Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the wordpress-seo domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /home/bcm/src/dev/www/wp-includes/functions.php on line 6121 Investment | Zikoko!

So you mean no one is insulting another person’s daddy over a small disagreement? Where am I?

But you see “.eth” everywhere

Once you start seeing usernames that end with “(3,3)”, mentally take off your shoes and brace yourself. You’re at the entrance to crypto Twitter.

You don’t understand anything

Just know you’ll start seeing words that make no sense. You’ll scroll through your feed thinking “Wetin be FUD?” and “Which one is GMI again? Golden Morn?”

Everyone talks like they have money

It doesn’t matter that the market is down and everyone’s wallet is in tears. Once a rich person, always a rich person.

You start seeing “fiat” too often

On top of that, they constantly shade the paper money you still don’t have.

Memes… everywhere!

Nobody makes jokes like crypto folks. So, if you start seeing too many memes, you’re probably in crypto Twitter. Even if everything else vexes you, you can at least laugh at the memes.

They say if you can’t beat them, join them. To join crypto Twitter, you need to first own some crypto yourself. You can do this easily on the Luno app, which allows you buy cryptocurrencies like Bitcoin, Litecoin and Ethereum. Download the app and sign up to get started.

Is your significant other the best thing since agege bread or is it time to return to the streets?

These are surefire signs that your partner doesn’t mean you well:

They don’t brush their teeth first thing in the morning

Do we need to tell you that they’re trying to suffocate you with bad breath? Stay woke.

They brush their teeth immediately they wake up

Who are they trying to smell good and stay healthy for, exactly? Check the streets, your boo might be there.

They like pasta

If your partner has a taste for creamy pasta and its cousins, your account or your lactose intolerant bowels are in danger.

Their beliefs are questionable

If your significant other is already saying stuff like, “30+ women are expired goods,” “partners don’t need to know about each other’s finances” or “Semo is nice,” why are you still there?

They have to travel 6 times a year

Are they in a weird competition with Bubu? Your partner clearly has no other plans than to erase your account. Avoid them.

You’ve still not seen their apartment

They’re trying to show you that they live on the streets. You have no future there.

Their mantra is “I can’t kill myself”

They spend money anyhow and blame it on mercury and her lucozade. Do you really want to be with someone that discourages you from smart financial decisions and investments in this economy?

All you both do is watch TikTok videos

You: “Baby, I really want to learn more about real estate, Bitcoin and NFTs.”

Them:

They don’t listen to the “To Be Quite Honest” Podcast

If your partner hasn’t told you about this podcast, they obviously don’t mean you well. They talk about real estate, investment opportunities, social trends, and other stuff that’ll bring you out of poverty. It’s not every time food or movies, sometimes think about your future.

To Be Quite Honest Podcast is a fun and engaging stop for everything about real estate investment. Get updates on new episodes on Instagram via @tobequitehonestpod

MTN Nigeria recently announced the price of its initial public offering to retail investors.The offer which opened at 8:00am on the 1st of December 2021 will close at 5:00pm on the 14th of December 2021 with a minimum subscription of 20 shares and lots of 20 shares thereafter.

At the retail offer roadshow in Enugu which held recently, the Chief Executive Officer, MTN Nigeria, Olutokun Toriola expressed his desire to have as many Nigerians own a share of MTN thus benefiting from the growth of the company.

Here are five reasons to embrace this public offer and invest:

1. A compelling growth story

According to the CEO, MTN is offering shareholders both strong dividends and strong growth. Growth of the dividends and growth of the market price with consistent payout.

2. A well-managed company

MTN Nigeria is a company that is well governed, and very efficient at what it does. According to him “We are disciplined, we have a board of directors that oversee what we do, we have auditors that check that the money is where it is supposed to be. We have a group that also ensures we are providing the profit margins that are expected of us.

3. ”Here to stay”

MTN is not exiting Nigeria and will continue to remain in Nigeria. MTN Group thus wants more Nigerians to participate in wealth creation in the future of MTN. This is why the public offer of 575 million shares for sale is made available in this first phase of a sell down.

4. Well-positioned for the long term

MTN is the leading operator in solutions for small and large businesses, as well as financial services and digital services. MTN believes that everyone in every village deserves the benefit of a modern connected life and will continue to lead and drive digital solutions for Nigeria.

5. Incentive

The offer includes an incentive in the form of 1 free share for every 20 shares purchases, subject to a maximum of 250 free shares per investor. The incentive is open to retail investors who buy and hold the shares allotted to them for at least 12 months, post the allotment date.

Investors can submit applications through the issuing houses, receiving agents (authorised stockbrokers and Nigerian banks) and online via a unique digital application platform, PrimaryOffer, administered by the Nigerian Exchange Limited and can visit www.mtnonline.com/po for more information.

Crowdyvest Limited, a fast rising Nigerian fintech company which creates an all-encompassing financial solution from savings to investment, has re-launched its mobile app with new investment opportunities.

Currently available on the Apple and Google Playstore, the newly re-launched Crowdyvest mobile app has a very neat user interface which is easy on the eye, with both mobile and desktop versions showing no major difference. The funding process on the app is hassle-free and the app is also very easy to navigate on both desktop and mobile to deliver a seamless and enjoyable experience for its existing and prospective users. Speaking on the revamped mobile app, Tope Omotolani, CEO of Crowdyvest said “We aim to become the platform that helps our members plan and structure their finances through the different range of products we offer.

“As we work with organizations in different sectors to power viable and impact-driven projects through the funds we raise from our members, a symbiotic interdependence is created, leading to financial and economic growth for all. We believe this partnership is needed to foster growth and create more opportunities for Africa.”

The re-launched app has introduced a couple of new financial products which include the Crowdyvest Yield. The old app had only the Vault, pace and flex Savings products, Hyperplan investment product and Crowdyvest Tribe, a platform built on the foundation of community-driven savings and wealth creation, to drive collectivity and foster growth for individuals and businesses but the revamped version has not only included additional products, it has also grouped all Crowdyvest investment offers under one segment known as Crowdyvest Yield.

Crowdyvest Yield is a catalog of alternative offers that include commodity-specific projects and discretionary plans available to members ranging from short to long term tenors across a wide range of sectors. It consists of the HyperPlan – an impact-driven funding opportunity where users/investors can earn as much as 21% returns on investment, Project investment which is an alternative investment and commodity-specific type of offer in different sectors, in partnership with pre-vetted impact partners and many more. You can earn as much as 25% returns on project investments.

This new distinction will provide Crowdyvest users a variety of suitable plans to choose from as they build a savings and investment culture based entirely on their capability with product prices as low as ₦1,000 and returns up to 25% per annum. They also have a wallet that gives up to 3% interest per annum. You can share funds from your Wallet with friends and family who are Crowdyvest members, at no charge at all.

In addition to the upgraded features and newly introduced products of the app, Crowdyvest has partnered with UBA Global Investor Services Limited and Parthian Securities Limited; an investment brokerage firm licensed by the Securities Exchange Commission (SEC) to ensure proper fund utilization, transparency and compliance thereby assuring its users of the safety of their funds.

How It Works

On launching the Crowdyvest app you’re taken straight to the log-in/sign-up page where you’re expected to create a new account as a new user or log-in as a returning one. Once you click on the “create one” option, you’re instructed to choose between creating an individual or business account. The user is then instructed to fill in basic details like name, surname, password, username, email address, phone number, gender, date of birth and in the case of a business account information like business name, business date of birth is also required.

You will then be required to verify your account with a passcode sent to your mail. Once this is done, your Crowdyvest account is ready for use. You will however be instructed to fill in your bank details and create a 6 digit security PIN to carry out any financial transaction. Once you type in the name of your bank and account number, the name attached to that bank account (which is your full name) shows up. Your BVN is also required. This takes less than 5 seconds to be verified by the app. You are then required to create a 6 digit security PIN to complete transactions. Once the PIN is created, a passcode is sent to your mail to authenticate it and you’re now fully ready to use the Crowdyvest mobile app.

How To Navigate The App

Having done the necessary registrations, the account is now ready for use. On the homepage there is a column on the right of the screen with several icons on how to use the app. It includes: the homepage, portfolio, savings (vault, pace and flex), yields (hyperplan, project, etc.), deals and offers, transactions and profile icons through which new users can easily navigate their way through the app. The entire process takes less than 7 minutes, after which you can begin your journey to financial freedom via a seamless and hassle free online banking experience.

Investment in Nigeria requires common sense. If you ask people, they might tell you to invest in Cryptocurrency and all those kinds of things, but listen to us: THE SOURCE OF YOUR WEALTH LIES AROUND YOU. Everyday things are rising in cost. Why not buy and hold them as investment? Don’t worry, we will guide you through it. Here are 9 profitable things you can buy and hold as investment in Nigeria:

1. Maggi cubes.

Maggi was two for N5 in 2012, but now it’s one for N10 now. Who knows, you could wake up next year and hear that one cube of Knorr Chicken now goes for N50 per piece. Better buy the dip now before it rises.

2. Titus sardine.

Sardines are now hotcake, but Titus sardine is the hottest of them all. It recently attained a record high when it rose from N340 to N650 in less than one week. Bitcoin is shaking. You better buy and hodl now, so you can resell when it lands at N1k.

3. Egg.

You can bear me witness when I say eggs once sold for N25 per piece, four pieces for N100. Now, one piece of egg goes for nothing less than N80. Chickens are now laying the new Cryptocurrency. Egg-o-currency to the moon!

4. Gas.

Before we say anything, it is important to let you know that anyone who can afford to refill their gas these days is a ritualist. If they cook for you with that gas, you better not eat it. Maybe they want to collect your destiny and use it to refill gas. But please, investing in gas is one easy way to cash out these days. Do you know how much one kg costs now? You better buy and hodl now. Christmas is coming, you will make your money back. Just stay safe sha. Don’t let your investment kill other people. Their ghost will swear for you.

5. Onions.

Onions will soon start competing with gold. Two small pieces now sell for N100. And these are sizes that used to sell at N20 per piece. Can you see how wide the profit margin is? If you are lucky, you can enter into partnership with a caterer. Year in year out, you will just be cashing out. If we were you, we would even buy stocks for our unborn children with it.

6. Titus fish.

Like Titus sardine, like Titus fish. One piece now goes for N1k plus, and according to the investment analysts on Zikoko’s Wall Street, this is still estimated to rise higher. You better buy ice blocks and convert your bathing drum into a cold storage. Stock up Titus fish and wait. When the boom happens, even Dangote will be begging you to invest in his business. Dangote wey still dey find money.

7. Frozen turkey and chicken.

Frozen turkey is now N2,500, if not more. Frozen chicken is slowly climbing up to N2,000 per kilo. If after all our advice, you still don’t know that you should invest in it now, then we are sorry for you oh. Don’t you want to get rich?

8. Vegetable oil and palm oil.

If anyone is saying tech is the best place to make money, it is a big lie. Tech, when you can invest in vegetable oil and palm oil, and cash out big time??? Do you know how much one gallon of vegetable oil is now? BUY THE DIP NOW OH. BUY IT NOW. A lot of these tech people are surviving on investment returns from vegetable oil and palm oil. They are just using tech to cover face. If tech is as easy as they say, how come you have not made money after one week of UI/UX?

9. Cows.

If you need us to spell out how profitable this is for you, then you don’t know anything. Go and start your investment portfolio now. May the dip be with you. Sha don’t forget us when the returns come in. It’s not only Dangote that is still looking for money. Zikoko sef still dey find money.

While smart investing is a sure way to build and retain wealth, it can be a daunting prospect for beginners. In the same vein, it is a lot easier when you understand the various options in which you can invest and ultimately grow your wealth. Here are some options you can consider when taking the step to managing your wealth like a pro – explained in simple terms:

Treasury Bills

Treasury bills (T-bills) are risk-free, short-term investment instruments that are issued by the Federal Government through the Central Bank of Nigeria (CBN). It is a way the government raises funds from individuals and organisations. They are considered among the safest investments with attractive returns since they are backed by the full faith and credit of the Federal Government. In addition, the longer the maturity date, the higher the interest rate that the T-Bill will pay to an investor. Although T-bills yield a lower rate of return compared to other forms of investment, they offer safety and a predictable profit which makes them a good choice for long-term investments in your portfolio.

When investing in T-bills, it is important to take note of the prevailing rate and your expected returns upon maturity. However, if you decide to sell before maturity, you may incur a loss depending on the prevailing market value.

Fixed Deposit

A Fixed Deposit is a short-term investment that guarantees you a fixed interest rate when you keep funds for a specified period. The minimum tenor is 30 days and the maximum is 365 days – at the end of the agreed period (tenor), your principal and interest amount earned are paid to you. This product can also be used as security for cash-backed loans.

The ideal strategy for Fixed Deposit investments is to diversify and spread out your investments across various banks while striking the right balance between risk and returns. It is also important to note that if your Fixed Deposit investment is terminated before maturity, the total accrued interest not earned will be forfeited. This means that only the portion of interest earned during the period that your money was held is what will be paid to you.

FGN Bonds

Federal Government Bonds are long-term instruments issued by the Debt Management Office on behalf of the Federal Government of Nigeria (FGN). When you buy FGN Bonds, you are lending to the FGN for a specified period of time and the FGN is obligated to pay you the principal and agreed interest as and when due, meaning that they have no default risk. Not only do these bonds offer opportunities to investors willing to invest long-term but also attractive interests that are paid bi-annually (twice a year). FGN Bonds can be accessed through primary licensed dealers and before investing, pay attention to the prevailing rate, maturity, payment dates and expected returns so you can make an informed decision.

Commercial Paper

A Commercial Paper (CP) is a short-term unsecured debt instrument issued by financial institutions and large corporations with high credit ratings. As a short-term instrument, CPs normally mature within 270 days. CPs are issued at a discount, which means interest is paid upfront. CPs are more suitable for risk tolerance and before investing, you may want to do your due diligence on the issuing company and take note of its risk of default. This entails an evaluation of their credit rating, brand reputation and experience of the management team. While CPs offers a return on investment in 270 days or less, it’s paid at maturity, not periodically, like with FGN bonds and other similar debt securities. It may be wise to consider all of your investment options before investing in commercial papers.

Eurobond

Eurobonds are financial instruments denominated in a currency other than that of the issuer – for example, a Nigerian Eurobond is issued by Nigeria in U.S Dollars. Despite their name, Eurobonds aren’t necessarily denominated in Euros and can take many different forms. They are issued either by Governments or corporate institutions and are highly liquid i.e can easily be converted into cash, which is a key benefit of this form of investment.

Given that Eurobonds come as government and corporates, as a prospective investor, you have to decide which to buy. While corporate-issued Eurobonds may offer higher interest than government-issued ones, they also offer higher risk. Like every other investment, buying Eurobonds should be a well thought out process and it is advisable to review and understand the risk profile of any Eurobond that you are interested in buying.

Managing your wealth

Wealth management is personal and there’s no one-size-fits-all approach to go about it, which is why it is important to have the right knowledge and information.

Always start with a clear picture of your financial goals while understanding your risk tolerance. Once this is understood, diversify your portfolio with the mix reflecting your tolerance for risk. Understanding these investment options is essential, however, it is also important to rely on sound recommendations from experts while dismissing “hot tips” from unverified sources. While this can seem complicated, a good partner will make it simple – even exciting.

The digital investment app, M36, not only delivers a wide range of investment products, including those highlighted above, but also offers support by professional financial advisors to enable you make sound investment choices that suit your needs.

Download the M36 App from the Google Play Store or the App store today and pick Your Track to Wealth.

For many young Nigerians, investing is a very treacherous undertaking. Between the tanking economy and growing responsibilities, you might find it nearly impossible to set money aside for investing. I mean, things are so bad, Shoprite is shuttering operations after 15 years. No, I’m not crying.

Back to the topic. Investing is certainly a great way to grow your finances. While saving money is nice and all, investing is a much better way to increase your wealth. One of the reasons for this is compounding.

Compound That Monayyy

Compounding interest basically means earning interest on your interest. Let’s say you invest N50,000 in government treasury bills with an interest rate of 18% per year. If you decide to reinvest your original investment and all the interest you acquire, you will receive N114,387 at the end of 5 years.

Let’s assume you decide to be disciplined and continue reinvesting your principal and interest. At the end of 10 years, you will have earned 261,691.78. While this might not seem like a lot of money, it is a great way to let your money make money for you. If you add this to the fact that investing in government treasury bills is one of the safest ways to secure your funds, you really have nothing to lose.

If you’re like the average Nigerian, you probably just set aside money for saving rather than investing. The rest is for balling. However, investing should be separate from saving. Saving is great so that you have a stash of cash for emergencies and other expenses. However, you should invest to grow your entire financial profile.

No, Seriously, You Should Invest

You should keep in mind that the reason for investing isn’t necessarily to become rich but to create a financial safety net for yourself. At some point, due to any reason, you might/will stop working. Having an investment portfolio is a great way to secure your future against what Nigeria tends to do to your personal finances.

Working in Private Equity is quite the dream for many young people in Nigeria who have the kind of qualifications they’re looking for.

The subject of this story didn’t get in by chance. She’s 23, recently finished NYSC and has been working since the first week she completed her final year project in school.

She studied accounting but decided to pursue an investment banking career. She hasn’t looked back since.

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

Let’s go all the way back, like way, way back – you know, to your childhood.

I wanted to be a doctor – finding the cure for HIV was supposed to be my life’s purpose. Then, one day in SS1, my Accountant uncle was like “why don’t you study accounting. You can work anywhere,”

And that’s how I ended up in commercial class.

I pretty much knew that I could survive in any career path but I particularly liked accounting because it had a sprinkle of maths here and there

So, it wasn’t money, but in fact maths.

While it was a spur of the moment decision, it wasn’t a path that was uninteresting for me because there was math involved so I had fun with it.

Speaking of money, I love, love money.

Hahaha. About money, when did you first clock the importance of money, ever?

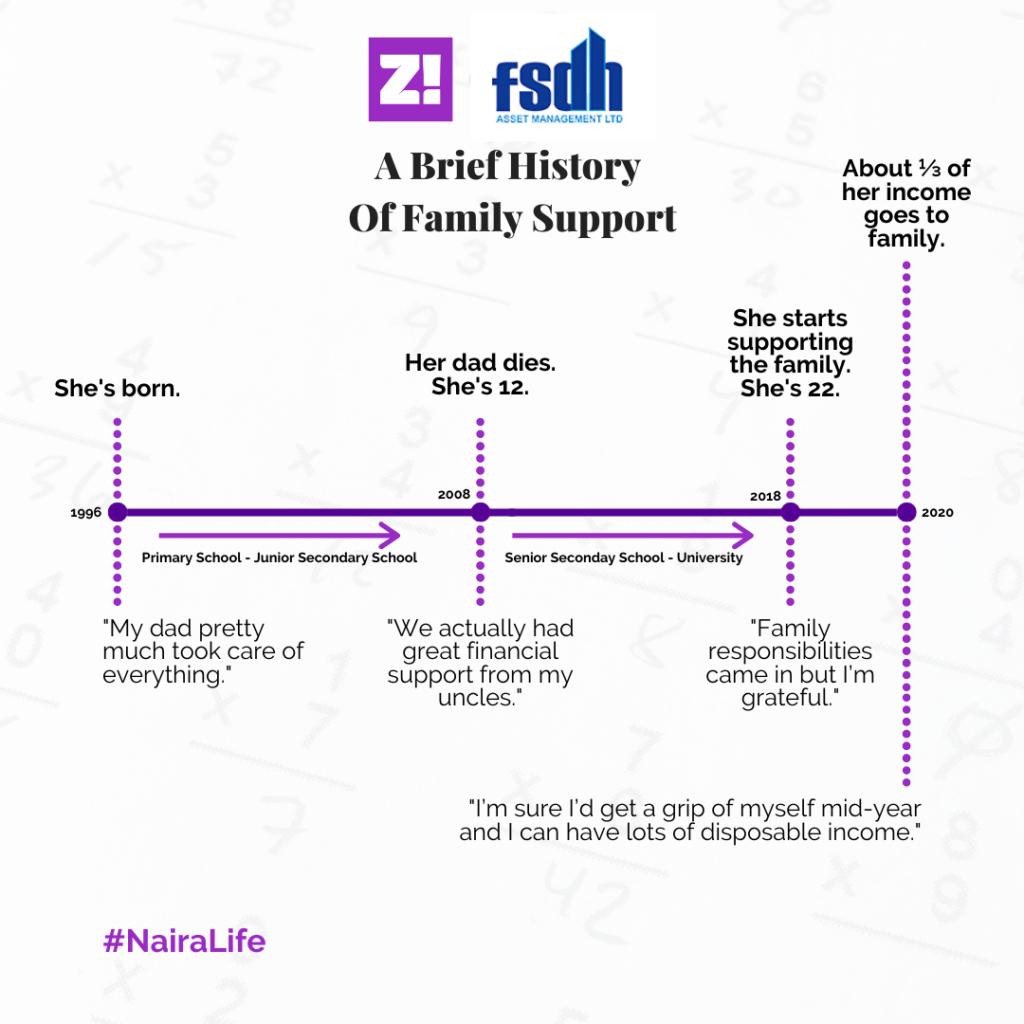

Look, I grew up in a low-income family. Three siblings and my mum – my dad is late.

I’ve always known that money is the koko. My sister and I have always dreamed of ways to get rich from a very young age.

Considering the fact that my dad died when I was 12, the hustle sort of intensified. Immediately we could navigate how to board buses properly we were on our way to building our Dynasty – that’s what we called it hahaha.

We pretty much have the ‘driven’ gene. It’s overwhelming.

And intense. Sorry about your dad.

Thanks. I was 12, about to write my Junior WAEC.

Must have been tough for you mum.

We actually had great financial support from my uncles on both sides of the family. One of them was the main sponsor – the person that pays for tuition and major bills.

That’s amazing. What’s the first thing you ever did for money?

I needed to go to prom in SS3 but we didn’t have enough money. My sister was a budding fashion designer and I was her model, so we made a sample prom dress. I took pictures and we wanted to show people the sample, so they can make their prom dresses with us.

We tried to go to one of the fancy schools – they didn’t make it past the gate, hahaha.

Hahaha. This is hardcore. Do you remember the first money you made though?

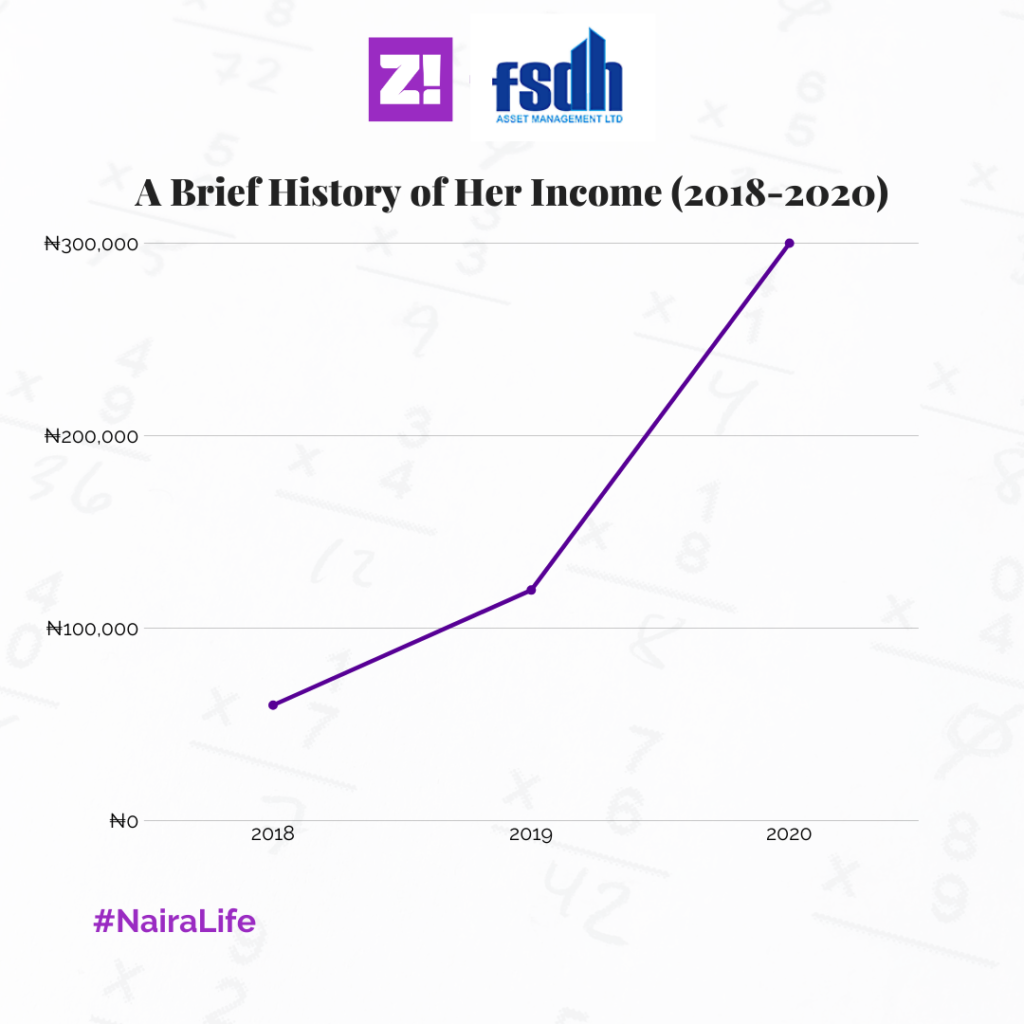

That’d be my first salary as a research intern at my pre-NYSC job. 2018. 60k.

Ah ahn, enjoyment.

Hahaha, not really. Family responsibilities sort of come in but I’m grateful. Anyway, I went on to serve at an investment bank in Lagos, and they paid me 100k a month.

I imagine these guys retained you.

They wanted to but I needed to work with a bigger company.

This energy, which market can I buy it?

Hahaha. I got a job working in Private Equity. I don’t know how long I’d be here but my little time here has exposed me to different businesses. In the near future, it’d be easier to run my business, if the time comes.

Interesting. What are your biggest WOAHs since you started working in Private Equity?

Considering that I’ve been here for a little over two months, the biggest WOAH has really been working for a company that not operating in only Nigeria. It’s strange but interesting understanding of other Anglophone African economies. For example, I never really cared about how the Ghanaian economy worked until I started working here so it’s quite challenging and interesting.

Unlike Nigeria, Ghana actually has an oversupply of power in its economy. Can you beat that?

You had to bring in electricity.

Haha! While the demand for electricity overshadows that of supply in Nigeria, the reverse is the case in Ghana. Now they have long term power contracts that they have to renegotiate so that the government doesn’t continue to pay for unused power.

Meanwhile, you are here, worrying about electricity and Okada bans. How has that affected you, by the way?

HORRIBLE. It makes me rant on my WhatsApp status every morning. One of my friends told me he fell ill and landed in the hospital.

Woah. I hope he’s okay.

Yes. The doctor just prescribed a drug called “Less Lagos Madness”

Hahaha. This is the funniest, not-funny thing ever.

It’s like I go to work with an open mind every day.

Questions like “would I get a bus?”, “how long am I going to wait for one?”, “how many people would I successfully shove trying to get into a bus?” My work colleagues can’t relate, I look like the crazy one

What’s your monthly income like now, and how does it disappear monthly?

300k net. One would think I’d have lots of Investments considering I’m a finance person but it’s not so. I have to write exams – ACCA and co. I also have to settle the school fees of my younger siblings. Currently saving up for rent. I’m sure I’d get a grip of myself mid-year and I can have lots of disposable income. Also hoping for a full-time role, from intern to an analyst.

Wait, are you an intern currently?

Yes. The way these multinationals work, they need to sort of see you work for a period before you transition into full time. It’s basically budgeted in dollars.

How much will you earn when you go full time?

I’m not sure. Wild guess? 800-1 million. It’s a year’s internship, but you can get a bump up earlier being a high performer.

I’m rooting for you.

Thanks.

It’s time to get our hands a little dirty in the nitty-gritty of your monthly expenses.

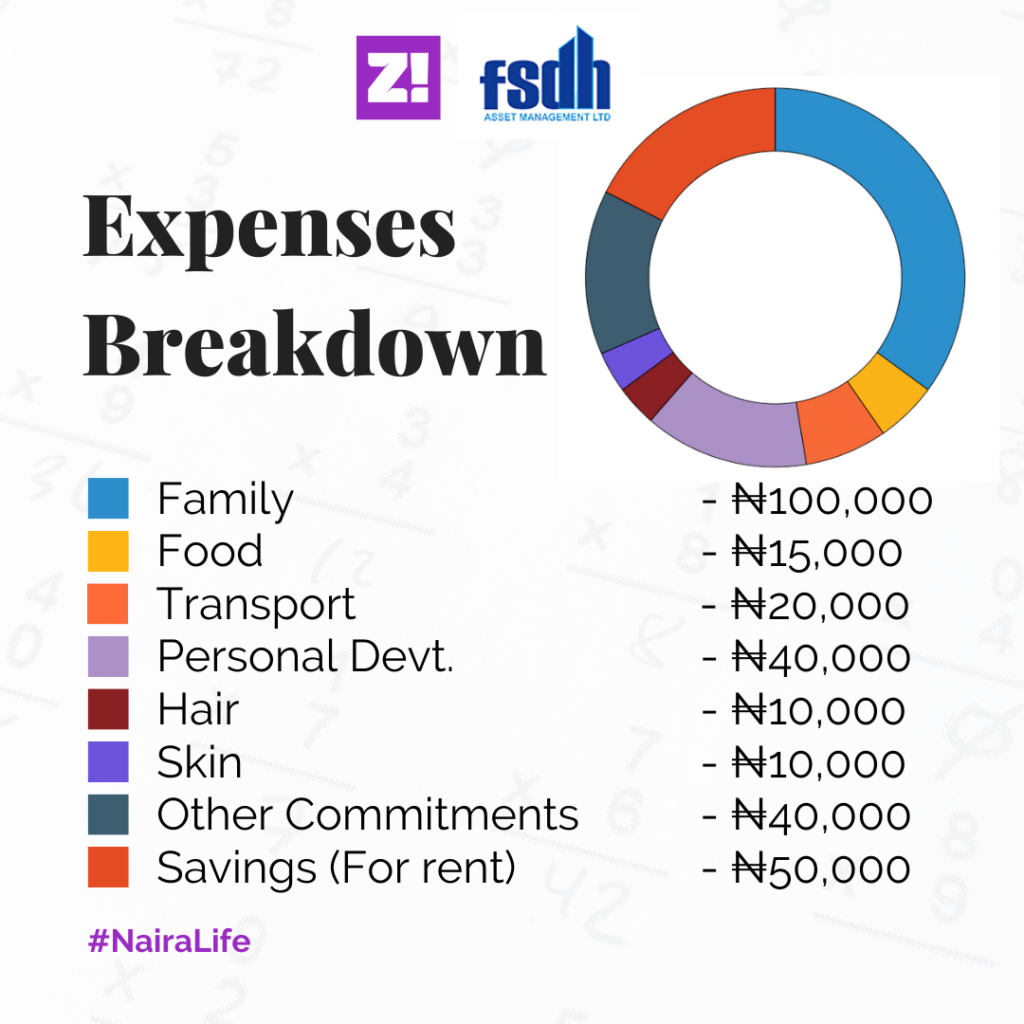

Let me explain the numbers. The family part includes monthly upkeep, part-payment for my sister’s school fees and brother’s school expenses.

Feeding is cheap because I try to cook. That transport part is definitely going up this month with this Okada ban. My skin and body maintenance is really cheap because I generally don’t wear makeup and all.

Being a girl is so expensive by the way, and I’m just doing the barest minimum at the upkeep department. That’s why I’m big on making more money and changing my life.

Tell me more about the upkeep part.

I mean, I don’t go shopping every other month, I don’t buy Vietnamese hair – at least not yet. No manicure or spa treatments. I don’t spend 50k on body oils and an extra 50k on fragrance. It doesn’t mean that I don’t like them but it’s not just time. Soon. I just need to stash good and smart.

The way I grew up has always made me approach things with a unique mindset, and it has worked to a good extent.

I see big things as very achievable. Like, “what’s the worst that could happen?” I have no problem banging on every dream company door if I need a job.

Interesting fact: Before I got this job, I wrote lots of cold emails to different companies’ CEOs. So I’m a big dreamer and intentional about creating generational wealth.

I’m curious, how much do you imagine you’ll be earning in 5 years?

With plan A or B?

Run me through both

This is very optimistic, but I want billions in annual revenue if I become an entrepreneur.

But following my career trajectory, I might be up for up to $250000 per year.

I’m going to leave that entrepreneurship part. $250k per annum? That is wild.

Yes. In my heart of hearts, this is it. The trick to earning well is to ensure you add enough value to account for your high salary. The higher ranked you’re, the easier it is to directly link your performance and remuneration.

Let’s create a scenario of a road to 250k. And what it looks like.

Go for Master’s next year – that should take a year. Start as an investment professional at one of the top Development Finance Institutions – $120k to 150k per year. Work my way through promotion to get to $250k per year.

Do you know what makes it more interesting? Earning that and living in Naij. Your house and utility bills won’t be alarming.

Multinationals also have a way around taxes which makes it less painful. Life is sweet.

What way?

A segue, but there seems to be a history of black tax with you.

It’s suffocating and needs to be handled with a brave heart if not, it’d leave the taxee frustrated and broke.

It is very dicey because I mean, who doesn’t want to help the family? I find myself struggling with it because I’d give an arm and leg for my nuclear family before I remember that I can’t walk.

But for young black professionals to be able to grow sustainable wealth, they must learn not to be guilt-tripped into giving all their money away. This would also prevent them from depending on their children when they grow old – they’d have an attractive retirement fund and viable investments to fall back on.

Word. Black Tax is a short term inconvenience for long term financial freedom. Discuss (20 marks)

I think it all depends on how you handle it. Paying black taxes on things like education of younger ones or buying a property for your old ones (which can serve as rental income) and all that can lead to a long term financial freedom because you’re empowering them.

However, if you use a chunk of your earnings to cover recurrent income (paying the food bills and electricity bills of many families), then there’s no long term freedom.

I always feel broke after I pay for all the important stuff and my account balance starts to dwindle. I literally panic.

Sorry.

What’s the last thing you paid for that required serious planning?

Everything. I plan for everything.

Do you have a safety net of sorts, in case anything goes south?

I know this is irresponsible but I’m trusting on my good genes not to fail me. I haven’t been sick almost all my life. I just need to make it to the middle of the year. No school fees to pay. Would have raised enough for rent.

On a scale of 1-10, how would you rate your financial happiness?

3. I need more money. I need a very nice apartment and to uber my way through life – I don’t want to drive in this traffic. I need money to start investing.

It’s like you didn’t come to this life to suffer at all.

I want it, and I’m going to get it. Many times, people don’t believe me, so I’ve started talking less. Sometimes, I’m scared about how passionate I am of these things.

I never got to ask, was it one of the cold emails that landed you the current job?

Let me tell you. I made a list of 12 companies – I was picky about where I wanted to work – and sent cold emails, LinkedIn requests and all that job stalking stuff.

And that’s how I landed this job.

Funny thing is, I still get interview requests from them but guess who now sends rejection emails to companies?

Energy.

Check back every Monday at 9 am (WAT) for a peek into the Naira Life of everyday people. But, if you want to get the next story before everyone else, with extra sauce and ‘deleted scenes’, subscribe below. It only takes a minute.

“Sticks and stones may break my bones but investment excites me.”

Those are the opening lines to a song I completely made up. But it’s also how I want my ideal relationship with money to look like. Each payday, I keep wondering “What are the investment opportunities for me?” “When will my enjoyment return from war?”

Maybe it’s the new year, maybe it’s my new age, but I decided to talk with someone more financially sound than I am about money and investment opportunities. Here’s what I learned:

Disclaimer: This is not to serve as a religious text but more to provide a way to look at approaching this issue one God-when at a time.

Charity begins at home.

The first takeaway from the conversation is that you should invest in yourself.

This doesn’t necessarily mean you should take a course or get an additional degree. The investment can be as little as reading a book on a regular basis, networking (Detty December) more to increase your social capital, or simply putting yourself in spaces that encourage growth.

Start where you are.

The second takeaway, although unpopular is that you should develop a savings habit. No matter how little.

Mad oohh Sorry, preposterously bonkers, but there’s inflation. How we go take do am?

After the discussion, there are three ways I have decided to think about this:

1)An investment that isn’t affected by inflation.

Think of foreign currency: “*One million dollars, elo lo ma je ti ba se si Naira?” whether you buy dollars from mallam and put under your bed or you use Piggyvest or Cowrywise, it is a good place to start.

To learn more about this, this is a good place to start.

2)Put money in something that gives returns above inflationand Nigerian anyhowness.

Things like government bonds, treasury bills used to be the preferred tool. Although the return rate is currently below inflation, a six percent return from treasury bills is better than a zero percent return from leaving money in the bank. T-Bills and government bonds are also relatively easy to learn about.

3) Try to learn about the stock market.

While this is also uncommon advice, it helps to think about this long term. This is more difficult to understand, riskier, and gives higher returns long term. So, learning and testing the waters with little sums can prepare you for higher stakes. You should only consider this as an extremely long term project and not short term in any way.

Ahan. Is that all?

Also, alternative investments should be considered. Depending on where you fall, this includes anything from bet9ja to agriculture and even transportation.

You should only invest your money in anything you can verify. If it sounds too good to be true, then it isn’t.

For an extra source of investment in Nigeria, make sure you verify the background of the people, where your money is going to, and how your money will work for you. If you can’t verify these things, take a step back and regroup.

Wow. This was long, abeg summarize

Invest in yourself as this is the fastest way to increase your earning power.

Develop a savings habit because learning to pile money increases how much you can invest with and thus increases your returns.

Invest in things above inflation, not affected by inflation, and learn how stock works. The last part is important for long term planning.

Mahn, this was long and I don’t know if anyone got here. If you did, don’t forget to show off some of your newfound knowledge to your friends.

If you’ve tried setting aside a part of your income for the future but failed, there’s a high chance that your main problem was with willpower. It’s okay. You’re not alone.

Even Jesus said that the spirit is willing but the flesh is weak.

Your willpower – more wobbly than a tower of Jenga – has put you in terrible situations when it comes to money. Situations not unlike these:

1) That time a rich relative gave you money that you were grateful for but didn’t exactly need right then so this was you and the money staring at each other and wondering what was going to happen next:

You ended buying up food with the money. You still regret your decision to this very day.

2) When an onigbese that has been owing you money for a long time finally pays but you’re currently in a good place financially and don’t know what to do with the money.

“WHERE WAS THIS MONEY WHEN I NEEDED IT, EHN?!“

3) That time you gave your savings to a family member to keep for you and made them swear to not give it back under any circumstances but this was you three days later when you wanted to buy new shoes:

Y’all are close so they forgave you eventually. It took a while though.

4) That time you actually saved a bit and were proud of your progress so you splurged on a little present for yourself but got too excited and overspent. Then this was you with the present:

What you thought would bring you happiness brought sadness and despair instead. This world nawa.

5)That time you were focused on saving money but your friends planned a trip to Rufus & Bees and you didn’t want to be left out so this was you playing arcade games:

You spent like 30k that day. Your friendship with them has been rocky ever since.

You know what’s better than having a Mexican standoff with money you own but know you’re not supposed to squander?

Introducing AELLA NOTES.

Aella Notes (from the fin-tech company, Aella Credit) is an investment web service that helps individuals invest safely. Interest rates range between 4% and 26%, depending on the size of your investment and length of time of investment. All you need to start is a minimum of ₦100,000 to start.

The best part is that you don’t need to worry about where your money is at any given time. The service has an easy-to-use interface that lets you track how your investment is being used. You can even create multiple investments. Click here to sign up.

Okay, let’s rewind a bit. I have always wanted to venture into farming, maybe it’s because I believe there is so much potential in the business. But every attempt at getting started and keeping up with it has been a serious pain.

Who did I offend?

First, I started out trying to cultivate maize on one acre of land and let me just tell you now, it’s not beans.The headache started with the farmer I partnered with because even though he had some experience with farming, he didn’t know too much about maize and he could have advised me on a better seed variety.At the end of the day, I waited to harvest the remaining maize and prepare to sell. What no one tells you about agriculture is the insane risk that is involved especially if your farm isn’t insured, and that’s exactly what happened to me. I didn’t insure my maize farm so I bore all the losses.Thankfully, I was relaying this story to a good friend of mine who had a smile plastered on his face while I was recounting this horror story of an investment.At the end of my long pitiful recount, my friend just shook his head and told me that had he had already read a lot of similar stories online and that was why he took the safer and more guaranteed route.He told me that he also had a maize farm and his farming has been nothing but smooth. He didn’t have to deal directly with farmers, because he sure didn’t have the time to train them, neither did he deal with labourers or selling the farm produce at the end of the farm cycle. I almost fell off my chair.

Is this real?

So I probed further and discovered that my friend had invested in agriculture through a platform that took care of dealing directly with farmers. The farmers had hands-on training from dedicated farm specialists, they were given improved seed varieties and were always on-ground to monitor the farmers, from planting to harvest to getting off-takers for the product so that there is nothing like wasted produce or the farmer can’t sell after harvest. To say “I felt I had just been handed a hot EXPO to profitable farming in Nigeria” was an understatement. I was excited.So, I invested the little money I had left from my misadventure into my old maize farm and used it to sponsor maize farms on this Agric platform which I later got to know was Farmcrowdy. Of course, I still did my research and I kept seeing nothing but good reviews, coupled with my friend’s testimonial, I just went ahead. Sat down, relaxed and waited for the harvest while getting all the farm updates on my dashboard. At the end of the farm cycle, I collected my initial investment plus pure profit, without lifting a finger. I have not looked back since then and I have continued to sponsor more farms to build my personal investment portfolio in the agriculture space. My name is Nnaemeka Obinna and I am now a proud farmer because I farm on Farmcrowdy. Better to work smart, than to work hard!

They’ve probably heard about it on a WhatsApp group and got curious, so they decided to put the school fees they paid to use by asking you about it.

Then you innocently start mentioning blockchains and wallets

They’ll follow you till the end of your speech like they perfectly understand, but just know it’s a scam.

Then you mistakenly mention “invest”

This sparks all kinds of red flags for them. “Is it like MMM?” “Will they run with my money?”. They somehow start to ask all the critical questions.

They give up and say they’re not doing it again

If anything sounds like too much risk, you can expect them to move in the opposite direction.

But they see you making money from it

As a wise man once said, “If you no make am, no evidence say you try your best”. They’ll eventually see you balling with the money you’re making from crypto and they’ll get interested too.

Then they’ll invest

Eventually, you’ll explain the whole thing one last time and they’ll pretend to understand, but they just want the money. You’ll help them sign up for a crypto exchange like Luno where they can buy some Bitcoin and Ethereum. Their money will go up and they’ll start looking at you like they’re reaping the fruits of their labour.

Then it dips for a moment and they’re holding your shirt

They’ll hold you like you’re the one who turned down the price. Even though you explained everything to them from the start.

Investing in crypto can be a stressful thing. So, why not use an exchange that simplifies it for you and makes it easy to use? A perfect example is Luno, which allows you to buy and sell cryptocurrencies like Bitcoin, Ethereum, and Litecoin very easily. All you have to do is download the app and sign up to get started.