Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the wordpress-seo domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /home/bcm/src/dev/www/wp-includes/functions.php on line 6121 Finances | Zikoko!

Recently, American actress Gabrielle Union and her husband became the subject of multiple internet think pieces after she revealed they take a 50/50 approach to their finances as a married couple.

Considering Nigeria’s mainly patriarchial society that still pushes the male-head-of-household mantra, I reached out to married Nigerian women to confirm whether there are Nigerian homes that employ the 50/50 approach to finances, too. It turns out, there are.

“At least, nobody can call me a burden” — Tola*, 33

I got married immediately after graduating from the university in 2015. I didn’t have a job, but he made enough money for both of us. He never complained about it, and I didn’t think getting a job was necessary. When we had twins in 2017, he began to murmur about expenses. One day, I asked him for money for a friend’s asoebi, and he said, “Do you want to kill me with demands?” I reported him to an older friend who told me to get something to do if I didn’t want my husband to develop hypertension.

When my children turned six months, I told my husband I wanted to find a job. He agreed, and luckily, I found a job quickly and got my sister to live with us and help out with the kids. Now, I give him half of my salary immediately it enters and still buy things in the house. My family usually says, “Isn’t your husband supposed to be taking care of you?” I don’t care. At least nobody can call me a burden.

“It just works” — Precious*, 29

My husband and I have a joint account, (separate from our personal accounts), where we send half of our salaries at the end of every month. It’s money from this account we use to sort out household expenses. We’ve done that for two years now, and it works for us. When money in the joint account isn’t sufficient for a particular expense, my husband makes up the difference.

“It’s my way of showing support” — Lolade*, 27

My husband and I have always gone 50/50, even before marriage. We’d go 50/50 for major dates and did the same for our wedding. Now, he handles household expenses like rent, fuel and major home repairs, while I handle groceries, data and Netflix bills, and little needs. When we have kids, we’ll also figure out a way to split. I earn more than he does, so it’s my way of showing support.

“It’s quite tough” — Mimi*, 36

My husband is really conservative. If not for the state of the nation, he wouldn’t even allow me to work at all. He got me a clothes retail shop some years ago on the condition that I’d use my income to support the home. It started out well, but recently, I’ve had to take up almost 70% of the household expenses, including the children’s school fees. He’s usually owed salaries at his workplace, so most times, we have to borrow from my business. This money hardly gets refunded. It’s quite tough because I have zero savings, and I can’t even complain because it’d seem like I’m being disrespectful.

When we decided to move to Lekki to be closer to work in 2021, we agreed that we’d have to split the ₦3m rent because neither of us could afford it alone. That’s the only thing we split 50/50. For other household expenses, we just attend to them as they come. He can buy foodstuff at the supermarket on his way home today, and I can remember we need engine oil when I step out tomorrow and just buy it.

“It’s not a rigid arrangement” — Chinny*, 30

My husband and I each earn below ₦100k per month, and we know it’s impossible to have an average standard of living if we rely on only one person’s salary. So, we pool half of our resources together to settle the bills and school fees of our two kids. It’s not a rigid arrangement. Some months, I may take up 70% of the expenses, and other times it’s 40%. We just do whatever we can to survive.

“It sometimes feels unfair” — Glory*, 31

My husband and I decided to go 50/50 when I got a job that paid more than his in 2021, but it sometimes feels unfair. I only agreed to go 50/50 when money started being an issue in the house. He felt I had money but was comfortable with him being broke, so I agreed to the arrangement to let peace reign. His idea of 50/50 doesn’t apply to household chores. I still do everything in the home. I’ve brought this up a number of times, but he takes it to mean I want to start ordering him around because I have money. If I can support him with the finances, why can’t he support me with chores?

*Names have been changed for the sake of anonymity.

One day, you’re wondering where to find the shortest fuel queue. The next, central bank decides to change its currency, fix a short deadline on old notes, then goes ahead to make the new notes scarce and force everyone to go cashless.

I didn’t think it’d be an issue really, until my bank started acting like the weapons fashioned against me, and I couldn’t even go cashless in peace. So, I tried to survive on only ₦500 cash at handfor two weeks, and I’m still alive. It’s very likely you don’t have cash too — or you don’t have enough for the necessary small transactions — so let me teach you how to survive this period.

Stay at home

Whoever invented introverts knows ball. I’m not much of an outside person, but this period has further taught me the wisdom of sitting at home and eating whatever I have in my kitchen. If work makes you leave your house every day, I sympathise with you.

Do online transfers for EVERYTHING

When they work, at least. A friend told me how she transferred ₦300 to a pepper seller. Thing is, you won’t know who accepts transfers unless you ask. Ask that okada man for a transfer option today.

Become interested in fitfam

Do you really need to take a bus when you can walk? Do you actually crave shawarma, or are your village people just working overtime? You can always tell yourself you’re pursuing your fitness goals.

Sleep

You can’t spend money while you sleep.

Shop at supermarkets

Since the major problem is cash, do your shopping at places where POS transactions are readily available. Of course, your bank can still disgrace you, but what’s life without a little risk?

Date a POS attendant

Who knows, you might get free new notes as a relationship privilege. Plus, imagine dating one of the hottest set of people in Nigeria right now.

Just give up

Even if you survive the two-week mark, what’s the assurance that the cash situation would’ve improved by then? God, actually abeg.

Cryptocurrency is everywhere. All over social media, you are likely to run into TundeBTC, Amaka.Eth, Ima.sol, and similar nicknames. You want to be one of them but don’t know how to start. Or you’re simply curious about crypto as a concept.

This article is for you, welcome.

Here are 5 things you need to know to be a proper crypto bro and get started as a crypto trader in Nigeria

1. Do Your Research

Cryptocurrency, blockchain and other related concepts can seem complex to understand, particularly with the way it is spoken about online. It often comes across as rocket science that can only be comprehended by super geniuses. We can assure you that point of view is a limited one and only exists for gatekeeping purposes.

This may sound overly simplistic but all it takes is a google search to start off your journey into demystifying cryptocurrency. There are tons of articles, crypto blogs, podcasts, and youtube videos explaining different terms and concepts within the crypto-blockchain ecosystem. Filter the social media crypto noise and do your own research. A great place to start is this free online crypto academy where all the crypto terms are explained in layman terms for quick understanding.

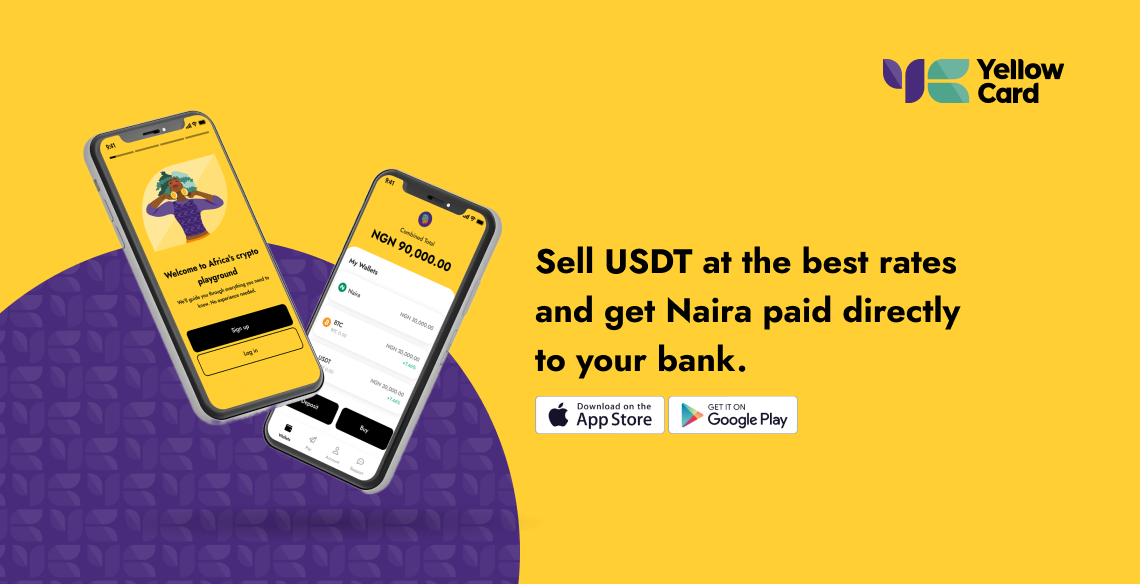

2. Use a Reliable Cryptocurrency Exchange

There are many crypto exchanges online, which is a good thing. The problem however is selecting the right one for you. As a crypto trader, there are certain basic criterias an exchange platform must meet such as low barrier entry, easy KYC process, affordable rates and 24/7 customer service.

As Nigerians, we need an easier way to get into crypto and exchanges that are tailored to our reality are the best fit. Fortunately, we have several homegrown crypto exchanges like Quidax, Buycoins and Yellow card. They all have amazing features. Quidax has an order book and 0% maker trading fee. Buycoins has instant P2P. Yellow Card has quick crypto-to-cash conversion and vice versa, little to no transaction fees, best rates in the market, plus you can literally trade with just 500 Naira.

3. Keep Your Eyes and Ears Open

Crypto trading requires a significant level of alertness. While it is inadvisable to dedicate every waking hour to monitoring the charts and keeping up with crypto online community discussions; It is necessary to stay up-to-date. Keep your eyes open for change in trends and keep your ears open for trading tips.

4. Avoid Market Peer Pressure

Peer pressure in the crypto ecosystem is very real. Even the most experienced traders have fallen prey to it at one point or another. Some might say it’s part of the cryptocurrency experience. Still, crypto peer pressure or FOMO (Fear Of Missing Out) can be avoided by always doing due investigation before buying any coin, token, NFT, or investing into a defi or web3 project. The crypto-blockchain ecosystem is as full of scammers as it is full of genuine innovators. Do not let market peer pressure coerce you into staking all your money on a scam project or investing all your funds into a scam coin/token.

5. Never underestimate security of your assets

Online security has never been as important as it is today. If you look up “crypto hack” on the internet, you will find over 10 serious hacks that have happened just this year alone. Your money and assets deserve to be stored in a safe wallet. You deserve to trade on a platform that values the security of your identity and assets. Exchanges like Yellow Card understand this and have fully implemented safety measures to ensure your funds stay protected.

Conclusion

Trading crypto is not as mysterious or as exclusionary as social media makes it out to be.

You just need two things – research and a solidly built cryptocurrency exchange to get you going.

One of the best things about choosing Yellow Card as your crypto exchange is that with just 500 naira, you too can become a Bitcoin Baddie or a Boss.eth. You also get great USDT rates, because what good is your money if you can’t get the best value for it? Sign up to sell USDT at the best rates in Nigeria.

Ever heard of sapa? Well, it’s that evil spirit that has made so many people resort to desperate — and sometimes, downright hilarious — attempts to get their daily urgent ₦2k to put food on the table.

I spoke to some people and they shared the most desperate things they’ve done for money.

“I spent the night in a dark classroom”

— Tola*, 29

This was during the 2011 Nigerian elections and I desperately wanted to be a part of the INEC ad-hoc staff. I’d applied but didn’t get selected. I got the bright idea to go spend the night in the school where INEC personnel would be taking off from, just in case somebody didn’t show up so I could replace them.

I met some other people there as well, and it was a long, cold night. Eventually, some of the selected staff didn’t show up in the morning and I took someone’s place. They paid me only ₦13k after everything — they even delayed payments by over two weeks.

I’ve also done ushering service jobs where I’d get paid ₦1k for a whole day, after leaving home at 5 a.m. and returning at 10 p.m. I did this between 2008 and 2011. Sure, I got to eat at the events, but it was horrible — all the insults and stress were just ridiculous. I can never do either of these two “jobs” ever again.

“I commuted from Ikorodu to Owode-Onirin every day for ₦500 daily”

— Wendy, 25

In 2013, I was trying to save up for JAMB, so my neighbour introduced me to a food canteen in Owode-Onirin where they paid ₦500 per day. I’d go there as early as 5 a.m. and try to convince the iron rod sellers near the canteen to buy a plate of food from me. Each plate was about ₦300, and I needed to sell at least 20 plates, retrieve them, wash them and sweep the store by 6 p.m. to get my ₦500 for that day.

I didn’t get paid in full somedays because madam could just complain that I wasn’t smiling or that I didn’t attend to a customer “well”. My transport fare to and from the canteen was about ₦200, and sometimes I only made a profit of ₦200 after everything.

I didn’t last up to two weeks there because one of the male sellers slapped my bum one day, and I hit him back in the face. Nonsense.

“I de-feathered chickens on the road for about ₦200”

— Charles*, 24

This was during the Christmas holidays in 2016, and of course, there were chicken sellers everywhere. All you had to do was walk up to a seller, select a chicken, and you could decide to have it killed, de-feathered and cut up for you for a price by the seller’s assistant.

My friends and I were broke so we decided to try this assistant business out. We suffered. We burnt our hands from the hot water we had to use to de-feather the chickens, and the hot sun beat down on us for hours. The angry and impatient customers yelling at us didn’t help matters. And for what? Payment of less than ₦200 per processed chicken? God abeg.

Less than a week later, my mum eventually had to ban me from going back when I started looking pale. Fun times.

“I worked at a construction site”

— Onyeka*, 45

This was when I was a broke student at LASU. I think we were on strike, but my roommates and I couldn’t travel home because we didn’t have any money. For days, we depended on soaking garri until one day, I noticed another roommate eating rice.

Of course, we were all shocked and asked where he got the money. He was reluctant but later told us that he’d show us only if we promised we’d be able to do it. Broke men like us? We had no choice.

The next day, he took us to a construction site he found, and the site manager graciously hired us. We had to carry cement and sand all day for ₦500. When we got back to the hostel, I seriously thought I was going to die. My body ached like I had been passed through a grinder.

Ibuprofen came to the rescue sha and we kept going back until ASUU called off the strike.

I’m not proud of this, but I once had to sell my mum’s gold necklace without her knowledge to settle a debt.

I was in my third year of university, and things were hard at home. I was on the verge of missing out on my exams due to unpaid fees — about ₦30k. I had to borrow money. Not long after, the person I borrowed from started pressuring me to pay back. I kept posting him till he sent cultists to threaten me — apparently, his cousin was a cultist.

I knew my mum would never sell the necklace because it was a gift from my late dad, but my life was at stake. I think she knows I took it, but she never questioned me.

For about three years, I made a lot of money writing exams for people, including WAEC and polytechnic exams. It was very risky, and also involved heavily “sorting” invigilators, but it paid well.

I wouldn’t do it again, though — I have a proper job now, and I don’t think it’s as easy to impersonate students now, compared to 2009-2011. I also can no longer afford to risk getting jailed.

* Some names have been changed for the sake of anonymity.

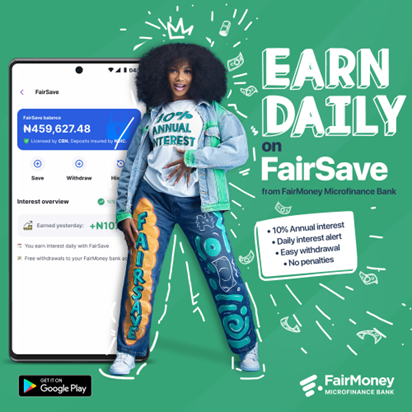

These days, every day is a “rainy day”, so saving money for the rainy days is no longer an advice, it is a must. But here is the good part, some good guys have put in the work to help us not only save money easily, but also make money everyday on the money saved, cool right? This is why we are introducing to you ‘FairSave’. Now hear us out;

FairSave is the newest savings product from FairMoney MFB aimed at helping you save and make money while you do other things you love. Here are 5 benefits you enjoy when you make savings a lifestyle with FairMoney’s FairSave:

1. First of all, you get up to 10% interest on whatever you save on the app.

This means that if you put one million in your savings wallet you can get 10% interest on that money for just saving it in that wallet, ok maybe not 1 million, but you get the point.

2. Easy withdrawal

You can withdraw your money (Principal and Interest) anytime you want. Nobody is locking your money for days or months. Your money is readily available and can be accessed anytime you need it.

3. No penalties on withdrawal

It is your money, so why should anyone charge you any dime for withdrawing because you need it. If you decide to remove your money anytime, you will not be charged a dime.

4. Daily interest alert

You receive an interest alert everyday!. This will ginger your spirit and you can be motivated to add more money to your savings because you know that your money is growing like grass. Another interesting part now is that you can withdraw your interest whenever you want.

5. Access to other FairMoney products.

In case you don’t know, the FairSave wallet is one of the products inside the FairMoney app. When you decide to use FairSave you automatically become a FairMoney Fam and this means that you can access the FairMoney FairBanking products.

What are you still waiting for?

Download the FairMoney app on playstore right away so you can join the FairSave geng to start enjoying all these benefits.

There’s a chance that you’ve once received a random message or call — with the caller sounding like they’re at death’s door — informing you that a family member or friend you haven’t even spoken to in years, owes an amount of money and will be disgraced soon.

On the off chance that you haven’t experienced this, you must have come across some “instant loan” offers.

What’s it like to take loans from some of them? Here’s what these Nigerians had to say:

“I still don’t know how they got all my contacts”

— Omolayo*, 27

I had been getting their promo text messages for a while and since I urgently needed money, I thought to try them out. I borrowed about ₦6k and I think I had to pay a total of ₦8k after 15 days. It was a relatively straightforward process — I had to provide my details, BVN and the details of two guarantors.

The problem started when I didn’t pay immediately after the 15 days were up. They started calling everybody on my contact list, not even my guarantors. They even threatened to get me arrested.

Thinking about it now, maybe they got the information through my BVN. This whole calling my contacts thing wasn’t communicated to me beforehand. I never paid back, and they didn’t do anything after the calls. I’m still waiting for the promised arrest.

To be fair, I knew the risks when I took out a loan from this app, but I desperately needed the money. I figured that even if I didn’t have it by then, I could borrow the required amount from another lending platform to settle it.

Things didn’t go as planned, and I started receiving calls from them on the day I was to pay them back. Within a few hours, they began sending messages to my contacts with my name, age and BVN, threatening to post my pictures everywhere the next day and brand me a thief.

It was so embarrassing to receive calls from my bosses and church members. I eventually paid back and was so happy when I learned that the government had shut them down.

I first heard about this loan app from my roommate at the university. The thing is, I got a text message informing me that this roommate had collected money and was yet to pay it back. It went further to say, “The whole family of [my friend’s name] is not to be trusted. Inform him to pay up his loan because devastating things could be done to his family’s reputation.”

I didn’t pay attention to it then and forgot to bring it up. Later on, I needed money myself and decided to try them — I figured they only made the threats if people defaulted. I took a loan and paid it back within the time frame. I soon became a regular customer, but the first time I delayed payment for a day, my family members received calls and messages.

The funny thing is that they never apologise for tainting your reputation after paying back. I guess that’s the way it is.

“They still sent texts to take another loan after disgracing me.”

— Linda*, 33

I’m a single mum and the sole provider of my daughter’s needs. I bowed to pressure to take a one-time loan when I urgently needed to sort out my daughter’s school fees. The interest was quite high — I think about 20% — and I was to pay it back after three weeks.

When the date approached, I realised I needed more time, and I tried to see if I could extend it, but it just wasn’t happening. When I missed repayment by one day, they texted me that they would publish my obituary. I thought it was a joke.

They started threatening my contacts and disturbing them with persistent calls. It was a nightmare. People that hadn’t bothered to check on me and my child for years now knew we were in trouble.

When I eventually paid, I swore never to have anything to do with them again. A few days later, they sent me another text asking to get “instant collateral-free loans.” They should hold it.

“It’s still a business.”

— Joe*, 26

I regularly take loans from these online guys because I run a monthly joint savings thing with some friends. My salary doesn’t come in regularly, and I sometimes have to rely on these loan apps to meet the monthly savings deadline.

I always keep to repayment time, so I haven’t had any ugly experiences. I think they go to these lengths just to secure their money back. I’ve gotten messages informing me about friends or colleagues that defaulted, and though I agree that most are too extreme, I figure they just do what they gotta do.

*All names have been changed for the sake of anonymity.

While smart investing is a sure way to build and retain wealth, it can be a daunting prospect for beginners. In the same vein, it is a lot easier when you understand the various options in which you can invest and ultimately grow your wealth. Here are some options you can consider when taking the step to managing your wealth like a pro – explained in simple terms:

Treasury Bills

Treasury bills (T-bills) are risk-free, short-term investment instruments that are issued by the Federal Government through the Central Bank of Nigeria (CBN). It is a way the government raises funds from individuals and organisations. They are considered among the safest investments with attractive returns since they are backed by the full faith and credit of the Federal Government. In addition, the longer the maturity date, the higher the interest rate that the T-Bill will pay to an investor. Although T-bills yield a lower rate of return compared to other forms of investment, they offer safety and a predictable profit which makes them a good choice for long-term investments in your portfolio.

When investing in T-bills, it is important to take note of the prevailing rate and your expected returns upon maturity. However, if you decide to sell before maturity, you may incur a loss depending on the prevailing market value.

Fixed Deposit

A Fixed Deposit is a short-term investment that guarantees you a fixed interest rate when you keep funds for a specified period. The minimum tenor is 30 days and the maximum is 365 days – at the end of the agreed period (tenor), your principal and interest amount earned are paid to you. This product can also be used as security for cash-backed loans.

The ideal strategy for Fixed Deposit investments is to diversify and spread out your investments across various banks while striking the right balance between risk and returns. It is also important to note that if your Fixed Deposit investment is terminated before maturity, the total accrued interest not earned will be forfeited. This means that only the portion of interest earned during the period that your money was held is what will be paid to you.

FGN Bonds

Federal Government Bonds are long-term instruments issued by the Debt Management Office on behalf of the Federal Government of Nigeria (FGN). When you buy FGN Bonds, you are lending to the FGN for a specified period of time and the FGN is obligated to pay you the principal and agreed interest as and when due, meaning that they have no default risk. Not only do these bonds offer opportunities to investors willing to invest long-term but also attractive interests that are paid bi-annually (twice a year). FGN Bonds can be accessed through primary licensed dealers and before investing, pay attention to the prevailing rate, maturity, payment dates and expected returns so you can make an informed decision.

Commercial Paper

A Commercial Paper (CP) is a short-term unsecured debt instrument issued by financial institutions and large corporations with high credit ratings. As a short-term instrument, CPs normally mature within 270 days. CPs are issued at a discount, which means interest is paid upfront. CPs are more suitable for risk tolerance and before investing, you may want to do your due diligence on the issuing company and take note of its risk of default. This entails an evaluation of their credit rating, brand reputation and experience of the management team. While CPs offers a return on investment in 270 days or less, it’s paid at maturity, not periodically, like with FGN bonds and other similar debt securities. It may be wise to consider all of your investment options before investing in commercial papers.

Eurobond

Eurobonds are financial instruments denominated in a currency other than that of the issuer – for example, a Nigerian Eurobond is issued by Nigeria in U.S Dollars. Despite their name, Eurobonds aren’t necessarily denominated in Euros and can take many different forms. They are issued either by Governments or corporate institutions and are highly liquid i.e can easily be converted into cash, which is a key benefit of this form of investment.

Given that Eurobonds come as government and corporates, as a prospective investor, you have to decide which to buy. While corporate-issued Eurobonds may offer higher interest than government-issued ones, they also offer higher risk. Like every other investment, buying Eurobonds should be a well thought out process and it is advisable to review and understand the risk profile of any Eurobond that you are interested in buying.

Managing your wealth

Wealth management is personal and there’s no one-size-fits-all approach to go about it, which is why it is important to have the right knowledge and information.

Always start with a clear picture of your financial goals while understanding your risk tolerance. Once this is understood, diversify your portfolio with the mix reflecting your tolerance for risk. Understanding these investment options is essential, however, it is also important to rely on sound recommendations from experts while dismissing “hot tips” from unverified sources. While this can seem complicated, a good partner will make it simple – even exciting.

The digital investment app, M36, not only delivers a wide range of investment products, including those highlighted above, but also offers support by professional financial advisors to enable you make sound investment choices that suit your needs.

Download the M36 App from the Google Play Store or the App store today and pick Your Track to Wealth.

Personal loans are good for a variety of purposes—from consolidating debt to solving a myriad of pressing issues. They are personal, which means your reasons are yours.

Do you remember the first time you needed more money than you had? Borrowing money then was not as easy as it is now. You probably would have run to family members or friends which usually meant nothing was certain, or apply for a bank loan, which was a very tedious process, hard to get – especially if you do not have an enviable collateral in choice locations, or know someone in top management position in the banks to stand as a guarantor.

The situation is completely different now. There are financial services providers like Page Financials who have changed the game entirely, they have not only disrupted the borrowing and lending ecosystem but have also shaped how even the banks respond to providing these services today.

With the intervention of Page Financials, a leading financial services provider, anybody with a verifiable and consistent income, that meets a few other criteria – like having a good credit history – can now easily get a personal loan from the comfort of their home.

If you are still thinking about whether or not to consider a personal loan, we have highlighted 5 reasons why customers usually resort to getting a personal loan.

1. Cash emergencies

If you need money right away to cover bills, an emergency cost or something else that needs immediate attention, you can take out a personal loan. Page Financials provide online applications that allow you to complete application conveniently in minutes. You could receive funding immediately as well, depending on your past credit history and the information you have provided.

You can use a personal loan to cover emergencies like:

Paying past-due home payments and utilities

Medical bills

Funeral expenses

An unexpected car repair or purchase

What you can do with a personal loan is limitless, and as established earlier, it is personal to you.

2. Debt consolidation

One of the popular reasons to get a personal loan from Page is for debt consolidation. If you have existing facilities with different lenders, you’d agree that managing multiple loans from several lenders can prove to be challenging. Missing on payments can result in negatively impacting your credit score. Availing a personal loan in such a situation can save you from financial distress. All you require to do is approach Page and state that you have some other loans elsewhere and would like to consolidate different payments into one debt with the help of a loan. This method offers several benefits that include enjoying an overall lower rate of interest which can help in reducing the timeframe required to pay-off your loan.

3. Rent, home improvement and repairs

Whether you want to renew your rent or looking to move to a more befitting neighborhood, or simply looking to upgrade your apartment and fix some repairs, a personal loan is a great way to cover the costs conveniently. The urgencies that come with meeting these needs are usually unprecedented which is why a personal loan may be your surest way to meet up with the deadline. Failure to meet up with rent on time for example will lead to series of embarrassments from your landlord, and…you don’t what that. In the same vein, if you see a new apartment that you love and fail to make payment on time, the house goes to someone else that has cash at hand. This is why speed and convenience are of essence when it comes to personal loans and part of the USPs at Page Financials, you can access a loan and get support anytime whether it’s 2 am or 2 pm so you don’t have to miss any opportunity again.

4. Vehicle financing

Auto loans are available if you’re looking to buy or lease a car, but personal loans are also available to finance any need you may have – including a vehicle financing. Another great reason why you should consider a personal loan rather than going for an Auto loans are secured loans and use your vehicle as collateral. If you’re worried about missing payments and your car getting repossessed, a personal loan might be a better option for you.

5. Starting/expanding your business

Side hustles are very popular these days, and are a great way to test the entrepreneurial waters. If you have one, or you are thinking of starting one, you are going to need some funds to run or expand it. Channeling extra funds into your side hustle can help you take it to the next level. But if you don’t have the money you need now, taking out a personal loan for your side business may help. Getting an outright business loan would normally require some sort of security or collateral – which most startups don’t have, which is why taking a personal loan as a salary earner – to fund your side business, would be a smart thing to do. Personal loans may be well-suited for side hustles because they are often smaller than typical business loans and don’t require a high level of collateral or profitability. All you need is a proven source of income — and that can come from your current day job.

What to consider when considering a personal loan

Applying for a Page Loan is super easy, everything happens online and you don’t need to visit their office.

The application process is in stages, at each stage, you’ll supply relevant information that helps make a decision to approve your loan. (See requirements for each category below).

You can upload all the documents online while filling the form so you do not have to worry about carrying files from one office(er) to another.

The first stage you will encounter while filling the application form is the BVN and IPPIS verification phase. You will be required to provide these details to help us to verify your identity and financial standing.

Loan requirements for private sector employees

To be considered eligible for a loan as a private sector employee, it is required that:

You earn a monthly salary (minimum 150k monthly)

You have up to 6-months’ salary account statement

You live/work in Lagos or Ibadan (bankers nationwide can apply)

You have a valid work ID from where you work or an evidence of employment or promotion

You have a BVN that is actively connected to your working mobile number

Some of the items above will be retrieved automatically when you begin the application, it usually takes customers less than 3 minutes to complete the application if they have the requirements ready. To apply as a private sector employee click here.

Loan requirements for public sector employees:

To be considered eligible for a loan as a Federal Government Civil Servant, it is required that:

You have your work ID

You have a valid Government issued ID

You have at least 3 months’ payslips

You will present a signed letter of authority to debit (the letter is available for download on our website).

To apply as a public sector employee, click here.

Reasons to avoid a personal loan

While personal loans can be a saving grace in times of great need, there are some instances you should avoid borrowing money. Consider avoiding a personal loan if:

You can’t affordit: Borrowing money in the short term is one thing, but remember you’ll still need to pay it back. If you can’t afford monthly payments for your new personal loan, consider skipping it.

You don’t need it: If you’re taking out a personal loan to cover the cost of something you don’t need in the immediate future, think about putting it off until you have more cash on hand.

The Page customer service is available 24/7 to answer any questions you may have. You can contact Page via a number of channels viz; Live Chat on the Page Mobile App, Live Chat on the website (Pagefinancials.com), social media accounts (@pagefinancials), Google chat (on Search Result Page).

Month has ended, meaning salary or allowance for you by the special grace of God. But even at that, have you seen how many days are in May? Thirty-one. So the real question is how long will your account balance last till the next credit alert?

Navigating life as a woman in the world today is incredibly difficult. From Nigeria to Timbuktu, it’ll amaze you how similar all our experiences are.

Every Wednesday, women the world over will share their takes on everything from sex to politics right here.

The woman in today’s What She Said is in her early 50s. She talks about her husband excluding her from all financial planning and how she has had to find out about several of his projects through friends and strangers.

Describe you and your partner’s financial planning situation in one word.

Insulting. My husband and I got married when I got pregnant for him at 23; he was around 36. That’s a 13-year age difference. He has always seen me as a child, right from day one.

He doesn’t hesitate to remind me that he is older and thus wiser, making remarks like, “I have been touching money since before you were born.” Back then, it really hurt, but I have since grown a much thicker skin. I just ignore him for my own peace.

What was the financial planning like in the very beginning?

As a naive young girl, I would collect my salary and keep on top of the wardrobe for both of us to take and sort things out in the house, while he would hoard his salary and sometimes not even tell me when he receives it. I didn’t think too much about it until a particular incident opened my eyes.

What incident?

I was 7 months pregnant with my eldest when I took about N3,980 from my savings and went to the market with my cousin to buy a bed for us. The one we had at the time was nothing to write home about.

About 3 days later, I took N50 from my husband’s pocket to make my hair. When he came back from work, he asked if I had touched his money. When I told him that I had, he flared up.

He started shouting that in my life I should never touch his money without telling him. My cousin was around when this happened. He was so shocked that my husband was acting this way because of N50.

Whoa.

When my husband went to see him off, I started packing the little things I had. My intention was to leave him. I think my cousin spoke some sense into him because he came back begging. I keep saying that if I had left the house that day, I would have left the marriage for good.

Did things get better after that?

No. My husband would make big financial decisions without consulting me. One time, he took leave from work and went to his village with our 2 children and laid the foundation for his house. It was someone in the village that called to congratulate me. I was just listening like a dunce because I was not aware of anything.

Did you confront him?

My dear, the beginning of my marriage was full of confrontations. When he got back, I asked about the project and questioned why he didn’t say anything to me.

To prove a point to him, I took out N100k from my savings — this was in the early 2000s — and gave him to add to whatever he had for the building. He was so shocked and somewhat ashamed that he wept.

Was there a change afterwards?

For a while, yes, but it was short-lived. My husband has serious trust issues when it comes to money and me. Sometimes, I would be in the room and he would run inside like someone being pursued only to take out money from his pocket and go into the living room. I just laugh it off because I am tired of crying.

So how have you both managed to run your home?

I do what I can for the house and he does what he can. It’s not a joint thing. One thing I am grateful for is that he is actually financially responsible. He takes care of what needs to be taken care of. He never joked with our children’s needs at all.

The problem just happens to be a “me” thing. I don’t know his bank account password or how much he has. As a wife, I know nothing about his financial life.

It was only recently, when he had a near-death experience, that he took me to different sites to show me his land. I was so shocked that he had property and waited until he nearly died to show them to me.

That’s awful.

I am supposed to be his wife, why am I the last to find out about thing like this? Am I a stranger? It looks ridiculous when you live with a man and call him your husband, but you don’t know anything about his finances. I am very open with mine, why can’t he do the same thing?

Have you considered leaving him?

Of course. Several times I would have left him for real last year because of this disclosure issue. Can you imagine my husband collected his pension and didn’t tell me?

Prior to me discovering this deceit, I have been taking care of everything in the house with my salary. He just retired and I had to shoulder most of our expenses. I kept encouraging him to hold on, hoping that when he gets paid, he will lighten my burden.

This man collected his pension and didn’t tell me for three months until I accidentally found out from a friend. I was so furious. For me, this was the height of wickedness. I had to force myself to calm down so I don’t end up killing him.

Ah, Ma, please oh.

Yes. A man who will look at you and see you as less can actually kill you, but I kept thinking about my children. What will people say? My husband is someone everyone considers to be good.

No one will meet him and think ill of him. Why do others get to see that part of him and he rarely shows that side to me? I don’t dispute the fact that he is a good man or a great father, but in the husband category, he falls short. I feel so alone in this marriage.

Are your children aware?

They only know what we tell them. I am trying to shield them from this aspect of their father. They are mostly grown now and are doing very well for themselves. I want them to be happy, knowing who their father truly is will cause them to worry. I have since discovered that this is my cross and I will bear it alone.

If you’d like to share your experience as a Nigerian woman, send me an email

For some young Nigerians, a savings culture is a mindset instilled at a young age, with many parents encouraging their children to put money aside for rainy days. Others weren’t so lucky, having to learn about saving alongside every other thing adulting throws at you.

I was curious about the saving culture among young people so I asked 7 people about their relationship with savings. Here’s what they had to say. Read below:

Shox, 24 – Saving isn’t the problem, rent is.

Personally, I think I save enough money. Usually, I save about 70% of my income so I don’t think I struggle on that end. The problem is depletion. I spend most of my savings on rent. Finding an apartment that isn’t an embarrassment to humanity and is within my salary range is nearly impossible. In all, I just think I have to earn more.

Mimi, 26 – I save alright, but black tax wants to finish me.

Saving isn’t really the issue. I just think I don’t earn enough money. I certainly used to earn a lot less when I was in Nigeria, but I had fewer responsibilities. Here, I have to think about rent, food and the almighty black tax.

I had a good savings streak until my brother died. I had booked a flight to Nigeria to see him when he was ill, but he died before my travel date. I spent more money to reschedule the flight for his funeral, but I missed that as well. Then my father needed money for his business and I had to take a loan for that too. I’m hoping my finances stabilise in the coming months.

Enejo, 21 – I don’t know how to save

When we were younger, my mother used to collect any money we got and saved it for us. It was done with our knowledge but we never actively participated in saving. Now, I’m not very good at saving money by myself. The money my mother saved for us is still in a trust fund and she occasionally deposits more money in it. Still, my saving skills suck.

Mo, 29 – I have three different saving portfolios

Personally, I don’t think it’s hard to save. I started saving when I was in secondary school, at the age of 15. It’s not like I was earning a lot then. It stemmed from wanting to be able to buy stuff without relying on my dad or my sisters and after that, it became a hobby.

Now, I have three different saving portfolios. I’ve been slacking though. I stopped working since I had my baby last year and my side business isn’t moving much. I strongly believe in saving because having an emergency stash is highly invaluable.

Molly, 29 – I haven’t touched my salary in almost 3 years

Me that I save anyhow? I haven’t touched my salary in about 3 years and I have N5.7m saved. I’m a lawyer, so I survive mostly on money from my private practice. I also get money from different sources, like my Dad. Generally, I don’t touch my savings for just any reason. I just save towards a target, like buying a piece of land or a car.

Tswaggs, 24 – I’m learning how to save

Omo, on God, I save as often as possible, although that’s a recent development. An emergency made me realise the need to start saving for rainy days. If I receive 10k, my brain automatically deducts 2k for savings and the rest is for balling. To be honest, it hasn’t been easy. Sometimes, you think you could use the money you’re saving for something else, but you really need to be disciplined.

Deola, 24 – My Mom does my saving for me

I’m not really a savings person like that because I always have my mom if I need emergency cash. Last last, she gives me the money and I repay her in instalments.

When I started working, my mom ensured she collected a percentage of my salary at the end of every month. When I was earning 45k, she would collect 10k. Now she has made me join an ajo (cooperative society)and I remit 20k monthly to it while I save 10k with her monthly.

The bad part is that always end up spending the money on other people, on emergencies or give it to my family whenever they need it.

“Sticks and stones may break my bones but investment excites me.”

Those are the opening lines to a song I completely made up. But it’s also how I want my ideal relationship with money to look like. Each payday, I keep wondering “What are the investment opportunities for me?” “When will my enjoyment return from war?”

Maybe it’s the new year, maybe it’s my new age, but I decided to talk with someone more financially sound than I am about money and investment opportunities. Here’s what I learned:

Disclaimer: This is not to serve as a religious text but more to provide a way to look at approaching this issue one God-when at a time.

Charity begins at home.

The first takeaway from the conversation is that you should invest in yourself.

This doesn’t necessarily mean you should take a course or get an additional degree. The investment can be as little as reading a book on a regular basis, networking (Detty December) more to increase your social capital, or simply putting yourself in spaces that encourage growth.

Start where you are.

The second takeaway, although unpopular is that you should develop a savings habit. No matter how little.

Mad oohh Sorry, preposterously bonkers, but there’s inflation. How we go take do am?

After the discussion, there are three ways I have decided to think about this:

1)An investment that isn’t affected by inflation.

Think of foreign currency: “*One million dollars, elo lo ma je ti ba se si Naira?” whether you buy dollars from mallam and put under your bed or you use Piggyvest or Cowrywise, it is a good place to start.

To learn more about this, this is a good place to start.

2)Put money in something that gives returns above inflationand Nigerian anyhowness.

Things like government bonds, treasury bills used to be the preferred tool. Although the return rate is currently below inflation, a six percent return from treasury bills is better than a zero percent return from leaving money in the bank. T-Bills and government bonds are also relatively easy to learn about.

3) Try to learn about the stock market.

While this is also uncommon advice, it helps to think about this long term. This is more difficult to understand, riskier, and gives higher returns long term. So, learning and testing the waters with little sums can prepare you for higher stakes. You should only consider this as an extremely long term project and not short term in any way.

Ahan. Is that all?

Also, alternative investments should be considered. Depending on where you fall, this includes anything from bet9ja to agriculture and even transportation.

You should only invest your money in anything you can verify. If it sounds too good to be true, then it isn’t.

For an extra source of investment in Nigeria, make sure you verify the background of the people, where your money is going to, and how your money will work for you. If you can’t verify these things, take a step back and regroup.

Wow. This was long, abeg summarize

Invest in yourself as this is the fastest way to increase your earning power.

Develop a savings habit because learning to pile money increases how much you can invest with and thus increases your returns.

Invest in things above inflation, not affected by inflation, and learn how stock works. The last part is important for long term planning.

Mahn, this was long and I don’t know if anyone got here. If you did, don’t forget to show off some of your newfound knowledge to your friends.

If you are anything like me, January has gone on for 80 days already. I was listening to FireBoy’s album the other day and I thought that some lyrics make a good cry for help. Here are some that resonated with me.

1 From the song Vibration – *”Egba mi, o pari oh”

*Someone save me, it is finished.

This was my reaction while checking my balance throughout December. I kept on asking: “who spent all this money?” Somebody send help!

2) Gbas Gbos from the song Gbas Gbos

Friend: How is your bank account like?

Me: Gbas Gbos. The usual.

3) “We go go America on a midnight train” – From the song What if I say

This is a financial red flag. Firstly, we don’t have a functional railway system in Nigeria. Secondly, we don’t have trains that go to America from here. Thirdly, if you enter midnight train in Nigeria, what you see is what you get.

4) “I am just trying to survive, I just want to win” – From the song Wait and See

This was my motto all through University.

5) *”If I say I should talk, where will I start my story from?” – From the song Energy

*Ti ba ni ki soro, melo ni mo fe so gan.

This is my reaction when people ask me anything about the situation of my finances. Where do I start from exactly?

All your life you have struggled with saving money and being financially independent? Every year, you make resolutions to improve but you give up midway and revert to your old ways. If this sounds like you worry no more, we have four not so difficult steps to guide you on the road to monetary freedom.

1. Learn to budget

If there is one thing you should include in your plans this year, it is tracking every single kobo you spend. Every single naira that goes in and out of your wallet should be audited and accounted for. No free money this year(wails in black tax). Anyone that needs money should call three months ahead so they can be included in your budget. Unplanned expenses are the single greatest source of financial disasters. Congregation, can I hear you say no impulse buying this year?

*Suddenly not so proficient in excel*

2. There is no passive income!

Any talent you can monetize, this is the year. From cooking to writing, and occasionally sleeping with other people – put a price tag on it! Seriously, think about any skill you currently offer for free and improve on it so you can make it a proper side hustle. One of the ways to achieve financial mobility is to increase your income.

*Addicted to cash*

3. Have an incase Nigeria goes to hell funds

If you can afford to (no responsibilities or absence of black tax), you should start to have a rainy day fund. If you earn enough to afford it, you should put away some percentage of your salary as an emergency fund because life is weird. Apart from your savings or investments, this is a good way to prevent unplanned expenses from resetting you back to brokeness land (I have been there and back I can show you vouchers).

4. There is always rice at home

The difference something as little as cooking your own food makes is enormous. Packing food to work can help you track your expenses and see what you spend money on outside of food. Also, learning to say no to the extra demands of owambe will greatly improve your financial outlook. Anything that is not important should be reviewed and immediately removed (Especially that gym subscription. We all know that summer body doesn’t count in heaven).

*Chicken Republic who?*

To make all of this work, a hack is to learn to forgive yourself. If you slip, take it as a bad day, and attack your goals with renewed vigor the next day.

Nigerians treat money like knacks; they want a lot of it, but won’t be caught talking about it. Every week, we ask anonymous Nigerians to show us their Naira Life – some will be struggle-ish, others boujee–but all the time, it’ll be revealing.

(Shout out to Refinery29’s Money Diaries for the inspiration.)

First in line is a family man who believes he’s a diehard team player.

Age: 37

Occupation: Financial Analyst

Location: Lagos

Relationship Status: Married (with two kids)

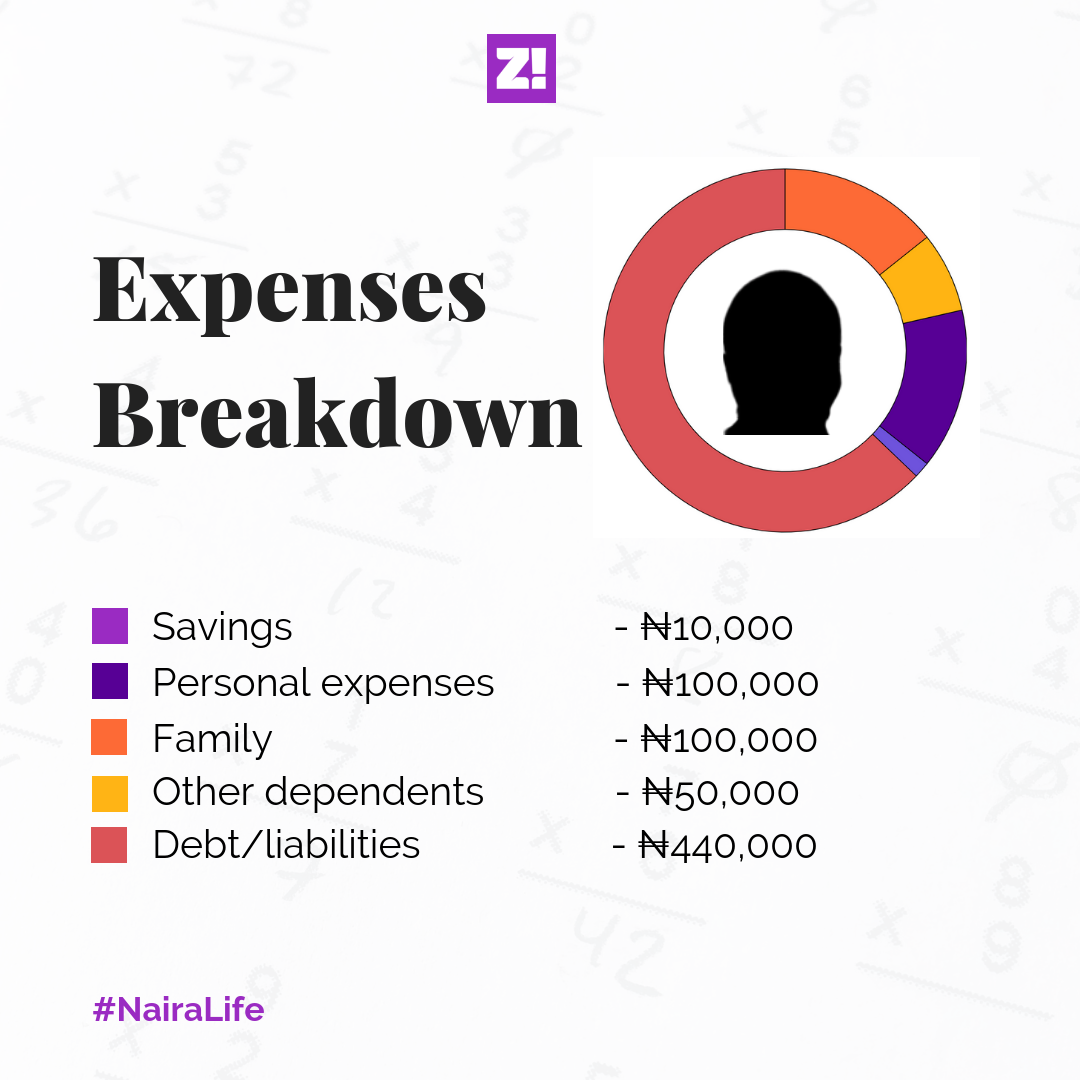

Salary: ₦700,000 (net)

Household income: ₦700,000

Rent: ₦750,000/year

What was the first salary like?

I mostly spent on people; family for the most part. I was quite traditional about it. I remember sending all of it to my mum as a gesture, and her sending it back to me. My net income at the time was ₦182k, and my annual package was ₦2.8 million. That, of course, includes bonuses and all of that. Also, this was 2010.

Less than 2% of your income goes into savings?

Yes, and that’s because the rest of my income goes into settling debts and other recurring commitments and liabilities. Also, I have this indiscipline of people asking for money and me not turning them down. Those 20 and 30k’s add up.

Investments?

None. I currently have no financial investments. I made some investments two years ago; they went bad, and I’m still paying for it. That’s where the debt came from. It’ll be completely paid in about six months though. For now, over 50% of my income goes into settling that debt.

What’s going to change about your spending when the debts are paid?

A lot more of it can now go to my family. Need to push up that family budget.

2019, almost 9 years since your first salary. What’s the annual package now?

My annual package is currently at ₦9.4 million.

How much do you feel like you should be earning now?

₦1 million. Net. I didn’t make some important switches in my career at the right time. Now, I believe you should move every 4 years max. I spent 7 years at my first job.

How much do you think you’d be earning in five years?

Using industry average, and where I currently am, I’d say somewhere between 1.5 and ₦1.8 million, net.

What do you feel like you should have had, but don’t have now?

Land. It’s just one type of investment I never really paid attention to. I just had a “never tie down capital” mentality. Most of my investments have actually brought me loss. Still, I’m not scared to take another risk.

Despite your bad investments, what are your best investments?

Definitely my certifications; the ICANs, ACAs, ACSes etc. When you work in an industry as structured as the financial industry, certifications help you stay competitive and valuable. Also, I’m kinda glad I got most of those certifications before I got married.

When do you want to retire?

You know, I used to think I’d retire at 45, but I realise now that I’m not a great businessman. It took a while to realise this, but I’m going to be working till the end, maybe 60. I’m the perfect company man; great energy, always representing, putting in the work for the team. I’m usually the person sharing impactful insights, and driving execution.

What’s your pension plan?

I don’t pay too much mind to it, but about 50-something-k goes into the pension account monthly. Currently, it holds no less than ₦4 million. It doesn’t make sense to me that I have that much somewhere–that is giving me about 7% annually but still–I can’t afford a house. I’ve done the math, and my pension is going to work best for me if I already own a house.

I imagine that the best use of my pension will be one where it helps me get a mortgage. I imagine a future where Pension Fund Managers in Nigeria create housing packages for consumers. If I have a ₦20 million pension and don’t own my house, I’m still screwed.

I inherited a mindset from my mum where I always imagined that I’d buy a house, instead of going through the trouble of building one. I was much younger, and that doesn’t seem so realistic now.

What are you long term plans at the moment?

I’ve been in debt for too long that it’s hard to see beyond it. At ₦700k, I can build a house in 3 years, because I really don’t have huge personal expenses. I’m just caught in the debt trap. At ₦700k, and with the responsibilities of family, I’d still be able to save ₦150k at least. In fact, 40% of my entire income can go into saving and investing.

What do you wish you paid attention to in 2010?

Discipline. I wish I’d began saving and investing early.

How would you rate your happiness on a scale of 0-10?

I’m really glad a lot of my happiness isn’t tied to my finances because I’d probably have high BP now. I’m totally fine. And while this might sound cliche, I have a family. I invest a lot of time in them, and it’s easy to underestimate how important this is for our future and mental wellbeing.

My head is still above water, and for that, I’m grateful.

Check back every Monday at 9 am for peeks into the Naira Life of everyday people.

If you’d love to share your Naira Life with us, tell us here. You’ll be anon, of course 🙂

Nobody ever knows how they get broke. One minute, you’re gallant, then you sneeze and you have only one thousand naira left in your account.

Just because we care, we’re here to help you figure how to stay alive in those trying times.

Plan your spending to the last dime

200 naira worth of garri. Four bags of pure water. 100 naira airtime for your phone. 100 naira for transport. 200 naira for contingencies.

Should keep you alive for a week or two.

Lock yourself inside.

Do you know what’s waiting outside? Bills. Invoices. And that woman on your street that suddenly remembers you took a crate of eggs from her on your way home from work last week.

Develop a sickness

If there’s ever been a time to be ill, it’s now. Except this is an illness that is completely within your control. It will help you avoid spending money on transport to work, and depending on how serious your matter is, you can use it to crowdfund yourself out of poverty.

Create a ‘Songs for the Broke’ playlist

Featuring everything that Brymo and Ade Bantu have ever made. Why? Because Wizkid and Davido will remind you of all the money you don’t have.

Do as little as possible

Think of it as putting your phone on airplane mode to conserve your battery. Be guided. Broke people don’t have any right to be energetic.

Please remain guided because some people are funny and that’s when they start doing somersault in their living room.

Do not eat when you feel like

Eat when real hunger is actually finishing you.

Pray.

Because at this point, only your God can help you.

Lastly, use your head properly.

Track where your money is going, so you can plan more effectively. That way, you know how to prepare better.