Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the wordpress-seo domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /home/bcm/src/dev/www/wp-includes/functions.php on line 6121 finance | Zikoko!

There are 3 things that are certain in this life – death, taxes and the presence of crypto bros on the internet. You may have likely run into a crypto bro or you may have not. Either way, consider this an introductory course into crypto bros.

Who are Crypto Bros?

Crypto bros are people who buy crypto, sell crypto or work in the crypto ecosystem. Matter of fact, if you have a crypto wallet, you’re a crypto bro. This community has a very low entry barrier but is very high stress inducing. Think of it as entering a swimming pool that is also a stream, an ocean and a dried up lake.

Without further ado, let’s meet the 10 types of crypto bros you are likely to find:

WAGMI Bro

WAGMI stands for “We are gonna make it”, so you already know this bro is always optimistic. His most used emoji is the rocket emoji. The market can be falling to the depths of tartarus and he will still be posting WAGMI. He’s pitched his tent in the crypto market and that’s where he will remain come hail or highwater.

Elon Musk Lite

Imagine Elon Musk as a Nigerian born and bred in Lagos. Now add privilege and capitalism and excess hustling and crypto enthusiasm to the mix. The Elon Musk Lite bro can be found making cryptic tweets and debating in comment sections. Best believe he owns the top 5 cryptos – BTC, ETH, SOL, ADA AND XRP. He also owns USDT and USDC. But he will never admit to owning them unless backed into a corner.

NGMI Bro

The Direct opposite of WAGMI bro, “Not gonna make it”. The moment the market dips even a little, he starts calling on the ancestors for help and dragging everybody that has ever tweeted about crypto or blockchain or web3.

FOMO Bro

Whenever new cryptocurrency is launched, this bro is right there ready to buy. He is always battling fear of missing out (FOMO) and losing. Yet, he keeps buying coin after coin, and participating in as many airdrops as he can catch.

The Whales

The Whales are the crypto big boys, they own and move crypto in large quantities. They rarely speak about crypto but they’re always at the backend moving the market. You’ll probably see them spending your annual salary on a Friday night at Zorya night club or W Bar.

The Dip Buyers

These ones wait for the market to dip then swoop in to buy coins and coins. Their motto is #buythedip come rain or shine. The bearish market is when they come alive and are most active online.

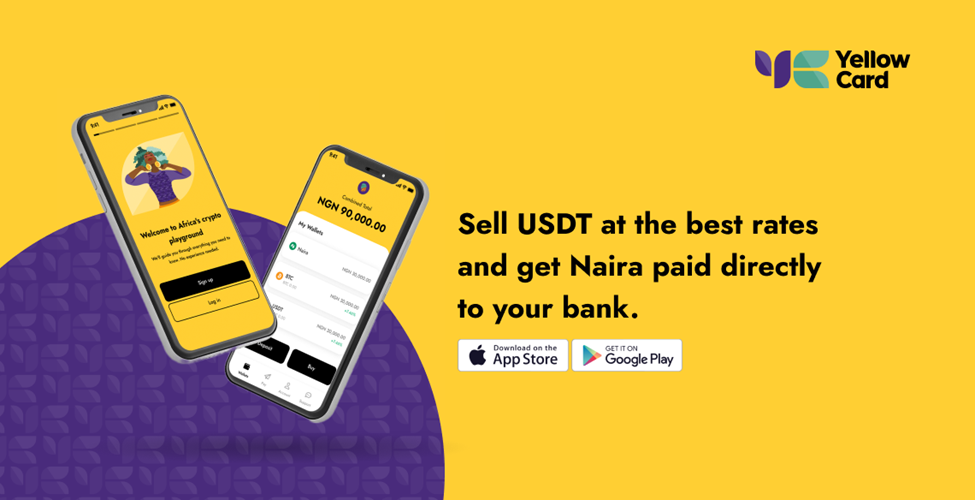

Yellow Crypto Bro

The chillest of all crypto bros. All they do is Sell USDT, introduce people to crypto and make threads explaining how to trade. If you need the best crypto memes, tips and market advice, they’re your plug. They also know where to get the best rates in the crypto market.

BTC Boys

These bros believe in bitcoin supremacy. If it is not bitcoin, they’re not interested. The amount of bitcoin they’re holding might rival that of the crypto whales.

Founder Bros

Founder bros are always building or announcing a new product or a new round of funding. Their twitter page has a nice balance of life wisdom, finance tweets and blockchain nuggets.

The HODL Bros

These bros are the no retreat no surrender of crypto. If the market likes it, it should fall to the ground, they’re not selling. It is rising to the moon? they still won’t sell.. They will hold on to their coins for dear life.

Crypto bros can be a handful, especially to non-crypto people, but they are also quite interesting once you get past all the rocket emojis and acronyms.

If you want a stress-free way to connect to the crypto community and understand how crypto actually works, join the Yellow Card community by checking out the Yellow Card blog or easily buy and sell crypto in Nigeria by signing up. Who knows, you just might become a WAGMI bro or an Elon Musk Lite.

Most of us (read: certain Gen Zers) agree that capitalism is the worst and we wish adulting didn’t come with having to work.

Still, we still get stories about people staying at jobs they hate due to various reasons and we wonder, how long is long enough to stay at one job? Is there an acceptable minimum?

Here’s what these seven Nigerians think:

“I go where the money is, abeg”

— Lara*, 28

I’m too old to be forming loyalty at another man’s business. I stay loyal to you for as long as you’re paying me. However, I don’t actively start searching for other jobs within six months of a new one, but if something interesting happens to pop up, best believe I’ll take it.

I think one year is a reasonable minimum — I can stay more than a year, but I don’t do less than that. I figure that I need that time to learn new things, make a difference and work at advancing my career. It also helps to avoid potential recruiters thinking you’re fickle and might be a waste of resources if they hire you.

I have a five-year rule, mainly because I’ve spent most of my career in multinationals, and I believe this gives me enough time to establish myself as an expert in a particular market and rise through the ranks. It also shows loyalty, and when recruiters try to poach me, they’re more likely to come with very attractive offers in a bid to get me onboard.

“I never spend more or less than two years”

— Max*, 27

Two years is my minimum and maximum duration. I’m at an age where I need to pay attention to intentionally growing my career and finances, and I believe there’s a limit to how much you can earn in one place.

For instance, a raise on a ₦120k job will probably take years before getting to ₦300k, but you can get to ₦300k immediately if you can find a higher-paying job.

“Six months should do it”

— Crystal*, 22

I don’t think anyone should want to quit a job before spending at least six months there. Sure, there might be peculiar cases where the workplace is toxic, but think about your CV. Unless you plan to remove the whole experience from your CV, it might not be a good look.

“I move whenever I like”

— Joy*, 26

I used to believe that I needed to spend at least one or two years at one job in order to build myself as a professional, but one company made me change my stance. I worked there for three months, and they never paid me one full month’s salary — they kept paying in instalments, and no one had to teach me before I left.

I think this idea of needing to stay for a particular period at one job does more harm to the employee — do I really have to endure an employer’s excesses so that I don’t “spoil my career”?

If there’s one thing I dislike, it’s job stagnation. My mentor thinks three years is ample time to demonstrate growth and contribute significantly to team goals, and I agree with him. However, if you’re no longer aligned with the company’s goals, it might be time to consider quitting, even before the three-year mark.

Another thing is — if you’re sure you’re doing fantastic work and your team or company just doesn’t recognise it or makes you feel like you’re not doing well, throw the three-year mark away and move to where you’ll be respected. Life’s too short to be managing jobs.

*Names have been changed for the sake of anonymity.

Ahead of the festive season, Stanbic IBTC Pension Managers, Nigeria’s largest Pension Fund Administrator (PFA), has unveiled the Stanbic IBTC Pension Managers Loyalty Program tagged Umatter. It is a reward scheme targeted at the customers of the PFA, to reward them for their loyalty and patronage through exclusive discounts as they shop with their e-loyalty card.

The loyalty program is available at the PFA’s partner merchants’ locations and stores across the nation. It is aimed at providing Stanbic IBTC Pension Managers’ customers with exciting shopping discounts to help them spend less and save more when they shop.Some of the participating merchant outlets are Maybrands, Café Royale, Hubmart Stores, Chocolate Royal, La Campagne Tropicana, Physio Centers of Africa, Medplus, iStore, Oriki, Launderland and Active Leisure. The discounts range from 5 to 12 percent on products and services purchased.

Stanbic IBTC Pension Managers’ partnerships with these major outlets will enable customers to seamlessly enjoy instant discounts on their purchases during this festive period, thereby making life even more easy and affordable for customers who use the Stanbic IBTC Pension Managers e-loyalty card. Stanbic IBTC Pension Managers will continue to initiate valuable programs like this that encourage people to continue saving for their retirement and building their financial future.New and existing customers can be a part of this exciting loyalty program by visiting www.stanbicibtcpension.com or calling 01 271 6000.

After “Detty December” comes “E choke” January, but that will not be your portion. If you follow these six tips religiously, “insufficient funds” will have nothing on you.

Pro tip: Number two always works.

1. Break up with your partner

You guys can make-up later, but you have to remain focused on securing the bag. Break up now, love won’t feed you.

2. Take Buju’s advice

Don’t go outside ooo. There’s debit alert everywhere. You never know where you’ll enter and your account will suddenly become minus 100k. Take heart ehn; it’s only a while. The outside is not running away.

3. Befriend your boss

Who else has the future of your account balance in their hands if not your boss? Start dusting their shoes and washing the plates they use for lunch at the office. If you don’t see your salary in January, at least you know who to fight (not us, plis).

4. Start planting what you’ll eat in January

Why spend money on food when you can harvest? See, carry hoe and watering can and transform that barren backyard of yours into a food court.

5.

Stock up on vibes and Insha’Allah

For every event, hangout or fun memory you make, keep a portion of the vibes aside for rainy days in January. It’s just thirty days, insha’Allah, you will survive.

6. Fast and pray

If people ask how come you are beginning to look thin and poor in January, tell them you are observing a special prayer and fasting period for supernatural blessings. Kabaya!

7. Lock your funds till mid January

Then throw away the key and forget you have anything called money somewhere. Your January self will thank you.

There’s nothing as annoying as slow network, errors or getting your card rejected when you need to make an important payment online.

If you’re in Nigeria, one of these 5 situations must have given you headache at some point.

1. Online shopping

After finally summoning courage to move all those items you’ve saved since 2019 to cart, paying will be another wahala. On top your own money you want to spend oh. This life.

2. Buying airtime when stranded

God help you if your car breaks down in the middle of nowhere and Tunji, your mechanic, is not on WhatsApp.

3. Paying bills

If it’s your village people working through your bank to make EKEDC embarrass you, pray against it.

4. Booking flights

Oh you think you can just up and go? Lemao. Wait till your bank falls your hand with network failure minutes before booking elapses.

5. Subscribing to Netflix

Something that you’re paying for because of Money Heist and King Of Boys, that’s how you’ll see that your card is not accepted for international payments.

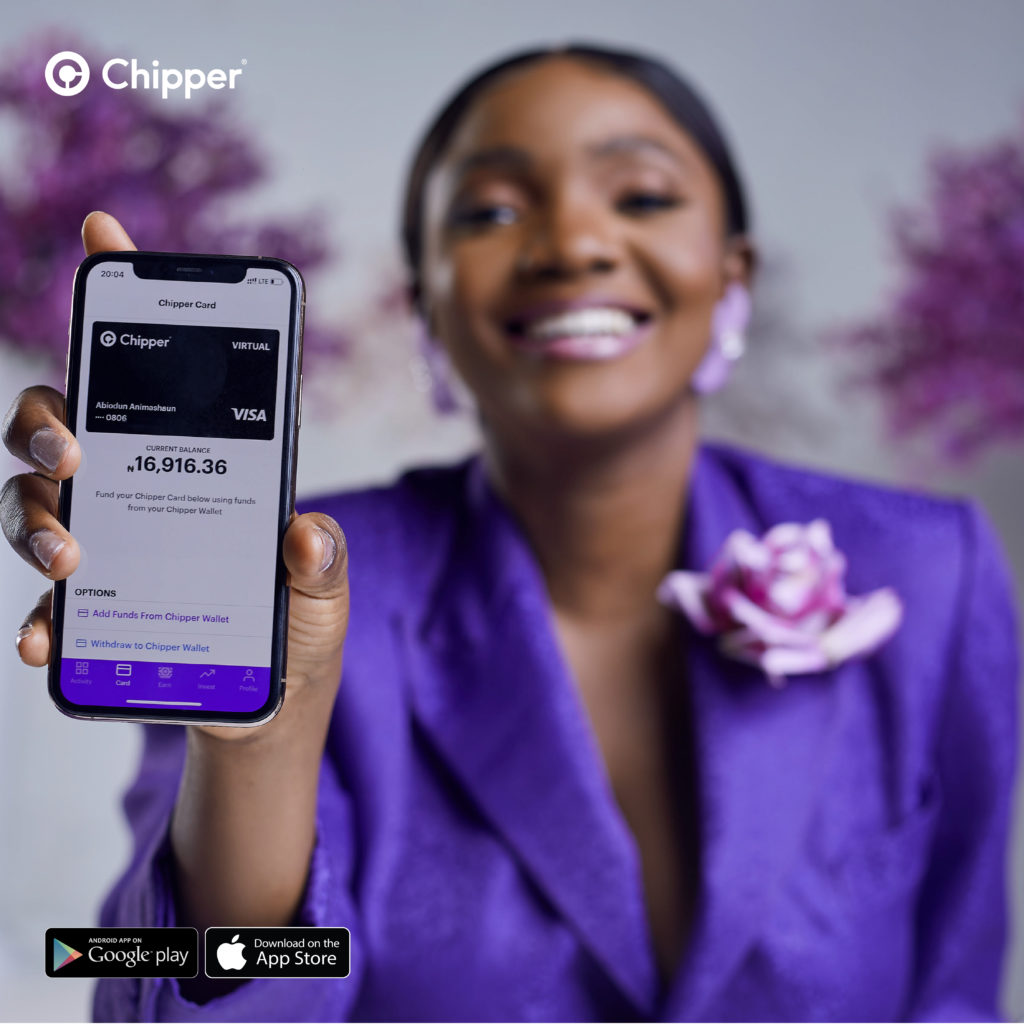

Having a virtual card like that of Chippercash can help prevent all this headache.

The Chipper Card is a pre-funded and reloadable virtual card that can be used for online payments globally. Here’s what makes it cool:

It is absolutely free to acquire.

For a limited time, you can automatically earn 5% cash back on all purchases.

You can use it for online purchases anywhere Visa cards are accepted.

Limit spending by only using the amount uploaded to your card.

Easily book flights or buy anything online.

The Merchants accepted at the moment are Ali Express, Amazon, Facebook, Bolt, Apple iTunes, Spotify, Google Playstore, BoomPlay, Youtube Video & Music, and Netflix.

The payment industry in Africa is fast rising, and as the industry continues to grow, the market is expanding and evolving despite the challenging global economic conditions. More often than not, this topic has been seen as boring, but with the recent developments, talking about it has become inevitable.

According to Statista, the total about of investment in the Fintech Industry globally since 2010 has been over $215.4 billion. This shows that the Fintech space is one that is growing and changing.

If you have ever made payment for a product or service using your mobile phone, personal computer or any other smart device, then, you are familiar with the Fintech industry as the payment industry is now commonly called.

This emerging industry may however in future, overrule the traditional banking system in Africa as Africans are gradually getting immersed in it. The payment industry has impacted many local businesses as most business owners now make use of the payment systems provided by companies known as Financial Technology (FinTech) companies.

FinTech refers to new technology that disrupts old or traditional ways of conducting financial transactions. This involves doing away with paper money and human interaction through digitized processes.

In recent times, several FinTech companies have emerged in the African payment industry. The common and widely used FinTech Companies in Africa today include Paystack, Branch, PayWithSpecta, Tala, Paga, Cellulant, Fawry, Jumo, Yoco, Zoona, MyBucks, Fluterwave etc.

These payment trends have created and are still creating both opportunities and challenges for industry players. Some of the biggest challenges include infrastructure development (especially sustainable electricity and telecommunication), low literacy levels, security and a host of others.

The different payment options available in Africa include:

Cash payment option

Check / Cheque payment option

Debit cardCredit Card

Mobile payment / Electronic bank transfers

Now, let’s look at the common terms associated with the payment or Fintech industry in Africa:

Crowdfunding: This is basically the use of capital gathered from a large set of people individually to finance a business or project. A common example is gofundme.

Chargeback: Let us assume you got debited for a product or service you did not purchase, the refund made into your account or payment card after you lodge a complaint is known as a chargeback.

USSD: It is an acronym for Unstructured Supplementary Service Data. USSD transactions occur during a particular session after dialling a code. The good thing about USSD is that it can be used on both smartphones and feature phones.

Mobile Money: In this case, your mobile phone is used to access all financial services such as payment of goods/services, money withdrawal, money transfer and more.Digital payments/e-payment: This is similar to mobile money. It is a method of making payments using digital platforms such as Paystack.

Mobile wallet: This is more like a wallet or purse but a virtual one.

Internet Banking: Almost all banks have this feature nowadays. It is the use of a web application to perform banking tasks. These days, people get to skip the line, i.e. they don’t have to queue at the bank.

It is safe to say that Fintech is the future of banking and payment industry in Africa as consumers are constantly looking for a single service that can manage all their payments in a simple, fast and secure way.

One of the biggest and best innovations in Africa currently is a platform called PayWithSpecta. PayWithSpecta combines both lending and payments into one solution. So, not only can you get credit, you can settle payments all at once without any stress or challenges.

Some of the benefits, of the PayWithSpecta platform, are;

You can pay back on installments

You can payback with a 0% interest if you pay back between 1-3 months.

You don’t have to expense cash when making payment in-store or online from any of our merchants.

You also get rewarded in cash when you refer merchants to the PayWithSpecta platform.

Never worry about getting important bills settled.

Some of the benefits of PayWithSpecta to a business are;

Citizen is a column that explains how the government’s policies fucks citizens and how we can unfuck ourselves.

After a series of lootings in Lagos State, Babajide Sanwo-Olu, the governor of the state, declared that the state will need ₦1 trillion to fix the damages incurred.

There have also been allegations of fraud and financial misappropriation against the speaker of the Lagos State House of Assembly.

Due to this, there has been public scrutiny on the Lagos State and the Lagos State House of Assembly’s disbursement of funds. We decided to break down the financial statement of Lagos State to get a true picture of the financial situation of the state.

1. Lagos State earned ₦644 billion in 2019

The total amount paid to the state for the economic value it offers is calculated as revenue.

Economic value includes the services that the state renders to its citizens and the country, from which it is paid back in taxes, allocations and other monies.

This revenue is divided into “non-exchange transactions” and “exchange transactions”.

Exchange transactions are transactions where two people buy and sell from each other. In a non-exchange transaction, there is no sale of any goods, and only one party takes from the other. An example of a non-exchange transaction is taxes and levies.

The money Lagos got from non-exchange transactions in 2019 include:

Taxation income – ₦348,001,113,000 billion .

Levies, fees and fines – ₦26,597,553,000 billion.

Statutory allocation – ₦229,495,389,000 billion.

Grants – ₦483,934,000 million.

Other revenue from non-exchange transactions – ₦3,958,723,000 billion.

Exchange transactions include:

Income from other sources – refers to money gotten from private sector development programmes, such as the Lekki-Ikoyi toll revenue, proceeds from hospital units and other miscellaneous revenues. This revenue was ₦24,014,757,000 billion.

Capital receipts – ₦8,972,888, 000 billion.

Investment income – ₦2,077,847,000 billion.

Interest income -₦1,161,184,000 billion.

The total operating revenue of the state was ₦644,762,788,000.

From the gross revenue of the state, the state spent ₦278,551,391,000 billion on expenses, leaving it with ₦366,211,397,000 billion.

The ₦278 billion expenses went to:

Wages, salaries and employee benefits – ₦107,132,214,000 billion.

Grants and other transfers – ₦16,626,164 billion.

Subvention to parastatals – ₦53,445,714 billion.

General and administrative expenses – ₦101,347,300 billion.

3. Other losses, charges and expenses amounted to ₦366 billion

After spending ₦278 billion on operating expenses, Lagos State further incurred losses in these respects:

Capital expenditure – ₦134,521,650,000 billion.

Public debt charges – ₦62,533,163 billion.

Net loss on foreign exchange transactions – (₦2,332,949,000 billion).

Depreciation – ₦104,491,678 billion.

4. Lagos State had a ₦66 billion surplus for the 2019 financial year.

After spending ₦278 billion on recurrent expenditure, and losing ₦366 billion on capital expenses, foreign exchange losses, public debt charges and depreciation, Lagos State had a surplus of ₦66,997,855,000 billion for the 2019 financial year.

5. Lagos State’s total asset is ₦2.4 trillion

Assets are divided into current assets and non-current assets.

Current assets include:

Cash and cash equivalents – ₦33,349,831,000 billion.

Receivables from exchange transactions – ₦325,268,000,000 billion.

Receivables from non-exchange transactions – ₦31,961,939,000 billion.

Inventory – ₦3,076,959,000 billion.

Non-current assets include:

Available for sale investments – valued at ₦49,665,927,000 billion .

Other financial assets – valued at ₦16,453,704,000 billion.

Property, plant and equipment (PPE) – valued at ₦2,271,309,527 trillion.

From this breakdown, Lagos State spent ₦134 billion to build infrastructure in 2019. So, spending ₦1 trillion to rebuild the state would equal the state’s capital expenditure for over six years, if we take into account the impact of inflation.

For more on Lagos State’s audited financial statements, check here.

We hope you’ve learned a thing or two about how to unfuck yourself when the Nigerian government moves mad. Check back every weekday for more Zikoko Citizen explainers.

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

When would you say you first “knew money”?

I have always wanted to be rich since I was 10. I started reading newspapers at an early age, and I learnt about MKO Abiola’s money and generosity. I would write on my school notes the number of houses I wanted to build, the number and names of companies I wanted to start, the number of chieftaincy titles I wanted to have.

My mum came from a poor family somewhere in the South West. She always prayed (and sang when doing chores) to have children that would change her fortune. Even at that age, I was gingered.

Since you remember being so driven, what was the first thing you ever did for money?

I was not really a business person. I was a book worm focused on my studies, so I could get good grades and land a good corporate job after school.

My first job didn’t come until after I graduated.

Tell me about your first job.

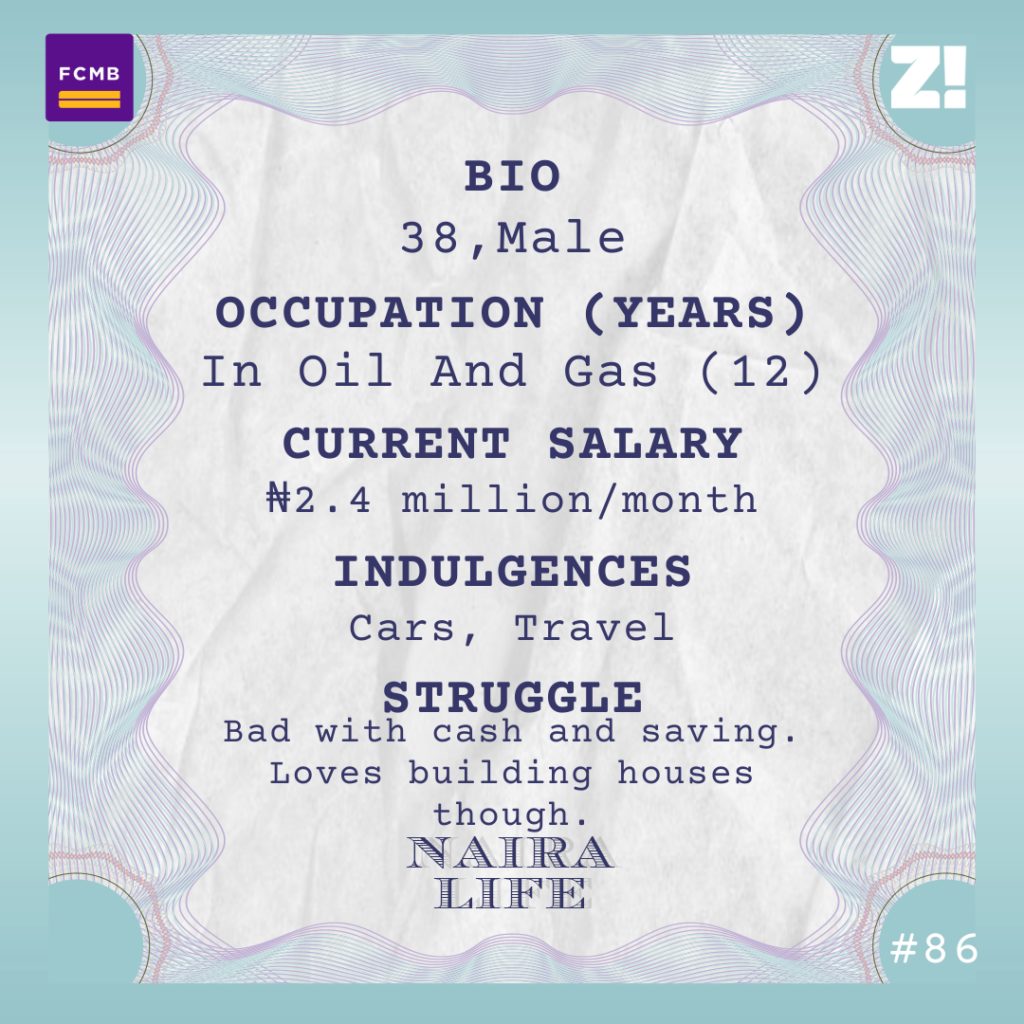

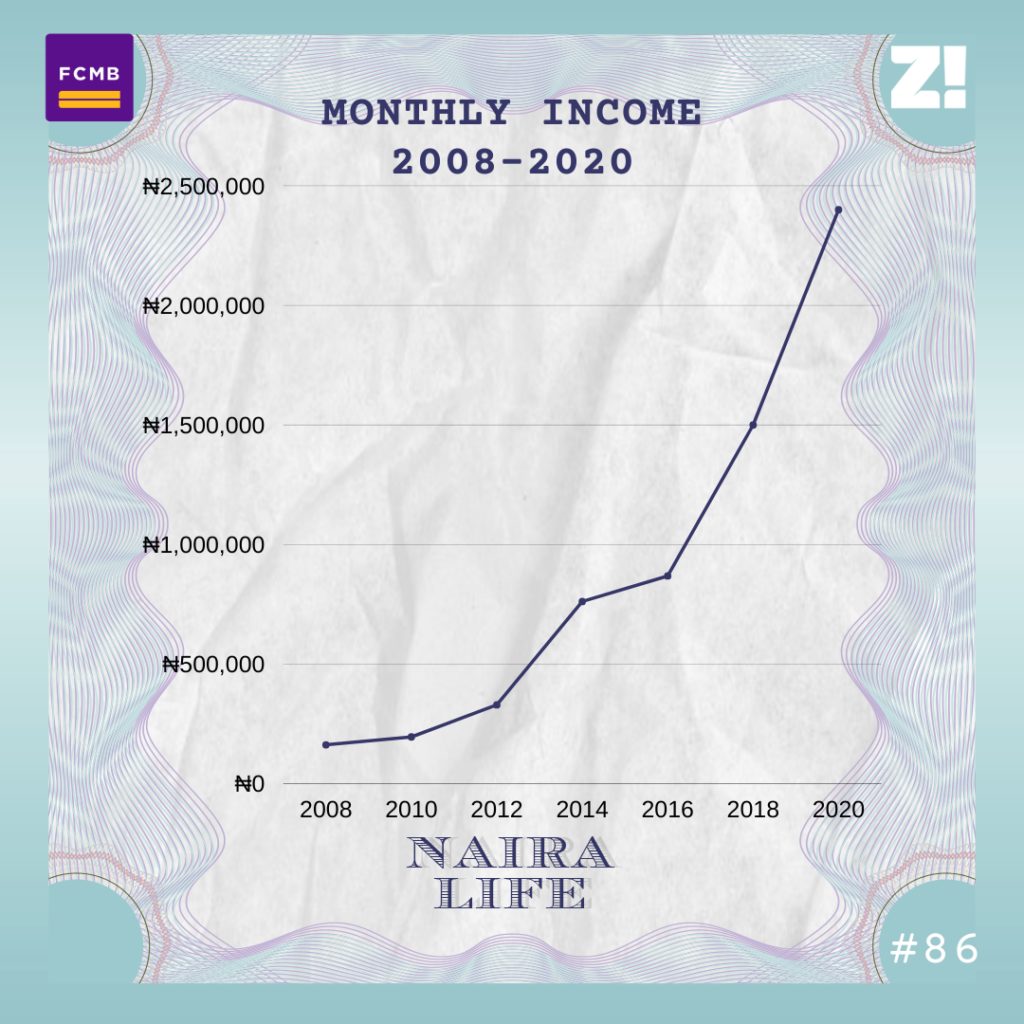

It was more like an internship at an investment management firm. I got it a few weeks after I graduated. My CV was submitted at the company by a brother. I was invited for a test, I passed, did the interview, got the job. This was 2007, and it paid ₦50k.

I got the real job after NYSC in 2008. Oil and gas. This one first paid ₦163k, then ₦196k after a few months.

What did it mean to get into an oil company in 2008?

Let me take you back to when I graduated in 2006. The economy was booming. Banks were recruiting en masse, absorbing people. Any second class upper graduate could get a bank job as long as they passed the job tests and interviews.

The capital markets operators, including the firm I worked for, were also doing well. So it was a period of boom.

Now, I must admit I was lucky. Oil and gas was not an easy industry to get into. It was and still is fiercely competitive. I remember ExxonMobil would invite entry-level candidates, and you’d see a sea of heads at a test centre. The test would hold in at least three centres. All for less than 20 slots.

My good grades really helped me. I got invited to five major international oil companies in Nigeria — Exxon, Shell, Chevron and Total Upstream. I had a shot at downstream too. The first offer I got was from one of the downstream companies a month after my NYSC. I took it and settled there. That was my launch pad into the industry.

Tell me about how your income grew from ₦163k.

By the time I left the downstream industry after four years, I was on ₦330k per month. An upstream company offered me ₦500k per month and I grabbed it. A year later, my role was upgraded and my salary rose to ₦762k. The next year, I was on ₦869k due to inflation adjustments. A couple of promotions and cost of living adjustments later, I now earn ₦2.4m after tax and pension.

Love it. Between your first salary and now, what important life events have happened?

I got married almost 10 years ago and now we have three kids. My initial plan was to celebrate my 10th wedding anniversary with my wife in Paris, but God had another plan with Corona.

Another thing, I enjoy building houses, so I would say I have never stopped building houses.

This is interesting.

I started my first housing project in 2009, and now, I have completed five houses — four bungalows and a duplex.

As soon as I finish one, I move to the next. I’m very bad at keeping cash, so I prefer to spend my money on these projects. I love decent cars too.

What’s a decent car?

Well, I’ve used a Range Rover, Land Rover and Chrysler at different points. That’s my personal indulgence. I also travel for fun.

Tell me what an average trip looks like.

I used to do Dubai every other year but got tired. I like London and Paris. I love Scotland too. I have done the major cities in Scotland — Glasgow, Edinburgh, Aberdeen and Dundee. I have done Turkey. I had fun in Istanbul, but the time spent at Hilton Glasgow was my best ever.

A typical trip lasts between 8 to 14 days. I travel economy class, but I use top hotels just for the experience. I try to use Hilton because I’m building my Hilton membership points so I can get subsidised booking.

I just love seeing the flashy modern cities. I really don’t fancy all these historical sites people talk about.

What’s on your to-do when you enter a new city?

I love football, so if there is a popular football monument in the city I’m holidaying, I try to visit. So I’ve visited the Emirates, Stamford Bridge, Old Trafford, Dundee United stadium, Wembley and Etihad.

I don’t club, so that’s out of it. I do a lot of shopping though. I buy most of my wears when I travel. TM and Zara stores are two of the first places I look for in any city. When I travel with my family, we go out in the evenings for sightseeing. When I travel solo, it’s sports monuments and shopping.

I can spend as low as ₦800k when I travel solo to one country. If I do more than one country and use top hotels, I may do up to ₦2m. With my family, ₦3m. I hardly spend more than ₦3m.

Back home here. I’d like us to break down your monthly expenses now. Let’s use your last income.

I spend about ₦1.1m on loan repayments — about ₦500k from it is actually Ajo. I have some short-term loans, banks throw loans at you when you earn that much. I spend about ₦1.5m on school fees per annum for my children plus that of a family member’s child under my care. In school fees months, I cut other expenses.

I spend about ₦100k on household stuff. I have about 10 people on my payroll, from my mum to family members. I spend about ₦100k on that. I always have an ongoing project, and I throw at least ₦300k on that. I keep about ₦200k for regular expenses — from car maintenance to gifts — during the month. I save a very little portion, less than ₦50k.

That ₦50k, hmm.

I’m very bad at keeping cash. I’ve been working for 12 years, and I can count on my fingers the months in which my salary lasted till another month. It never did when I was earning ₦163k and it still doesn’t do now that I earn over ₦2m. It’s the weirdest part of my personal finance. I used to complain, but I’ve realised there is little I can do.

How do you fund your holidays?

Several ways. But mostly from lump-sum payments, like bonuses and 13th month received towards the end of the year.

Raising ₦800k to ₦3m is not difficult by the way. Most of those expenses up there are not fixed. I may decide to not spend the ₦300k project budget for three months.

And of course, I pay school fees only thrice in a year — January, April and September.

I also stagger my travel costs. If I want to travel in December, for example, I won’t spend all the money then. I can buy flight tickets in July, book hotels in September and by the time I travel in December, all the money I need are my shopping and feeding expenses. With this planning, it’s not difficult.

Let’s talk about projects. What type of projects do you spend on?

Houses.

I’m curious about the unit economics of building houses.

They are usually small houses that cost between ₦15m to ₦30m. Three are personal. Two of the houses are commercial. I only recently finished the ones that will be commercial, so returns have not set in, but I’m hoping to get the returns in 10 years. To be honest, I did not build the houses for immediate economic consideration. I see it more as a store of value. Together, the five houses are worth about ₦100m.

I think you have an interesting relationship with money.

Well, I wish I could be good at saving though, I don’t think I have had ₦5m in my bank accounts for over a month. I realised early in my career that I am bad at keeping cash, so I decided to spend on things I could see: houses.

There’s also me trying to help people within my means because I believe I am lucky to have such a decent job. I try to have fun too, as permissible by faith. Travelling is my main indulgence. Then cars. So these are things I spend money on.

I’m poor at investments too. If I invest in liquid assets, I can easily sell them and spend the cash, hence my reservation about it.

This is not necessarily the best personal finance strategy, but this is what I do.

Has this “lack of cash” ever backfired?

A number of times. I once needed a huge sum for an unforeseen family event, and they expected me to just transfer the money immediately or after a few hours. No one believed me when I said I didn’t have cash. I had to screenshot my account balance to convince a sibling. How much? ₦400k.

What comes to mind when you think about retirement?

Relocating back to my country home in my village and enjoying a stress-free life. Hopefully, I would have built more commercial properties and rent would be a good source of income.

My pension account balance is currently above ₦30m. Hopefully, it would be up to ₦100m at retirement.

I have a small side business too; a small consulting firm that is not yet profitable.

So, I’m banking on rent on my properties, pension and retirement benefit from my employment. One of the good things about the upstream oil and gas industry is its decent retirement package.

You could go home with as much as ₦100m after 25 years of service.

I also hope my saving culture would have become better before retirement, so I should have a decent saving balance.

On a scale of 1 to 10, how would you rate your financial happiness?

I would say 8. I am lucky to have a good job that pays more than ₦2m per month. It hasn’t translated to a heavy financial chest, but I am still happy at the projects I have done. Even more, the number of people that have benefited from it.

You know, I built one of the houses for my mother. Handing it to her remains the most fulfilling day of my life.

Every now and then, your phone buzzes and you see a bank alert. In this moment, your mind races through a ton of possibilities. Is it credit alert? Debit? What do they want? Why are they messaging me if its not credit alert?

Here are 5 stages your mind runs through when you receive messages from your bank.

Credit alert

Unarguably, this is the king of all alerts. Nothing in this life beats a credit alert notification. You watch as your account balance has swollen and you start budgeting which food platter you’re going to buy because you’re forever a foodie (no need to be ashamed. This is a safe space).

Debit alert

The instant you receive a debit alert, your heart starts to race. You start thinking about your weekend and all the things you spent money on. This is where the regret starts to set in as you wonder whether that tray of small chops is really worth the heartbreak your account is going through.

Monthly account statement

I’m sure banks send this to you so that all your reckless spending in the month is laid bare to you. Cast your eyes upon your spending habits and be ashamed. You bought that mad shoe that you’ve always wanted, but at what cost? Your monthly statement will show you the cost.

Card maintenance fee

First of all, why does my card need maintenance? What exactly is the maintenance? Are they changing the engine oil in the card or what? Card that is in my wallet all month? What is the meaning of this?

SMS Notification Charge

If there’s an award for the most annoying charge, this would take the price. Because can anybody explain why your bank is charging YOU because THEY sent YOU a credit/debit alert? Lord make it make sense.

Birthday/Holiday Messages

When you realise that your bank is going to charge you an SMS notification fee for the birthday and public holiday messages nobody asked them for, your blood starts to boil. Who asked them for birthday wishes? Instead of them to send you money for your birthday.

For many young Nigerians, investing is a very treacherous undertaking. Between the tanking economy and growing responsibilities, you might find it nearly impossible to set money aside for investing. I mean, things are so bad, Shoprite is shuttering operations after 15 years. No, I’m not crying.

Back to the topic. Investing is certainly a great way to grow your finances. While saving money is nice and all, investing is a much better way to increase your wealth. One of the reasons for this is compounding.

Compound That Monayyy

Compounding interest basically means earning interest on your interest. Let’s say you invest N50,000 in government treasury bills with an interest rate of 18% per year. If you decide to reinvest your original investment and all the interest you acquire, you will receive N114,387 at the end of 5 years.

Let’s assume you decide to be disciplined and continue reinvesting your principal and interest. At the end of 10 years, you will have earned 261,691.78. While this might not seem like a lot of money, it is a great way to let your money make money for you. If you add this to the fact that investing in government treasury bills is one of the safest ways to secure your funds, you really have nothing to lose.

If you’re like the average Nigerian, you probably just set aside money for saving rather than investing. The rest is for balling. However, investing should be separate from saving. Saving is great so that you have a stash of cash for emergencies and other expenses. However, you should invest to grow your entire financial profile.

No, Seriously, You Should Invest

You should keep in mind that the reason for investing isn’t necessarily to become rich but to create a financial safety net for yourself. At some point, due to any reason, you might/will stop working. Having an investment portfolio is a great way to secure your future against what Nigeria tends to do to your personal finances.

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

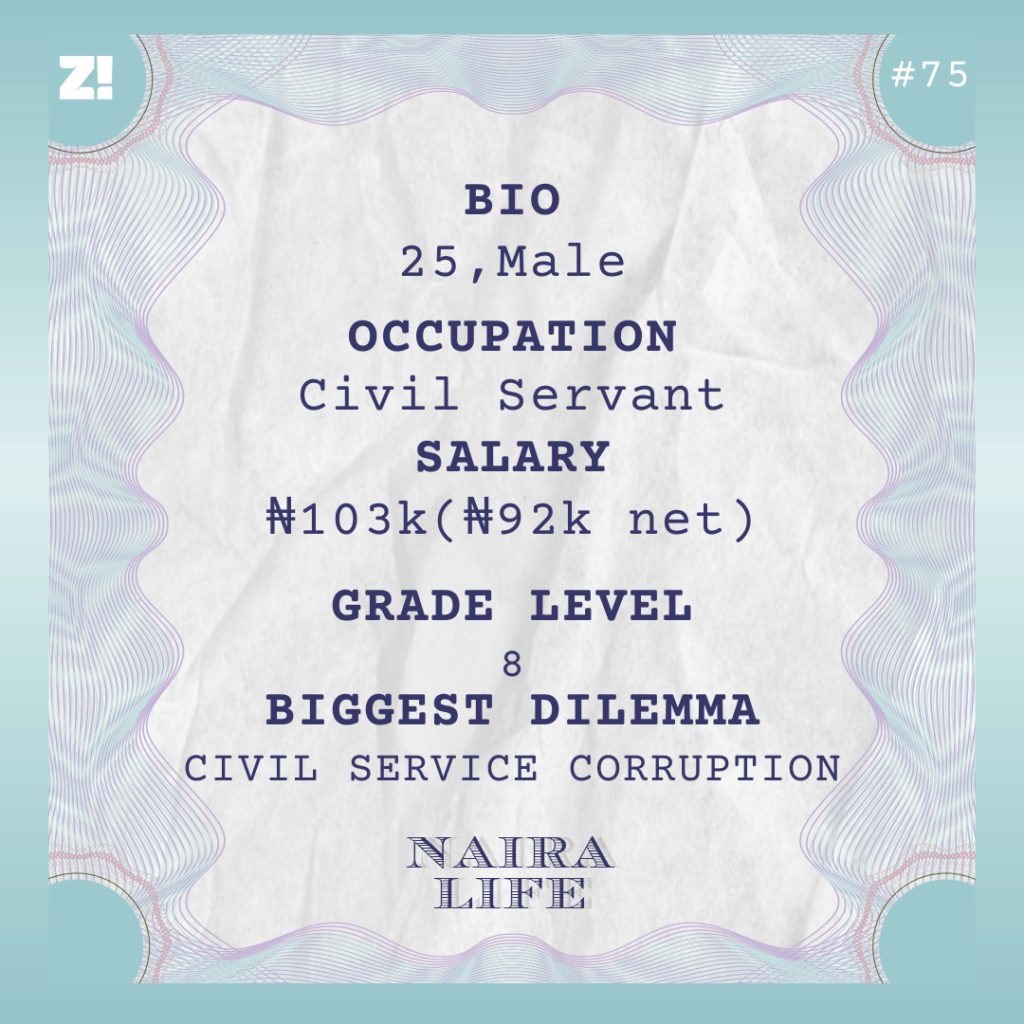

Tell me about what it was like growing up.

I was born in ‘95 in Lagos. My dad was Director of Finance in a government agency at the time. He became DG in ‘99 when Obasanjo came into office. So life was really good. I had everything I needed growing up.

We, the smaller kids had a car and a driver attached to us, we mostly just needed permission from mumsy to go chilling.

Mad o. What level do you have to be to become a director?

Level 16 in most places. I think 1-3 have been eliminated. You come in at level 4 if your highest qualification is an SSCE and you max out at 7 unless you bring extra qualification. Degree holders start at 8, MSc holders at 9, PhD/ICAN at 10.

There’s 3 years between each level up until 14. There’s no level 11.

Why?

To be honest I don’t know. At GL 12, you’re a Principal Officer; at 13 a Chief; 14 you’re an Assistant Director; and 15, Deputy Director. You can still be a Deputy Director on 16 if there’s no vacancy in the organization.

Tell me about your mum.

She was a teacher before they moved to Lagos in ‘92. That was also the year my dad became Director. She stopped working since then. My dad died in the mid-2000s. She became a businesswoman afterwards; poultry farming, buying stuff from Dubai and reselling.

Sorry about your loss man. How was it for her?

She was devastated but had to worry about us. I remember when she started the poultry. We had just moved houses in ‘07. The farm was my dad’s but it had no structures. So she built the structures and put the chickens in it. It became huge in two years but we kept having issues with the farm manager. It was always chickens dying or the eggs not adding up.

Ah, farm managers and eggs.

Sha, she sold the farm in 2011 because she said she was running at loss for like 2 years. She got around ₦15m for it.

That was when she started trading fabrics from Dubai. That lasted for about three trips over like 2 years. Since then she hasn’t really been into any business, apart from a few catering contracts from senior government relatives here and there.

How’s she been getting by?

Rental properties. We all work apart from my younger brother, the last born – he’s in his third year – so we all chip in at the end of every month. We’re 7 kids; 4 of them are now married; 1 man, 3 women; and the remaining of us, 3 boys, are at home.

7 kids. Your mum raised 7 kids?

I swear down. Big ups to her.

I’m curious about your dad’s inheritance.

From what I can remember right now; a house and 3 plots of land in Abuja, a farm in Niger State, three houses and two plots in the Northwest. I loved snooping around since I was a kid and I can remember seeing cash figures of about 70 million before they divided it. We also got $100k death insurance. It was actually the airline that paid us – he died in a plane crash.

Eish. So sorry man. What were the first things that changed financially when your dad died?

No more pocket money obviously. Our cars went from 8 to 4 – official cars were returned. We could no longer sustain 24 hours light and only used the generator overnight. Along the line, we started turning it off at 11 pm.

We had to move houses and get a smaller one – I think it was because of maintenance. The initial house was a 7 bedroom with a study and 3 sitting rooms, huge boys quarters also. We moved to a 4 bedroom with boys quarters.

Two of my siblings got married, so we didn’t need that much space.

How did it change you, personally?

Devastating. I feel I was the closest to my dad and it wrecked me emotionally even at that age. I kept wishing it was me instead of him. Financially, I didn’t feel much of the difference because my mum made sure I had all I needed.

Obviously not sleeping with gen was annoying, not getting any money weekly when I was home from boarding school was tough too. But I was quite similar to a lot of my friends so I couldn’t really complain.

My dad used to buy a lot of gifts because he travelled a lot, all of that stopped.

I was in one African country in January to collect a posthumous award on his behalf and I couldn’t hold back the tears fam. I cried on like three different occasions.

*Hug*. Let’s digress, what’s the first thing you ever did for money?

NYSC; January ’17. I was an Office Assistant in the finance department of a government parastatal. It prepared me for getting retained. I now became an accountant in the budget section. While serving, I didn’t do much work and I felt like the whole place was just dead. But when I became a staff, my boss switched up on me and work became really serious.

Buhahahaha

I dey tell you. It’s a small parastatal that feels redundant but they have revenues topping ₦7 billion per annum since 2017, so there’s a lot of work in finance. Expenditure equaling revenue as well.

So basically, no profit?

The difference is usually less than ₦20 million.

Abeg wetin dey chop this 7 billion abeg? Abeg.

The largest expenditure for the agency is transportation. And that is at the heart of the agency.

Logistics is a crazy businessman.

It takes about ₦1.5 billion. Also, there are offices in every local government. Over 1,000 in total. So fueling of vehicles and weekend allowances.

Then there’s money for Ogas too; international travel gulps over ₦100 million. Local over ₦150 million, that’s for all staff sha.

So basically, the Ogas who make up probably less than 5% are spending more than the entire workforce.

More or less. A minister used to send some of his international travel bills too.

How does this even work?

The thing was crazy o. Sometimes, letterhead approval will just come from the ministry saying the conference or whatever they’re going to relates to our parastatal. And as such, we had to cover the cost.

OLUWA WETIN DEY HAPPEN?

Guy, hahaha. This Naija ehn. I saw things and I learnt a lot while there – I benefited also. I got to save enough money to buy a car. Although my mum had to give me money from my inheritance to complete it sha.

Hold up. Tell me what you learned, and of course what you benefited.

I learned how government accounting works. I learned how approvals are passed from Director-General to Director of Finance to Deputy Director and me or my colleagues.

Any kobo to be paid has to pass through about 4 or 5 offices. Directors’ approval limit was ₦2.1m I think and the DG was ₦4m if I can remember.

What were your expectations about the civil service, and what were your realities?

I expected a dysfunctional system without accountability. Civil servants were supposed to be the same, and couldn’t care less about their jobs. I came to find out that the civil service actually works. Also, what I mean by accountability is systems like the Treasury Single Account and some internal checks. Everything that has been done can be tracked, except you don’t go looking for it.

There is just so much redundancy. Selfish people want to cheat the system all the time. For example, the accounting model doesn’t allow for any payment to be made without checks and balances but everybody along the line is ‘settled’ and thus looks the other way. External auditors come and they’re automatically expecting the same treatment too.

Anybody that doesn’t tow this line is quickly turned against and a witch-hunt starts almost immediately; I saw this first hand with a senior member of staff. She became unwilling at some point to approve the multiple payments and she claimed to have something on all of the top management.

They swung into action to find something on her and they did. At that point my morality had been so affected too that I was against her, I’m probably just realising this now.

Fascinating, your realisation that is.

Well, what can I say? She was frustrating my boss and his boss and the way it was conditioned, I couldn’t help but support them. Disloyalty is rewarded with an immediate transfer.

There are people that still manage to go home with money that is clearly not their salary, where do those come from?

So many ways o. For the big bosses, most of their illegal money comes from inflated contracts and collecting kickbacks from contractors. A 2015 Prado for example, will be bought in 2018 for ₦75 million. A car that would most likely not have cost above ₦25m.

For that to be possible, the DG, Director of Finance, Head of Audit and Head of Procurement all have to be in on it. Then the money will trickle down to the lower boys, and that makes you complicit. And in a place that spends ₦7 billion a year, you can imagine the number of inflated contracts a year.

Then we had Duty Tour Allowance or estacode as the case may be. There’s already a budget before the start of the year stating the amount to be spent on local travels and international travels. The organisation makes sure every kobo is spent, no matter how frivolous the trip. In some cases, you don’t even need to travel, as long as your boss – usually a Director – signs off that you indeed were supposed to travel. You’ll be paid without stepping out of the office.

This has happened to my face countless times.

That is crazy.

If you have something important that needs to be passed, you’ll go office by office and drop something for the boys so your paper can be passed till it gets to the appropriate office.

During internal budget defense week, I got ₦30k just for being there.

“Thank you for coming” money?

Exactly. But we were about four in my grade range. I don’t even have any idea what my bosses would get.

Tell me about the first time this thing ever happened.

During NYSC, my boss asked to see me. I went to see him that day but couldn’t because he was so busy. The next morning, an elderly colleague asked if I had seen Oga, I told him no, he said: “Ehn Oga dey find you, you no wait for am, this boy you don’t know good things.”

When I went to see him, Oga gave me ₦20k just like that. I received this about 15 times during my 2-year stay at the agency.

Crazy. How did that make you feel?

I went to tell my colleague, a level 9 staff at the time. And he said, Oga gave everyone in the division.

“Is this frequent, what is it for?” He said Oga understands salary cannot be enough and because of his benevolent nature, he helps his boys out whenever something comes in.

I reflected on whether it was right or wrong for a while until I forgot about it.

That’s heavy.

I know for a fact that it is wrong and contributes to whatever rot we’re seeing in this country. But maybe I’m saying this because I’m not eating anymore. These things are extremely hard to stop when you’re a part of them.

I had a colleague who was a very devoted Christian. She came when I was there sometime within my first year. I told her how people get money and she told me that she’d never collect money whose source she has no clue about.

Then one time, our Oga gave her 20k, but she didn’t say anything. The next day, I asked her about the money, and she was like, “how did you know?” I told her, remember that time you said you’d never collect money whose source you don’t know?

Has there ever been anyone who’s gone into this system and completely resisted?

Not a single person I know of. It actually made me start thinking twice about my dad and all of my friends’ parents in govt. Everyone I spoke to always found a way to justify it. I always come to the conclusion that my dad was a good person in office. Bad people are usually discarded after death. My friends’ parents, if you see the balling they do, it’s hard to imagine a government official getting it legit.

What level did you start with, and what level are you in now?

8, officially started in December 2017. Left the agency and went to another one from April 19 to start afresh from 8 again. The transfer process is cumbersome. So I was advised to resign and take up a new appointment. So I’ll be due for promotion 2022.

It was quite disappointing, but I did start afresh.

I still want a career in govt though, somewhere that fits my interest and skills like the Central Bank, NSIA, NDIC etc.

I’ve always had an interest in governance and I would like to contribute my skills and ideas to improve this country.

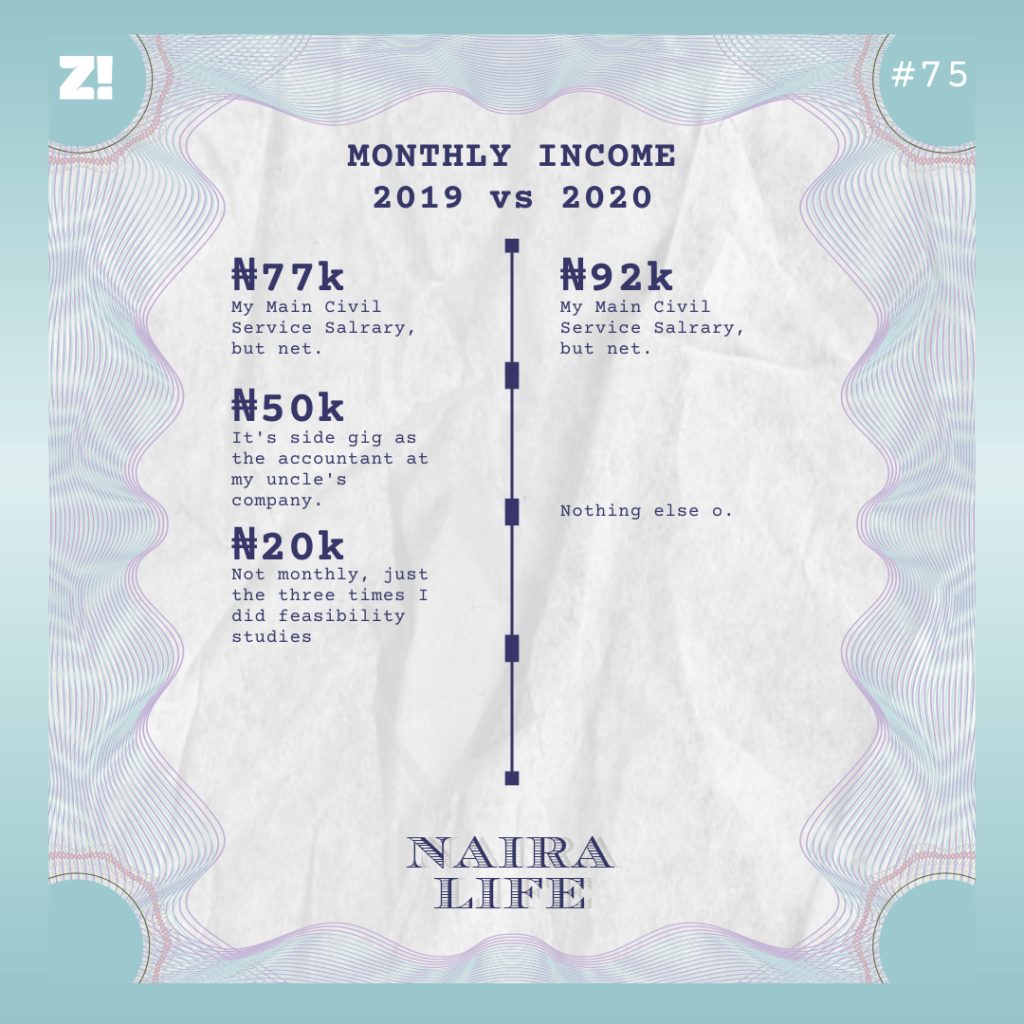

Now’s the time to breakdown your monthly income. Every dime. Where does it go, where does it come from?.

Also, what do you spend your money on monthly?

Fuel: ₦20k

Eating out (office and otherwise): ₦25k

Data: ₦9k

Miscellaneous: ₦8k (Laundry, car repairs and other stuff)

Savings: ₦30k

Do you have a monthly savings target?

2019; ₦40k. 2020; ₦30k. I’ve not missed a naira. The pandemic has helped a lot though.

How much is in your savings chest?

About ₦1.4m, $1k and the rest naira. I’m scared of putting everything in one place. Even the $ are in different forms.

Do you have insurance, pension and all of that?

I have NHIS as my health insurance, doesn’t cover everything but it’s not bad. I have a pension as well. And it’s growing nicely, love checking it every quarter. I forgot to mention, I also receive roughly ₦200k every year from rent.

From your dad’s property?

My property now.

ENERGY.

Hahaha.

What’s something you really wish you could be better at?

Making money off intellectual property. Financial consulting so to say. That’s what led me to write feasibility studies.

How would you rate your happiness levels on a scale of 1-10?

4 TBH. Alhamdulillah for what I currently have but I feel like I should be earning roughly 220 net a month at this stage. I’m still far off from that.

I would have been earning the same but my promotion would have been due December this year so technically early next year.

What’s something you want right now, but can’t afford?

In the short term, a new car. Long term; a Masters’ from a school worth going to (Salford, LSE, INSEAD etc.). In the long run when I’m vying for a management position they definitely help. There’s also the fact that I want to learn from the best. I saw my dad’s CV and I found out he had 5 international appointments. I want something like that; being good enough to hold those positions and titles.

This question helps guide whether to throw a big wedding or pay off debts and have a quiet wedding instead.

2) How are we handling the payment of bills when we get married?

Let’s be guided. Who handles what and what bill. I pay for light and water, you pay for waste and cleaning. That way everyone budgets appropriately.

3) How much money should we spend on vacations?

Are we going to Obudu cattle ranch or Santorini for honeymoon? Babe, talk to me.

4) Are we open to receiving external help from parents?

Let’s say hypothetically, daddy wants to buy us car because the old one is faulty, what’s the protocol for that? Just thinking out loud babe.

5) Do you have an emergency fund?

I know we are covered by “God forbid” and whatnot, but if shit hits the fan, is there a buffer for that?

6) Kids, how many?

Cut your kids according to your pocket size or some shit like that. We need to sit and break down the financial implications of raising one child, two children, three. etc.

7) What’s the policy with helping siblings financially?

If you help siblings, do you expect them to pay back? or is it dash? and am I supposed to chip in?

8) Named brands vs Generic brands?

I am just asking so I can know how we will be planning salary expenditure. So, I can plan accordingly.

9) If we have fertility issues, how much money are you open to spending?

I know it’s not our portion but it’s good to consider this, please.

10) Public school or private schools for our children?

This question is important because it will affect our cash flow in the future so it’s better we plan for it from now.

I spent the last two days reading about how online payment platforms work in Nigeria. Why am I so jobless you ask? I’ll explain later.

But first, if you don’t already know how card payments work, here’s the gist:

Disclaimer: This is not meant to be an authoritative guide. It’s a framework to understand what happens.

Every time “enter your card details”, how does it even work self?

First three things to know: Your bank, online payment service provider, and the financial institution of the company you are patronizing.

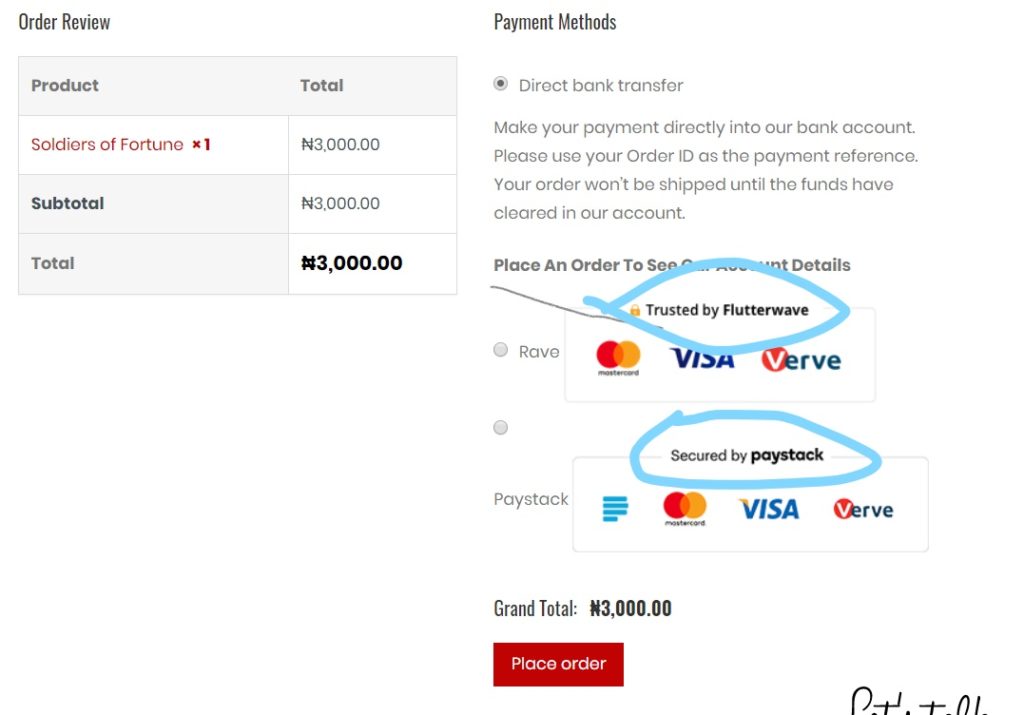

So, you decide to buy your power bank from Big Cabal electronics. They also don’t like stress and they want you to pay from the comfort of your singlet and boxers. To make both your lives stress-free, they employ the service of a payment service provider to collect the money online.

Payment service providers are like the guys who collect money from yellow buses for the NURTW but without the violence. They help businesses safely receive online payments.

Payment service providers are circled.

So, when it’s time to pay, you fill in your card details in the payment service provider’s form which is located on the seller’s check out page.

Ahan. Just like that. Is it safe?

Immediately after you fill the form, the service provider encrypts your details. Encryption is like when the smart student covers her work so we can’t copy from her in the exam. So, no one can see your details. It’s safe.

What next?

Remember when your bank people were pursuing you to collect visa or master card? or in some cases, verve card? Well, these people(master card, visa) work in partnership with banks and are in charge of issuing payment/A.T.M cards to us. So, the online payment provider sends in the covered details to these card issuers.

Because these issuers are besties with banks, they then forward the covered details to your bank for authorization. Your bank will tell them whether you can afford to pay for it or not.

How much are you having in your account?

For subsequent transactions, this whole process will be restarted from scratch as this covers only one transaction.

But…but…how does Big Cabal electronics get their own money?

After your bank says “let my people go”, Big Cabal delivers your power bank to you. You no longer miss any gist and your devices are always charged.

Your own bank then deducts the money for the power bank from your account. Pay the deducted sum into the bank of the online payment provider and they, in turn, pay into Big Cabal’s bank. All this takes a total of 24 hours to be completed.

And they transacted happily ever after…

If you enjoyed reading this, click here to learn more.

1) After saving for a long period of time and you finally check your balance:

*delayed gratification always wins*

2) You on your SafeLock withdrawal day:

3) Invest that gym money in mutual funds today or buy dollars

4) Stay at home

Don’t spend your time and limited funds hanging out with people you don’t even like that much. Stay at home and save your money.

5) The point

In this philosophical exercise, he ponders on the point of all your savings if you don’t chop life from time to time. This is because if you die, your next of kin will aggressively spend your hard-earned money on things like Ponzi schemes or even playing baba ijebu.

6) Choose yourself

You that you are always sending everyone money, who sends you money? From time to time buy yourself something nice. You deserve it.

7) Moving out advice

Once your parents start to complain that you are the one that has hidden harmattan, or that your perfume smells too nice for someone who doesn’t even pay rent. You know this is a sign to start putting money away for your own place because:

Expensive aso-ebi also falls under this category.

8) Amen

Is any Nigerian “advice” complete without a prophecy?

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

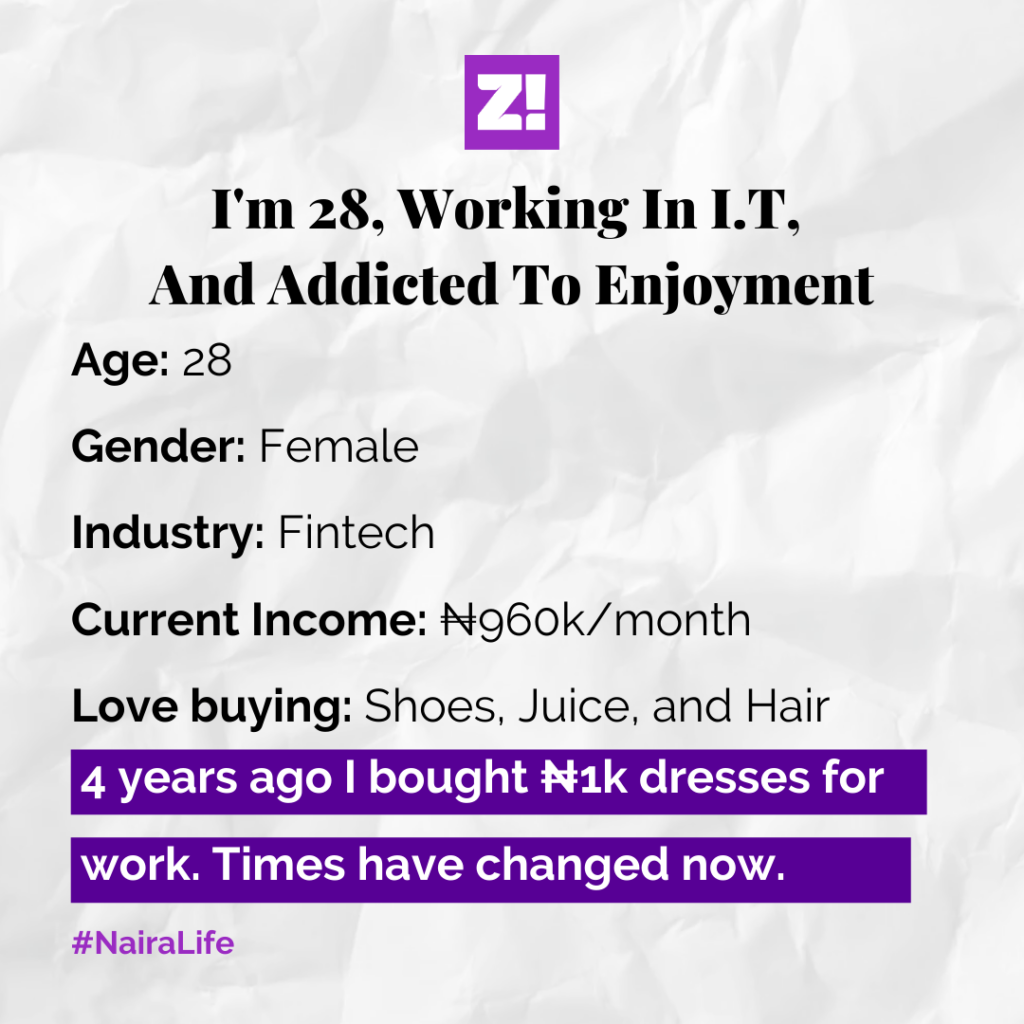

The subject of today’s story is an IT expert with a special focus on the financial sector.

What was it like growing up?

Someone once said this about me while I was in school: “Is it not that girl that used to act as if her father has all the money in the world?”

Sounds silly, but this is how I can describe my dad while I was growing up; he always provided everything we needed.

One day, I overheard a neighbour arguing with his wife and he said, “Where was your father when I was sending you to school?” And I just knew that I never wanted to be in that place that she was. I’d rather just stay in my lane, and not collect insults.

You know, my dad has one of those large families where you’re responsible for your siblings, nephews and nieces. But still, whenever we needed something, he always came through.

What was the first thing you ever did for money?

I dunno if this counts, but I was one of those people that their state governments sent on a scholarship to go to school abroad. I also got a stipend of a few hundred dollars per month – can’t remember the exact number now. My dad also sent some money every other month.

But what I’d consider my first real income was my NYSC allowee in late 2013, ₦19,800. My dad also cut me off from pocket money from his end. But my mum started giving me ₦5,000 monthly from her tiny salary – she was a teacher.

Then I had my ₦5,000 from the state government.

After NYSC?

Ah, I was waiting for my daddy’s connections to get a job. Well, I waited for four months.

Ouch.

Staying at home sucks. One time, I lied to my dad that I was travelling for a job interview, but I actually went to my sister’s school to stay in her hostel for a few days.

Then one day, someone asked for my CV.

Progress. Where?

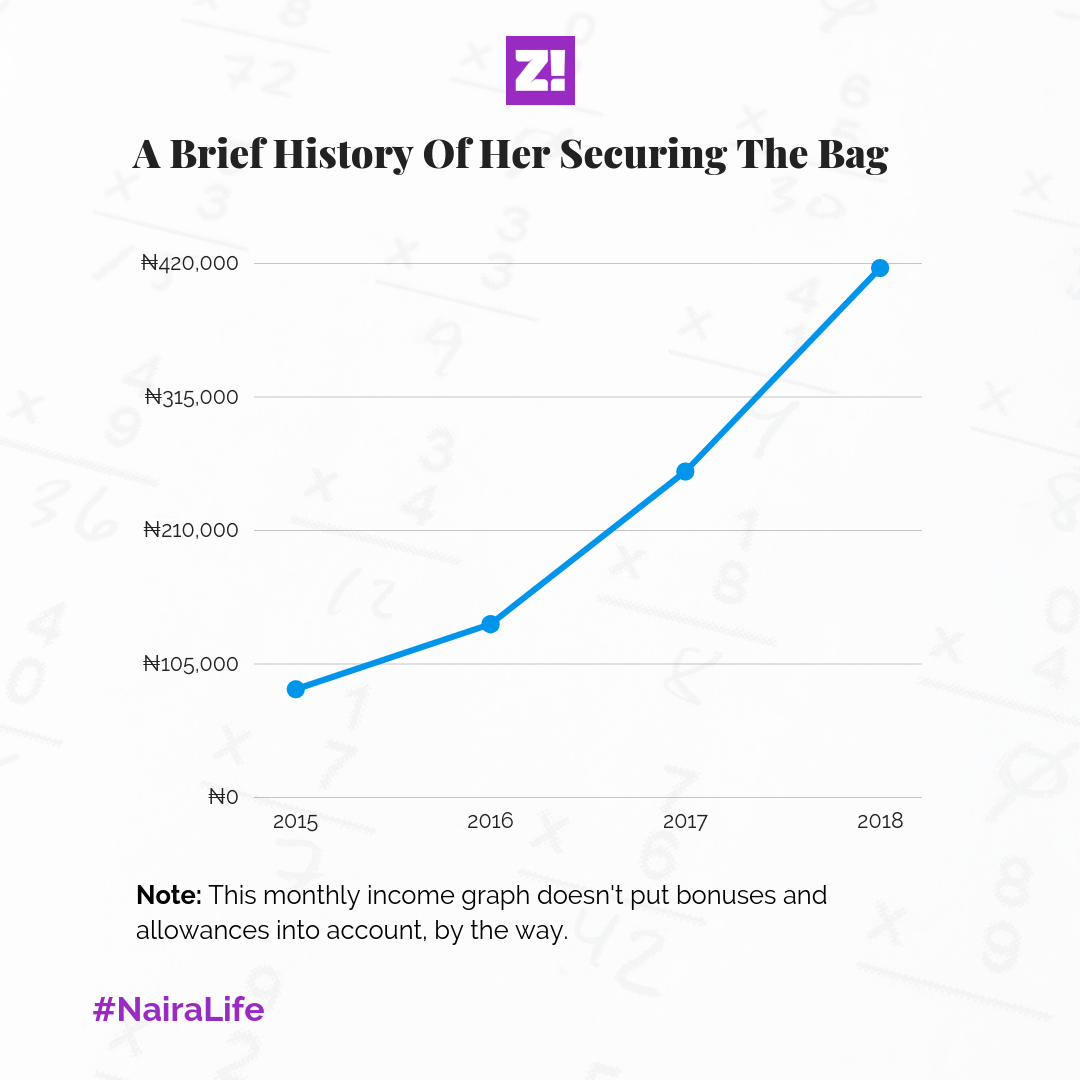

A bank. I got a call one day and fast forward to one month, I was starting as a contract staff. We got started on ₦80k/month, while a normal staff was earning ₦142k. I think contract staff are the banks’ way of saving costs.

You know what’s wild? I didn’t want to go for the interview. I thought I wasn’t good enough. It’s the same thing with the scholarship exam. I just felt I wasn’t good enough until my sister kicked me out of the house to go take the test.

At the end of the interview and training at the bank, I was the best in my batch, so I had the privilege to choose any department I liked.

I chose the IT department, of course.

So, you had to move to a new city to take this job?

Yes. I used to live outside Lagos. Moving to Lagos was hard, financially. But my dad took care of my first rent and I had my ₦80k to live with. You know, my glasses got bad in those days and I couldn’t afford to fix it. I couldn’t afford brand new clothes, so I’d go to the market to buy secondhand clothes and ₦1k dresses. I used to be scared of going to markets then, but I had no choice really.

I found solace in the promise that we were going to have our appraisals and salary reviews after one year. Over one year later, it didn’t happen.

Why?

By August, my dad said, “You are a first-class, international graduate and you shouldn’t be earning ₦80k.” He was hustling a lecturing job for me that would have paid more, and we actually fought about it, but I just knew I needed to be away from them.

We had a town hall at work, and when it was question time, I raised my hand to ask why our salary had not been reviewed months after it was supposed to. The whole discontent at the time forced me to start thinking about my options. I started studying the bank’s pay structure, and I realised that if I stuck to their growth patterns, it’d take me about a decade for me to get to about 300k+ per month.

This is super interesting.

Nothing was making sense to me anymore. But a few weeks after that townhall, our salaries were reviewed and we were upgraded to full-time staff. I got upgraded to ₦142k. Then I went to buy something.

Ohooo.

I went to buy hair. That cost me ₦45k, but I paid in instalments. This was towards the end of 2016, by the way. In mid-2017, I got a message:

Person: Hey you, are you interested in moving?

Me: But of course!

I got called for an interview. They liked my CV, and I got offered a job. I suck at negotiating, so they offered me ₦217k. Also, at the time, that felt like a lot of money.

How did that go?

It didn’t feel like a good call, but I think leaving the bank had to happen, because it pushed me to grow, and in a way, leave my place of safety. But you see that place? It was shitty and toxic.

Also, every month, they’d split the salary into two. Then pay you the other half as a lump sum at the end of the quarter – I think it was to beat tax. So while I was earning more than I was at the bank, it felt more difficult. I stayed there for three months.

Where did you go?

So, while I was working at the bank, I had someone who I might call a work big sister. She just hit me up one day, while I was still at the bank:

Big sis: How much do you earn now?

Me: 142k

Big sis: I’ll be in touch.

So, while I was at this place, she reached out and did the interview and bam. I got the job. That bam was months of uncertainties and “we’ll be in touch” etc.

Awesome. Awesome.

HR offered me ₦250k. I asked for a review, and eventually, it went up to ₦275k. I took the offer mostly because someone I respected and learned a lot from was going to be my boss again.

Was there a probation period?

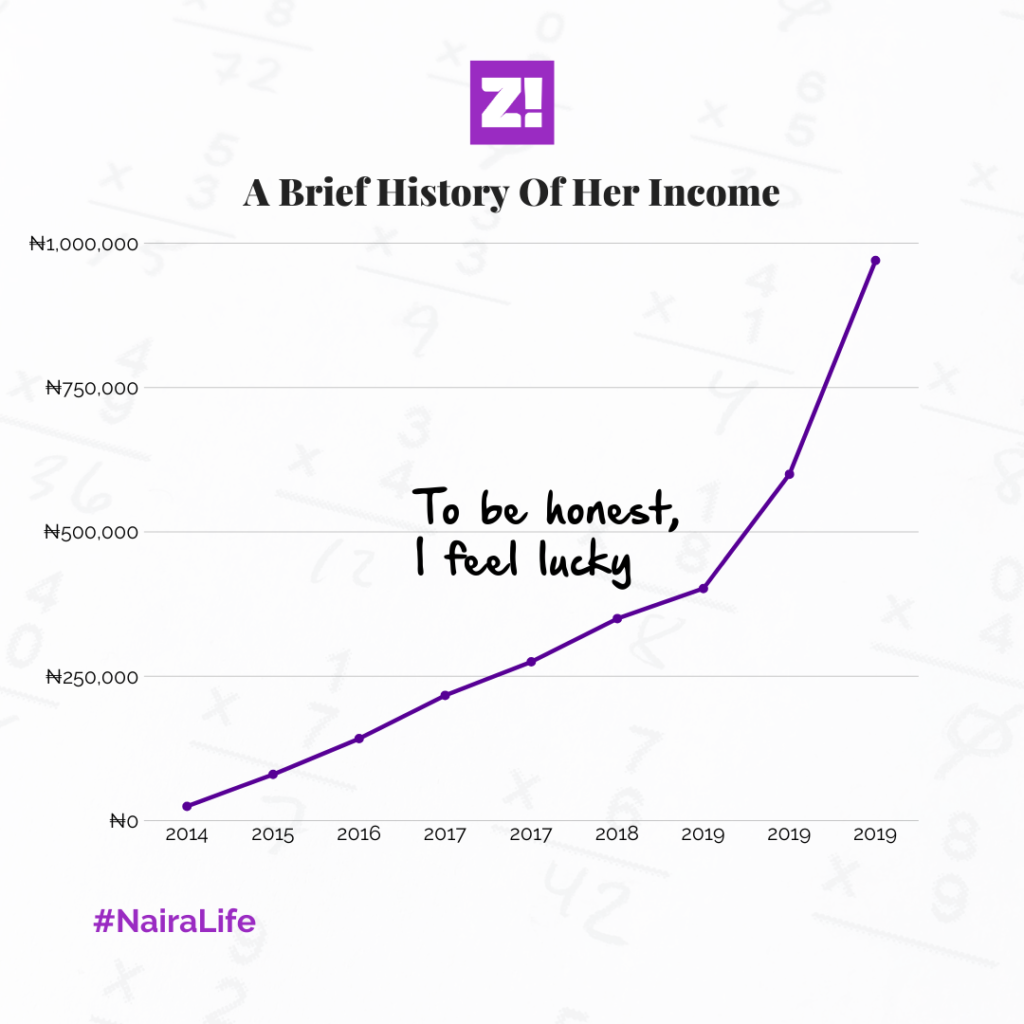

Yes yes. And six months later, I got a message saying my performance had been reviewed, and now my salary was increased to ₦350k. By the end of 2018, up again to ₦402k. And then a shocker: towards the end of the 2019, I got a raise to ₦600k.

I heard the sound of sirens in my head now.

Hahaha. But as my money increased, I felt more responsible with family and stepped up. I got a loan from work to get a place in Lagos. So even though my salary was increased, part of it had to go to repaying the loan. A few months into living at the house I got, I was going crazy.

Why?

Traffic. It was killing me so much that I literally abandoned the house. I took another loan, this time outside work, and rented another place. By the end of 2018, I took another loan. Also, I feel like I was living from paycheck to paycheck, and saving was just hard.

Then a friend of mine linked me up to a gig where they needed an I.T. person. It was abroad, and that paid $250 weekly.

Weekly money is good.

This one started in July 2019. This reduced a lot of my loan burdens. By December of 2019, I became debt-free.

It’s crazy, because in 2015, just about four years ago, you were on ₦1k dresses. How you see life?

Ahhh, I’ve grown. The day I knew I’ve grown was one time when I went out for dinner, and when my bill came, it was slightly over 10k. I just pulled out my card and paid. And I realised oh shit, I couldn’t have done this in 2015. But, I can do that now! I just got a hold of my finances, and I don’t know how my dad managed to have all that responsibility with how much he earned. He used to earn about 600k, but that dropped to about 300k, and somehow he still manages to have all the responsibilities that he currently has.

I stan. Let’s look at everything you netted in December 2019.

First, there’s my ₦600k salary. Then my 13th month; 650k. Then my $250 per week, which brought everything to about ₦1.6 million.

Now that we’ve established that, let us talk about your Detty December.

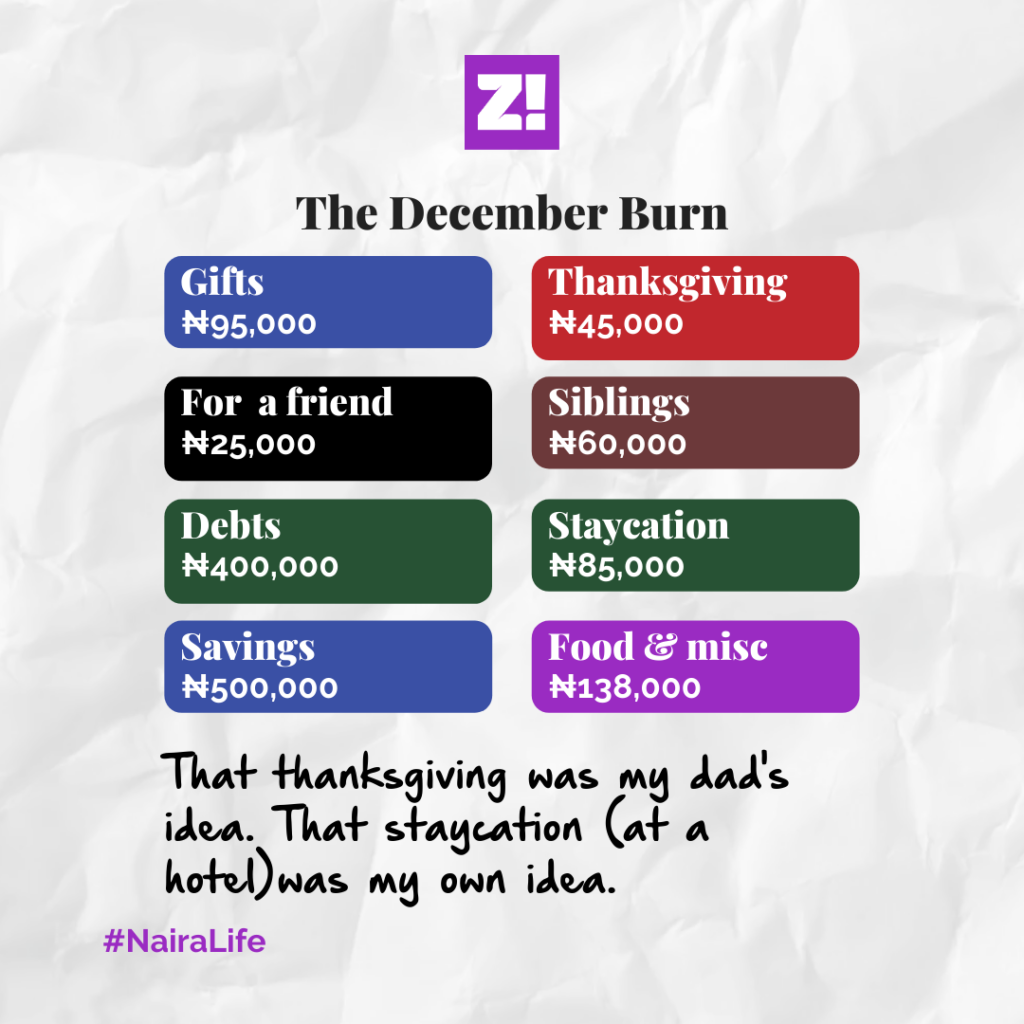

Hahaha. First of all, I cleared all my debts. All my outstanding debts were almost ₦400k. Then I did a two-night staycation; ₦80-something-k. I moved 500k to my savings. Send ₦60k to my siblings in total, as per December.

Then I kept ₦262k aside to survive the 100 days of January.

That’s almost 1.5 million.

I’ve just been buying food anyhow. Today now, I just branched somewhere and ended up buying food and juice and all that for 15k. Don’t ask me about the rest.

What’s something you want but can’t afford?

A holiday to say, Bali. I feel like I can’t afford it because I always have to go back to my savings to make big expenses like this.

What’s the last thing you paid for that required serious planning?

It was a work trip that I didn’t have to pay for. But something else happened; I dipped into all my savings and spent everything buying gifts for my family, nuclear and extended.

You can tell me how much it is now. I’m holding on tightly so I don’t fall down.

Hahaha. About a million. The first child of a Nigerian family for me means buying gifts for everybody when you travel. So shoes, bags, clothes. Add my excess luggage money to that money.

Talking about buying things, what about yourself?

Ohhh, I’m a big spender on gadgets. I must – must use the latest iPhone at every point in time. Also, I like shoes a lot.

And hair.

What’s your biggest financial regret of 2019?

I couldn’t save more. And that’s mostly because I bought a lot of shoes, and then I added weight. That meant that I had to buy new clothes. A lot of new clothes. And of course, I was no longer buying the ₦1k dresses, so that means I spent more. My average dress now costs ₦7k or so. The other time, I went to a store and bought a dress for ₦25k.

Let’s attempt to rate your financial happiness on a scale of 1-10.

I’m a 7. For someone who coasts through life, I feel extremely lucky and it just feels like God’s grace. I can’t discount the fact that I’m a hard worker though.

Despite the fact that I feel lucky, I need to get to a point where my money starts to work for me. Can’t be dipping into savings every time I want to buy basic things.

Check back every Monday at 9 am (WAT) for a peek into the Naira Life of everyday people. But, if you want to get the next story before everyone else, with extra sauce and ‘deleted scenes’, subscribe below. It only takes a minute.

Every week, we ask anonymous people to give us a window into their relationship with the Naira – some will be struggle-ish, others boujee–but all the time, it’ll be revealing.

Here: a lady who cares deeply about fresh food, tells us how she keeps her finances on a leash.

I have many first salaries. The first money I made was Uni in 2011; 300-level and I just sold something that made me ₦2,500. I remember sending part of the money to my siblings. I think I bought them airtime.

“Are you sure you have to send me this money? You need it o.” That’s what my brother said.

But anyway, my next first salary was my NYSC salary, and it wasn’t just the usual ₦19,800. My Place of Primary Assignment also paid me ₦65k.

Then to my first post-NYSC salary, my take-home was ₦136k. The annual package was about ₦3.15 mil. (Annual package is the total income earned that year, and they’ll include the money that gets taxed, paid to the pension manager and bonuses).

Where does your money go?

So first, I’m always saving. When my salary enters, my personal rule is to not touch it, until I’ve first of all looked at my budget. I have a budget on lock till December because I have projects, travel plans. So I have to know at what point I need to pay for what, and when I’ll be able to afford it.

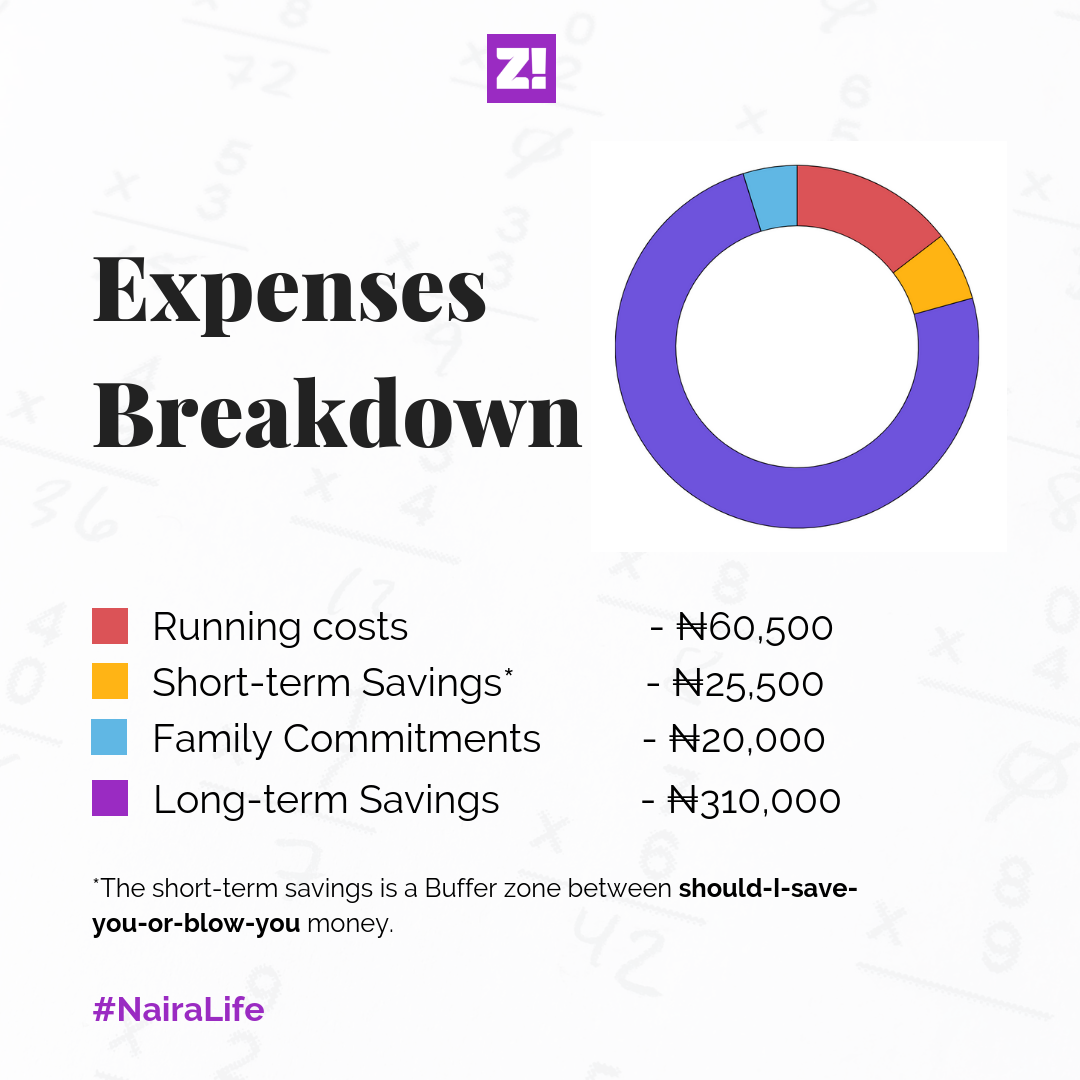

I like to think about my savings in two brackets; short term and long term. My long-term savings is about ₦310k, and it’s for the more tangible things, like investments. My short term is around ₦25k every month.

I also have to say that it’s very rare for me to save the whole long-term savings every month. It happens somewhere around once in 3 months.

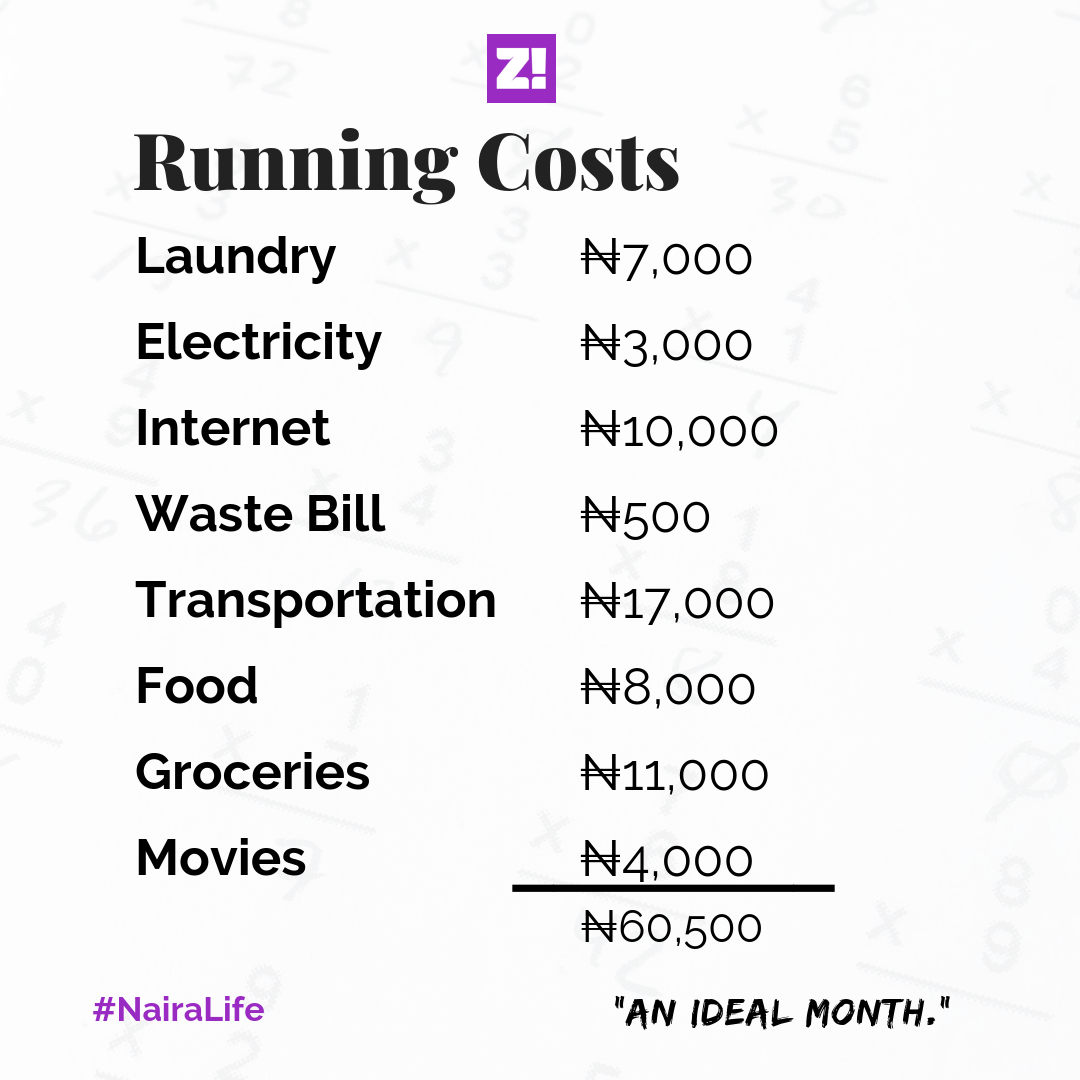

For my running costs, I don’t have a lot of expenses so I always budget about ₦60k.

This isn’t always realistic though. Sometimes, all it takes is one day of reckless grocery shopping.

When it’s looking like I’m going to be in trouble, I just pause–check my account, wallet, everything. Then I check my remaining commitments and bills for the rest of the month. I may have to adjust some things or borrow.

But as long as I’m not taking Ubers, or spending too much on food, staying super-conscious, I’m good.

What do you spend the short-term savings on?

Small things tend to pop up–like bridal showers and the occasional Aso-Ebi – like once in 3 years. I tend to be selective about the Aso-Ebi I indulge in, and it’s not even about the money. I think it’s an imposition, and it’s cancelled in my books.

But to be honest, what tends to take the bulk of my money is fresh food. Every other weekend, I might just blow like 4k. I used to have a groceries budget. Used to.

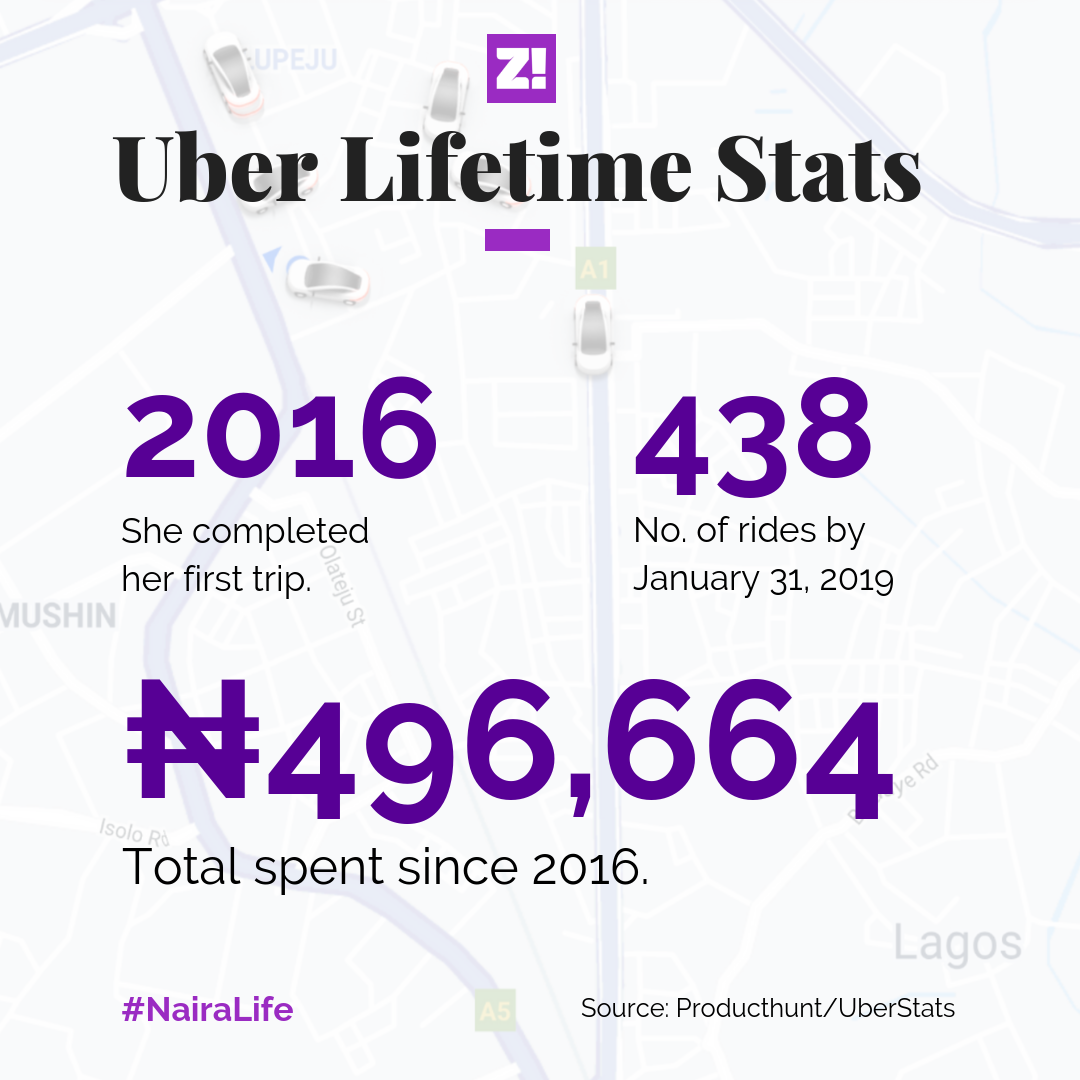

My Uber budget has almost disappeared because I have a car now. My ₦6,500 full tank lasts me for 2 and a half weeks.

I still Uber every now and then. Public transport to work used to cost me ₦400 a day, to and fro. It was actually ₦300–the extra ₦100 is for the occasional fruits I buy en route.

What do you think about what you currently earn?

I dunno, really. I never realise how little I was earning, just until I’m earning more. But I’m content with it.

What was the old job like?

It was quite prestigious. You walk into a room–any room–tell them where you work, and everyone falls in line. But it was also die-on-the-job work. It trains you to become a soldier. After 2 years, I quit mostly because I was looking for a better quality of life.

Now, I’m lucky to be at a job where I have a good quality of life and I earn good money.

Realistically, what is great money for you?

First of all, it can’t even be in Naira.

How much money are we talking here?

Bastard money. Just leave it like that.

What’s something you can’t afford but totally want now?

Property. It’s not even a want. You should always be looking to own property because you can’t be paying rent in this Lagos. But for how long will I save to buy a property of ₦30 million really?

What does your ₦250k/year rent currently fetch you?

Oh a studio apartment–one room, a kitchen and a bathroom. You know, my leave allowance used to be my rent money. My former job used to pay my leave allowance in the month rent was due.

Do you ever think about retirement?

I really haven’t thought about it, but maybe I’ll go to where rich people are, find someone to marry me, then start doing rich people things.

…

Okay on a serious note, I know the goal is to find something I enjoy doing to the point that I don’t have to retire. Currently, I’m not there yet, I’m just winging my whole career.

Once in a while, I just remember “oh, we have this pension thing!” and then I check. It was a little over ₦1.6 million at my last check.

What’s the last thing you paid for that required serious planning?

My car. All of my long term savings last year went into my car. I copped it for ₦2.9 million. My agent gave me a pretty good deal.

Tell me the most stressful miscellaneous you’ve had to pay for?

Definitely car trouble. ₦25k or so. Or when I have to fix something in the house, like the annoying plumbing that spoils overnight.

I’m constantly over-planning, so big expenses hardly catch me unawares.

So, you have an emergency fund?

Remember that 20-something-thousand? That’s supposed to be my emergency fund–in fact, I named it “Contingency” in my spreadsheet. So by the end of the month, I’m like “wait, no emergency. Oh, nice. Spend that money girl.”

Another bad habit I have is that, say I budget ₦40k for something and it comes at ₦20k, I just go yayyyyy, and then I blow the rest on food.

This financial satisfaction thing, where will you say you are at right now?

Between ₦136k to ₦416k, I think there’s a point you get to where you’re just okay. You don’t have to worry about some basic stuff–a comfort zone. So about life satisfaction, I’m content.

When did you hit the comfort zone?

I’m not sure, but the move that gave me peace of mind also gave me good money. My previous take-home when I quit was ₦256k, so it was both.

About that annoying 5-year question;

I’ve always failed this. People ask me, and they’re never satisfied with my answer. They find this hard to believe, but I’m not the most ambitious. I’m not big on ambition, but I can’t compromise on competence. I believe in cultivating competence, even if all that’s required of you is washing plate at The Place.

Career-wise, I’m totally winging it.

Let’s try this question again, but short-term.

One of my goals this year is to actively seek out investment opportunities. I did a 7-year Sukuk bond in 2017 that will give me a 16% profit. I also invested in an Online Agric investment platform in October 2018. You pay like ₦250k in stages and you get an estimated ₦100k profit.

Also, there’s the ₦50k Ajo I just do with the money I don’t really need with part of my long term savings.

When it comes, I’m balling.

You do pretty well with money.

To be honest, I think knowing where you are with money gives you power. I know what I can’t afford for the rest of the year. When I get paid, I don’t touch my money until I look at my budget. Like, I’m always rushing to my laptop to check my spreadsheet before I touch it. I also have a separate account for my running costs.

Any side hustles?

I have this one where I’ve put in a total of about ₦200k. I started last year, selling stuff online with a friend. We split the damage 50/50. We’re on our third inventory cycle, and for the first time, we don’t have to put any money into it.

3rd inventory?

Yeah, the stuff we sell. The first inventory, we put in money of course. The 2nd cycle, we put in a little less money. Then the 3rd cycle, the only reason we put in money was to increase our inventory.

How’s that going?

We sell on Jumia, and that one is pretty easy. But the Instagram part? If selling on Instagram will not teach you patience, nothing will. Constant engagement is exhausting.

I’m thinking about what you said earlier about ‘quality of life’

Quality of life for me means quiet in my head. I just want to be able to slow down, and think clearly. Not necessarily money. I remember this one night at my last job:

I’m working overnight with two other superiors. Between them is a total of 25 years of work experience. I totally respect their commitment to the work, but I know right there that I don’t want to live like that for long.

That moment was my trigger.

Check back every Monday at 9 am for peeks into the Naira Life of everyday people.

If you’d love to share your Naira Life with us, tell us here. You’ll be anon, of course 🙂

As much as Nigerians love money, they can be very clueless about it. Things like how to invest and grow your savings or manage your money efficiently can be confusing for the average Nigerian. Like how many of us even know what mutual funds means? So if you are confused about money as we are then you need to be following these social media accounts ASAP.

Tunji Andrews

@TunjiAndrews is the Lead Economist at Time, Trade and Commodities (TTAC) and a media personality. Asides his Twitter page, his show ‘The Money Business and Economy Show’ on Nigeria Info FM offers a treasure trove of financial tips.

Nairametrics

@Nairametrics is a financial literacy and business new site. Beyond the site, their Twitter page is packed full with financial advice and tips that are updated pretty regularly.

Ugo Obi-Chukwu

@Ugodre is the team lead at Nairametrics. He is also a chartered accountant with over 16 years of experience in financial management and corporate finance. So you already know he knows his shit.

Arese Ugwu

@smartmoneyarese is the author of the best selling book ‘The Smart Money Woman’. She is also the founder of Smart Money Africa, a personal finance blog that will offer you better financial advice than just there’s rice at home.

Nimi Akinkugbe

@MMWithNimi has a Bachelor’s degree from the London School of Economics and was once General Manager and Head, Private Banking and Director of Stanbic Bank. She also runs a personal finance site called ‘Money Matters with Nimi’

Moe Odele

@Mochievous is an experienced finance attorney and startup advisor. She runs a social enterprise called ‘Scale my hustle’ which helps new entrepreneurs launch and grow successful businesses.

Oluwatosin Olaseinde

@tosinolaseinde is the founder of ‘The Money Africa’. She’s a chartered account with over 8 years of experience in finance.

The Money Africa

@themoneyafrica offers insight into everything money. From financial literacy, to how to grow your money in ways that don’t involve MMM type of schemes they’ve got you covered.

Tomie Balogun

@tomiebalogun refers to herself as a millennial investment expert. And if you scroll through her Instagram page you’ll find that she lives up to her promise.

If you know any other great accounts, please share!