funds is guaranteed. For more information visit www.stanbicibtcpension.com or call 01 271 6000.

If you get up to 15 on this quiz, you’re either a pensioner already or you’ll start collecting pension soon. You probably have a grandchild somewhere sef.

Nigerians treat money like knacks; they want a lot of it, but won’t be caught talking about it. Every week, we ask anonymous Nigerians to show us their Naira Life – some will be struggle-ish, others boujee–but all the time, it’ll be revealing.

(Shout out to Refinery29’s Money Diaries for the inspiration.)

First in line is a family man who believes he’s a diehard team player.

Age: 37

Occupation: Financial Analyst

Location: Lagos

Relationship Status: Married (with two kids)

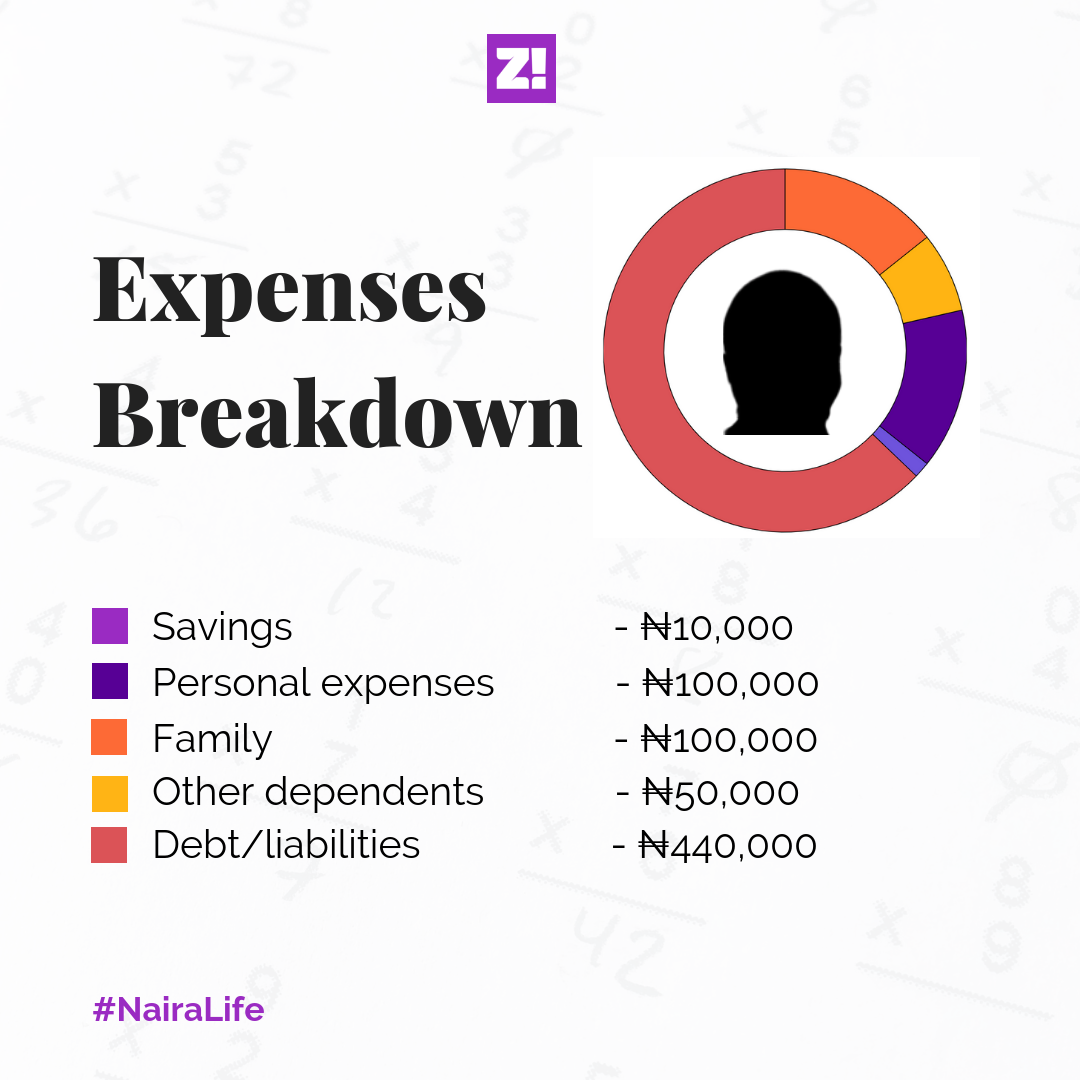

Salary: ₦700,000 (net)

Household income: ₦700,000

Rent: ₦750,000/year

What was the first salary like?

I mostly spent on people; family for the most part. I was quite traditional about it. I remember sending all of it to my mum as a gesture, and her sending it back to me. My net income at the time was ₦182k, and my annual package was ₦2.8 million. That, of course, includes bonuses and all of that. Also, this was 2010.

Less than 2% of your income goes into savings?

Yes, and that’s because the rest of my income goes into settling debts and other recurring commitments and liabilities. Also, I have this indiscipline of people asking for money and me not turning them down. Those 20 and 30k’s add up.

Investments?

None. I currently have no financial investments. I made some investments two years ago; they went bad, and I’m still paying for it. That’s where the debt came from. It’ll be completely paid in about six months though. For now, over 50% of my income goes into settling that debt.

What’s going to change about your spending when the debts are paid?

A lot more of it can now go to my family. Need to push up that family budget.

2019, almost 9 years since your first salary. What’s the annual package now?

My annual package is currently at ₦9.4 million.

How much do you feel like you should be earning now?

₦1 million. Net. I didn’t make some important switches in my career at the right time. Now, I believe you should move every 4 years max. I spent 7 years at my first job.

How much do you think you’d be earning in five years?

Using industry average, and where I currently am, I’d say somewhere between 1.5 and ₦1.8 million, net.

What do you feel like you should have had, but don’t have now?

Land. It’s just one type of investment I never really paid attention to. I just had a “never tie down capital” mentality. Most of my investments have actually brought me loss. Still, I’m not scared to take another risk.

Despite your bad investments, what are your best investments?

Definitely my certifications; the ICANs, ACAs, ACSes etc. When you work in an industry as structured as the financial industry, certifications help you stay competitive and valuable. Also, I’m kinda glad I got most of those certifications before I got married.

When do you want to retire?

You know, I used to think I’d retire at 45, but I realise now that I’m not a great businessman. It took a while to realise this, but I’m going to be working till the end, maybe 60. I’m the perfect company man; great energy, always representing, putting in the work for the team. I’m usually the person sharing impactful insights, and driving execution.

What’s your pension plan?

I don’t pay too much mind to it, but about 50-something-k goes into the pension account monthly. Currently, it holds no less than ₦4 million. It doesn’t make sense to me that I have that much somewhere–that is giving me about 7% annually but still–I can’t afford a house. I’ve done the math, and my pension is going to work best for me if I already own a house.

I imagine that the best use of my pension will be one where it helps me get a mortgage. I imagine a future where Pension Fund Managers in Nigeria create housing packages for consumers. If I have a ₦20 million pension and don’t own my house, I’m still screwed.

I inherited a mindset from my mum where I always imagined that I’d buy a house, instead of going through the trouble of building one. I was much younger, and that doesn’t seem so realistic now.

What are you long term plans at the moment?

I’ve been in debt for too long that it’s hard to see beyond it. At ₦700k, I can build a house in 3 years, because I really don’t have huge personal expenses. I’m just caught in the debt trap. At ₦700k, and with the responsibilities of family, I’d still be able to save ₦150k at least. In fact, 40% of my entire income can go into saving and investing.

What do you wish you paid attention to in 2010?

Discipline. I wish I’d began saving and investing early.

How would you rate your happiness on a scale of 0-10?

I’m really glad a lot of my happiness isn’t tied to my finances because I’d probably have high BP now. I’m totally fine. And while this might sound cliche, I have a family. I invest a lot of time in them, and it’s easy to underestimate how important this is for our future and mental wellbeing.

My head is still above water, and for that, I’m grateful.

Check back every Monday at 9 am for peeks into the Naira Life of everyday people.

If you’d love to share your Naira Life with us, tell us here. You’ll be anon, of course 🙂

1. You finally got that job, one million years after graduation.

Ope o!

2. You, when you see your mates still seeking employment.

I have arrived!

3. How you feel, when you get your first salary:

Rich gang!

4. When the oversabi 23-year-old girl in your office starts talking about pension.

Oversabi!

5. How you ball, as per, you’re not about that struggle pension life.

Pension ko, pension ni.

6. Until you visit the village and see your cash money uncle looking all broke and miserable like:

Wawu!

7. You, when you realize your uncle’s wahala is that he blew all his money without a retirement plan:

Hay God!

8. So you decide to be sharp and not play yourself because suffer-head is not your portion.

Before!

9. So you kuku start searching for correct PFAs online.

No time!

10. You, when your ARM Pension Funds start to look all nice and good.

YASSS!

11. How you sleep at night, knowing you won’t retire broke and miserable thanks to ARM pensions.

My future is safe!

Are you still wasting time? Don’t sleep in a keke, contact ARM Pensions to secure your future today. Click here to begin.You can also hit them up on Facebook and Twitter.

![It’s Taken Us Three Years [and Counting] to Access My Late Aunt’s Pension](https://dev.zikoko.com/wp-content/uploads/zikoko/2023/10/Will-1.jpg)