Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the wordpress-seo domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /home/bcm/src/dev/www/wp-includes/functions.php on line 6121 Debt | Zikoko!

Debt is just like the proverbial shege — it touches everybody. Almost everyone has had to deal with debt at one point or another, either due to money mistakes or urgent needs. I asked six Nigerians to share how they handled debt and what they learned from the experience. Here’s what they said.

I’m a mechanic, and in 2022, one of my regular customers dropped his car in my garage for repairs. His car’s AC system had issues. It wasn’t the first time his car — or even other cars — would spend the night in the garage, but that night, thieves broke into my garage and stole car parts. This customer’s engine — worth about ₦500k — was stolen.

The man refused to hear any explanation and insisted that I had to replace the engine. We finally agreed that I’d pay him ₦300k in instalments over six months. I paid twice but was broke by the third month and begged for an extension. He refused and got me arrested. I spent four nights in jail before a family member borrowed me money to pay for that month.

I still went into more debt during the remaining months because I had to keep borrowing from loan apps to meet the customer’s payment and avoid another prison episode. I finally finished paying all the money I owed to several apps in January 2024.

I don’t pray to experience that kind of situation again. I now try to be careful with the type of cars I allow to sleep over in my garage. If they steal a Benz, what will I do? I also pay for vigilantes in my street for added security. More importantly, I’m now avoiding loan apps. They’re easy to get, but the interest rates will keep you in a borrowing cycle for a long time. It’s better to ask friends and family for loans.

Charles*, 39

I was one of the people who lost their money to MMM in 2016. The worst part was that it wasn’t just my money; I had borrowed people’s money, too.

I was trying to double my profit, so I took my ₦300k life savings, borrowed ₦500k from two other people, and put it into the scheme. When it crashed, I started running away from my creditors. Omo, there’s no swear these people didn’t send to me. I kept blocking their calls, but they always used new numbers to send texts filled with swears and curses.

I only got to pay one of them back in 2019. The other person had died, and I still feel guilty about it today. It’s a bad sign to owe a dead person money. I’ve even seen the person in my dreams a couple of times. I’d have given the person’s relatives the money if I knew any of them. Unfortunately, I don’t, so I just have to live with the guilt.

The experience has taught me never to borrow money for any investment again. There’s always risk in investment, and losing money is easy.

Titi, 24

I borrowed ₦100k from my mum’s ajo contribution money to buy sneakers to sell online in 2021.

Before then, I’d been seeing people post items to sell on their WhatsApp and thought it was a good idea. I didn’t know these people didn’t own everything they posted o. They just posted pictures and only bought the items when people paid for them.

My mum kept the contribution money with me for safekeeping, and I thought I could quickly use it for business before she needed it in about six months. That’s how I bought about ten sneakers and started posting on WhatsApp. The business didn’t go as well as I’d hoped, and when the six months came, I only had ₦40k to pay.

I had to come clean with my mum, and she was very disappointed. She had to borrow money to meet up, and I eventually paid her back after some months, but I know I destroyed her trust in me. I should’ve involved her right from the start. She’d have even warned me about the foolishness of using that much money to start a business I’d never tried before.

Joseph*, 22

I used to have a bit of a gambling problem. I don’t gamble as much now, but the dumbest thing I did was gamble ₦80k out of my school fees on a ticket I thought was “too sure” in 2023.

I lost the money, and instead of telling my parents, I borrowed ₦10k from a loan app and bet it on another ticket to triple the money. I lost that one, too. I was too scared to tell my parents, so I kept going to school like everything was okay. I missed four exams because of non-payment of school fees, but I still didn’t tell anybody.

My parents only found out when the loan app called them and told them to make me repay the loan or risk going to prison. I had to tell them everything. They’ve settled the debts now, but I automatically have four carry-overs. Even me, I know I made a series of terrible decisions.

Lizzy*, 29

I went into debt in 2020 after I trusted a close friend and agreed to stand in as a guarantor for him to collect a ₦700k loan from a microfinance bank. He used the money to japa without telling anyone. We only met his apartment completely empty.

Of course, the bank came to hold me when they didn’t see him. I had to repay that loan monthly for the next two years. Thinking about it still annoys me but I know I’ll catch this “friend” one day. He thinks he’s run away, but hand will still touch him. I can’t stand in as a guarantor for anyone anymore, though. I’ve learned my lesson.

Israel*, 33

I got scammed trying to japa in 2019 and lost about ₦1m. I had borrowed that money from a friend who works at the bank with the promise that I’d repay the money once I started working abroad.

But my agent ran away with my money. I was right back at square one, and I had a debt to settle. Fortunately, my friend was very understanding and told me to pay any amount I was comfortable paying monthly. I used a year to finish repaying that money, and he never once stressed me. He even returned ₦300k to me after I finished paying.

When I later asked him why he was so relaxed, he said it wasn’t the first time I’d borrowed money from him, and I always repaid. He said, “I know this situation isn’t your fault, but I know you and trusted that you’d do the right thing”.

That left me with something. We can’t always avoid unforeseen situations like debt, but having a good reputation might just make all the difference in how your creditor treats you.

As a chronic, unapologetic onigbese, does shame not visit you?

We’ve told everyone, your partner and debtees, what to do when you refuse to pay back your debts. Obviously, that hasn’t worked, so sit down and let us advise YOU on what to do when you’ve been stung by the bug of onigbese-ism.

Break coconut on your head

You’ve refused to pay back the money you owe, so obviously, you have a coconut head. We suggest you go head to head with an actual coconut and hope the impact will reset your brain and nerve endings, and you’ll do what’s right.

PS: If you land in the hospital and you call our name, we’ll deny you like newly elected politicians deny their wicked godfathers.

Wash your head with coconut water

After the much-needed factory reset, this’ll cleanse you of all rubbish behaviour, like holding on to people’s hard-earned money simply because you can.

Print “onigbese” on a t-shirt and make it your uniform

Since you can’t stop kidnapping people’s money, buy a plain T-shirt, print “I’m an onigbese” on it, and wear it around town. That way, people already know you can’t be trusted, and the next time people want to get into business with you or you ask for a loan, they’ll know what they’re getting into and flee.

Find shame

It’s public knowledge that you can’t shame the shameless, and there’s no one as shameless as an onigbese. But please, find shame so when people start dragging your name and everything you hold dear through the mud, you can feel it and finally pay them.

Beg for forgiveness

Make a list of all the people you owe and how much you owe them, and go on an apology tour. Just make sure you take their money with you before they drag you to Kirikiri for wasting their time.

Beg the police to arrest you

Take yourself to the nearest police station and beg them to put you in handcuffs and drag you into a cell. If you’re in the cell, you won’t see the people you’re currently owing money or anyone new to owe. And hopefully, when you come out, the fear of all you endured in the cell will lead you down the right path, one that isn’t filled with debt, shame and embarrassment.

Disappear

We know you. You’re probably not going to do anything we’ve said. Just pack your bags, leave the country, make sure you lay low for the rest of your life and tell your children to get ready to break generational curses. This is because the people you’re owing will swear for you, and at least one will work.

Granted, the Nigerian government owes a shit-ton of people a shit-ton of money. Your employers probably also owe you at work, but none of this compares to the feeling of living, copulating, and doing life with a renowned onigbese that owes everybody around them money.

It’ll be okay, though; we know exactly how you should handle it.

Collect your money small small

Congratulations to you, you fell in love and became a payment plan. Sometimes, the only way to deal with the shame and pay the people your partner owes is by tricking the love of your life, taking their money, and paying their debt little by little.

Report them to their olubawi

What do you do after your partner has been dragged on the internet, your good name has been tarnished, and someone’s begged you to beg your partner to pay them for the fifth time in a row? Take the matter to their family house and table it there. You’re not the first person to fall in love. But if the olubawi and your partner share the same brain cell, then our sincere apologies because nothing will change.

Shame them

Anyone who owes another person has no shame. But for your sake, we hope shaming them works and your LOML feels motivated enough to pay their debt.

Get a savings account

This savings account won’t be taking you away from poverty, but from the shame, disgrace, and ridicule you got yourself into when you decide to fall in love with a chronic onigbese. Why? you’ll need the money in there to pay off some,if not all, of their debt.

You? Have money? God forbid. As far as your sugar plum is concerned, you’re now

perpetually resting in the arms of negative account balances and zero funds.

Leave them

Everyone and their daddy can be owing you outside, but you deserve to have a little peace in your house. So, if you can, we suggest you leave your partner before they stop staining your white and fully drag you into the mud.

Become two onigbeses in a pod

If you can’t beat them, you join them. This way, you and the love of your life can become an onigbese couple: Loved by none and shamed by many.

The Nigerian federal government is the big boy who borrows money to keep his swag alive. But how long will this go on for?

It’s probably time to sort our debts out once and for all, and we have a few ideas on how to make this happen.

Borrow from other African countries

During times like this, it’s best to get help from those close to you. We can just get other African countries to pay our debts and sort them out later. They’re our brothers and sisters, after all.

Seize the politicians’ expensive property

The Federal Government should start from the top and cut off bonuses and unnecessary expenses like lawmakers’ newspaper and wardrobe allowances. Reduce their salaries too.

Let’s use the money to pay back some of our debt. It’s a small sacrifice to make for our beloved nation.

Or let Nigerians contribute

Trust Nigerians in the goodness of their hearts to come through for the country. So seek their faces for assistance, FG. Small contributions here and there and money will complete before you know it.

Try GoFundMe

Maybe if Nigeria shouts that we’re broke and cries out to the world for help, people will come to our aid and we may sort out our debt and possibly cashout, too. It may look like a skit, but who knows where our helpers will come from?

Cry to God

For a country that’s super religious, there’s no reason why we shouldn’t let God be in charge of Naija’s finances. There’s nothing He can’t do.

Deny the debts

If all options to pay back fail, maybe all Nigeria needs to do is deny that it owes anyone money. After all, when it comes to unlooking, Nigeria is the father of invention.

Close the country and run away

If denying the debts doesn’t work, Nigeria might as well close shop and run away for a bit. When the collectors come for their money, we’ll tell them our president and the powers that be aren’t around. The citizens didn’t take out the loans, right?

Someone begs you for money. Next thing you know, you’re begging them to return it. Wild. These 7 Nigerians share their worst experience with onigbeses.

“He used my money to do wedding” — Val

Around the end of 2022, I decided to start my fitness journey. That plan included getting a gym instructor. Tell me why this instructor decided to ask me for ₦20k. I hadn’t even trained with him for up to a month, so I wasn’t sure I could trust him, but I gave him ₦10k because he claimed his mum was sick. The following week, I started calling him, but he didn’t pick up. Then I heard rumours at the gym that the silly guy took money from different people for his big wedding. Nothing was even wrong with his mum. I’m now scared of gym instructors; the guy has scarred me.

“She asked for more money after three months” — Doyin*

There’s this former colleague of mine. We weren’t exactly friends, but we used to talk now and then. She texted me one day to ask for ₦20k and said she had to take care of some important stuff. We agreed she’d pay back in two weeks, but when the time came, I didn’t hear a word from her. I texted her two days after, and she sent a voice note apologising and even asked for my account number. One week later, still nothing. She started to claim network issues. After two weeks, she finally sent ₦10k. Then, she sent ₦5k the week later. I never got the remaining ₦5k because she said someone who was owing her would send it to me, and I got tired of chasing her.

Can you imagine three months later, she came to ask for ₦50k? Must be ment.

“He took my money and disappeared” — Foyo*

I had this friend who I’d known for a few months. He texted me on Instagram sometime in August 2017 to ask for ₦5k. I can’t remember the payment arrangement, but I know he practically disappeared. I tried to call and text, but he wasn’t responding. By October, when I texted him on IG requesting my money, he said he was disappointed I’d just sprung it up on him. He stopped replying my messages, and we never spoke again. I later found out that was his thing. I no longer lend people money because I can’t fight.

“He started asking why I decided to give him money” — Jima

In 2017, I gave a friend ₦10k for his final project. I was still in school then, so it was out of my allowance. When the time came for him to pay back, he started speaking in parables, saying things along the lines of “who sent me to give him money?” We were in different universities, so I couldn’t drag him by his trousers to pay.

Precious, wherever you are, know that God will judge you.

“He asked me to return a jersey he gave me” — Linda

My friend texted me that he needed me to send ₦10k to someone; he’d maxed out his account transaction limit and was going to repay me the next day. I kept calling, but he kept posting me. From September, the next time he texted me was February. He asked me for my account number and sent ₦4k. I didn’t even say anything.

After about a year, he followed me on IG again and posted about how he couldn’t wait for God to bless him so he could bless others. I replied saying he should be sure to send my ₦6k when it happens. Can you believe he said I have a bitter heart and was trying to act smart, but I was a thief? He asked me to return the jersey he gave me three years ago if I wanted my money.

“She started giving me one-worded responses” — Chi

When I was going on my industrial training, I decided to sell my hostel bed space. A friend of mine offered to buy it for ₦20k, and I agreed. We had mutual friends, I didn’t think it’d be a problem. But the first month came with no money, and the same thing happened in the second month. After pestering her, she sent me ₦5k on the third month. I continued to text her, but she wouldn’t reply. If she managed to respond, it’d be with one word. I got tired of dragging her eventually.

“She could afford to buy clothes and change her hair, but not to pay me” — Timi*

In my first year of university, I lent a close friend of mine the ₦18k I was supposed to use to register for a compulsory course. She needed to pay some dues or so and promised to repay a week after. But when the week came, she said she didn’t have it. For weeks, she kept coming up with new excuses, even though she could afford to buy new clothes and change her hair. She eventually paid on the day of my exam. Luckily, I’d saved enough to pay for the registration in time.

*Some names have been changed for the sake of anonymity.

It’s finally salary week, and I’m so excited I could cry. Some of us just want to know what it feels like for money to enter our accounts again.

For others, salary week means freedom from the many loans taken to survive January’s 774 days.

I’m not sure what kind of salary would save today’s #NairaLife subject. He’s currently ₦2m in debt. He didn’t exactly set out to be in so much debt, though.

Just like how this #LoveCurrency subject didn’t set out to be the poor partner with a trying-to-survive career in the relationship. Love happened, and even though his 15-year-older partner can afford to spend his entire salary in one night, he tries to balance the dynamic through the power of thoughtful gifting.

Wouldn’t life be so much easier if we could all manifest as much money as we need?

In this letter:

#NairaLife: He’s 23 and on His Sixth Business in Three Years

#LoveCurrency: Cohabiting in Lekki on a ₦90k Customer Rep Salary

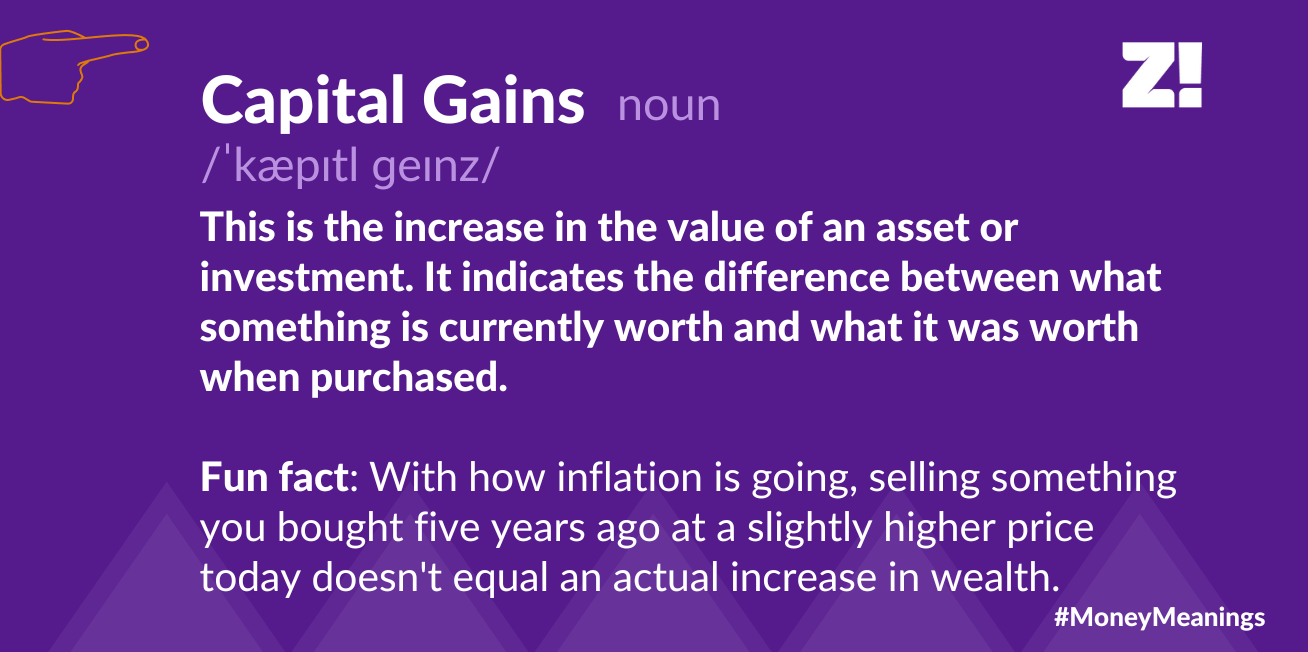

Money Meanings: “Capital Gains”

Game: #HowMuchLast

Where The Money At?!

#NairaLife: He’s 23 and on His Sixth Business in Three Years

The 23-year-old student on this week’s Naira Life started his first business in 2020. Since then, he’s tried and failed at five businesses. He doesn’t know what it is, but something keeps pushing him to try again, even though he’s now in ₦2m debt.

I want reliable information to make business and lifestyle decisions to live a Sparkling Life. I want to bank with Sparkle, because it’s digitally simple ✨

Alexei* is a 26-year-old man with a partner who’s 15 years older and earns enough to spend Alexei’s salary in one night. In this article, he shares the misconceptions about their relationship, the power dynamic and how he gets away with being poor through the power of gifting.

An excerpt: The worst happened two weeks ago. I’d sent their official driver to help me pick up a delivery, and when they came back to the house, the security guard knocked and said, “They’re looking for your daddy.”

We can’t say we’re about the money and not actually help you find the money.

So we’ve compiled a list of job opportunities for you. Make sure you share this with anyone who might need it because in this community, we look out for each other.

On January 3, 2023, the presidency announced that the 2023 budget has been signed into law, along with the Supplementary Appropriation Act. Ordinarily, news of this should prompt excitement. And it has indeed — but for all the wrong reasons.

So what’s in this budget that has Nigerians in panic mode?

A very high budget deficit

Unless you have a passion for all things finance, budgets are often very boring documents to read and when you’re compiling a budget meant to serve 200 million people, it can turn into a snoozefest.

This one’s different though. The first thing that stands out is that it has a very high budget deficit.

The budget which is themed “Budget of Fiscal Sustainability and Transition” is in fact, a joke. A budget with a deficit of ₦12 trillion cannot, by any understanding of the word, be defined as sustainable.

Let me add some context:

This is like saying as a person, all you "hope" to earn between Jan and Dec 2023 is N900k but you have laid a plan to spend N2.1million. How do you plan to survive?

Think about that and like she said, start going to INEC office to pick your PVC.

In its initial executive proposal, total expenditure was set at ₦20.51 trillion. The ratified one which was signed into law by Muhammadu Buhari has an increase of ₦1.32 trillion. This brings total expenditure to ₦21.83 trillion while revenue remains at ₦9.73 trillion.

The government has defended this increase, saying it is in response to the havoc caused by the floods that affected infrastructure and agriculture sectors. Others are sceptical, saying that the budget is being padded.

Huge debt servicing

A sizable chunk of Nigeria’s revenue in recent years has gone towards the servicing of debt. According to Bloomberg, Nigeria spent 80 per cent of its revenue to pay debt in the first 11 months of 2022. The trend looks set to continue.

More than 90 per cent of the deficit will be financed by local borrowing. Borrowing means more debt, more debt means more debt servicing which is the interest the government pays when it borrows money. ₦6.55 trillion out of the ₦21.83 trillion total expenditure has been set aside for debt servicing in 2023.

We hear you screaming omo and we are too.

In the third quarter of 2022, the Debt Management Office (DMO) put Nigeria’s debt at ₦44.06 trillion. On January 4, 2023, the Director General of the DMO, Patience Oniha, breaking down the 2023 Appropriation Act said:

“Once it is passed by the national assembly, it means we will be seeing that figure (ways and means financing) included in the public debt. You will see a significant increase in public debt to ₦77 trillion.”

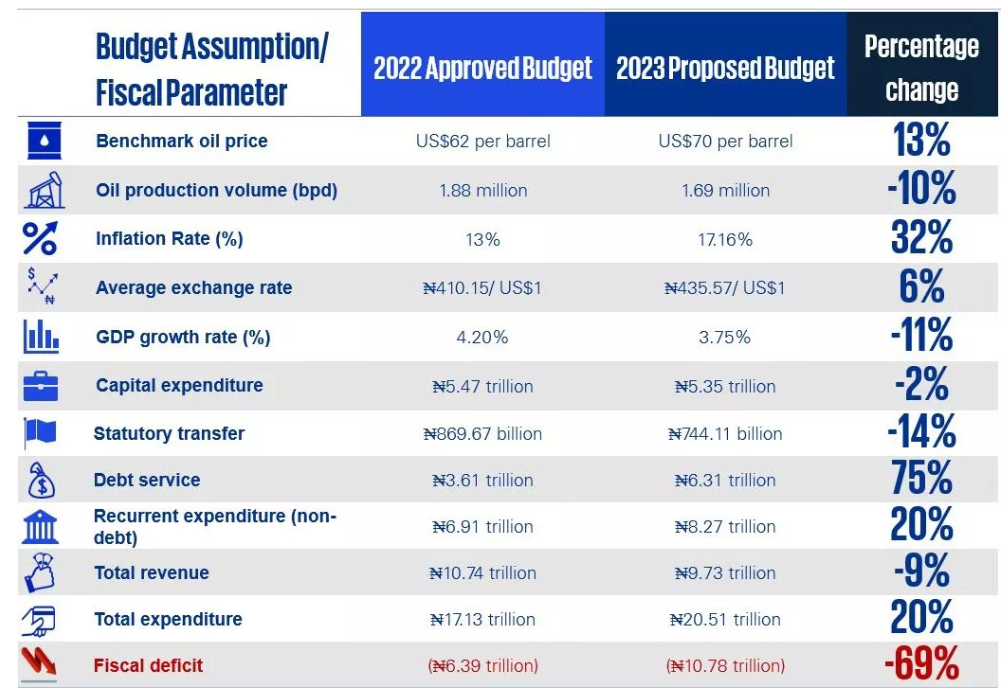

If you go through the fiscal parameters — that is, assumptions made about the budget such as what the price of crude oil will trade at, inflation rate and so on, — a couple of things stand out that should set the alarm bells of Nigerians ringing.

Based on the initial budget proposal sent to the national assembly last year, the audit firm KPMG, broke down some of the assumptions. The graphic you’re about to see makes a comparison between the 2022 and 2023 fiscal years. Check out the percentage change for each item to give you a sense of the wahala that is brewing.

[Budget Assumption: KPMG]

No one knows for sure how the 2023 election will play out as that could also affect how the budget is implemented. One thing’s certain though — whoever’s coming in has work to do, and it’s not pretty.

For many Nigerian politicians, becoming the governor of a state is the pinnacle of political success and should be the time to sit back and enjoy. That doesn’t seem to be the case for Ademola Adeleke, the dancing governor of Osun State who currently has little reason to dance.

On December 15, 2022, Adeleke alleged that the former governor of Osun State whom he defeated at the polls, Gboyega Oyetola, left ₦407.32 billion in debt.

What’s the breakdown of the gist?

Oyetola has boasted in the past that he was able to successfully run Osun State without borrowing a dime. The new sheriff in town, Adeleke, decided to check out the claim with the office of the state’s Accountant-General. His conclusion was that it was untrue. He added that a portion of the debt comes from a bridge finance facility of ₦18.04 billion which Oyetola borrowed after he lost the election in July.

GOVERNOR ADEMOLA ADELEKE REVEALED THE TOTAL DEBT PROFILE OF OSUN STATE TO COUNCIL OF TRADITIONAL RULERS IN THE STATE

“The only fund in government coffers, as of Monday, November 29, 2022, was for November 2022 workers’ salary. Otherwise, the state treasury was empty. If the ₦76 billion debts on salaries and pensions are added, the state is indebted to the tune of ₦407.32 billion. The amount owed to contractors is yet to be determined.”

Nobody likes to be called an onigbese and sure enough, Oyetola’s camp has fired back.

How has Oyetola responded?

Oyetola’s spokesperson, Ismail Omipidan, remained adamant. He responded that his boss didn’t borrow while in office. The response more or less said Adeleke didn’t know much about governance and maths. According to him, any debt claim is from another former governor, Rauf Aregbesola. The governor said there’s ₦14 billion left over in the state’s purse.

“If you go to my principal’s welfare address, he stated it clearly, that like every other state, we benefitted ₦3 billion on a monthly basis for six months from the federal government as budget support.

“This money was given to all the 36 states of the country without request. You cannot categorise that as a loan.

“So the new governor does not understand the working of government and he should have allowed those that understand the rudiment to explain it to him. So that he won’t be coming to the public to embarrass himself the way he did.”

What have reactions been like?

Some traditional rulers in the state like the Oluwo of Iwo don’t think Oyetola could have taken on such debt. Others, like the Oluwo of Kuta have said he should get on with his job since he asked for it.

“Mr Governor, you need to leave brickbats to your party and face governance. There are a lot of landmines ahead of you. You have to face governance with a view to meeting our expectations and your promise on your first 100 days in office, the days are counting.”

The days are counting indeed and Adeleke more than anyone knows this.

Ultimately, he’ll be judged on his performance, not his excuses.

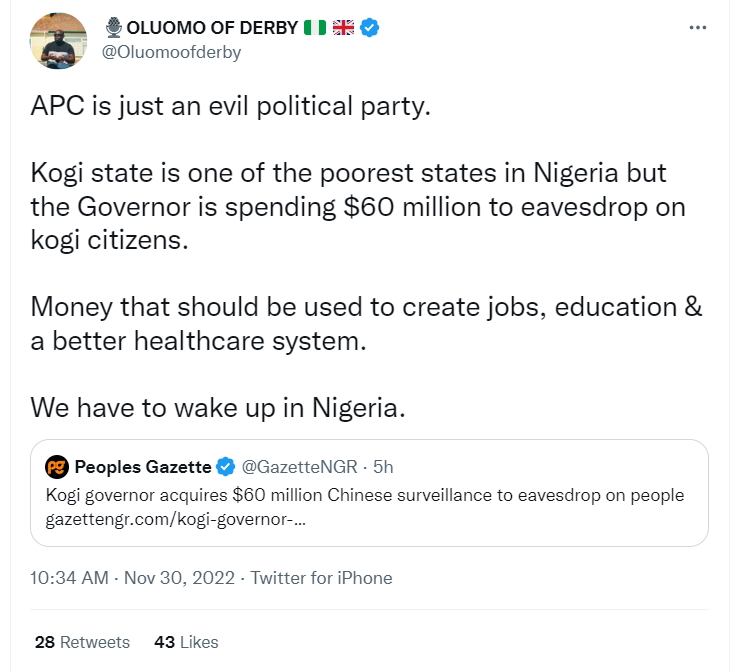

Kogi State is in the news again. Still reeling from the aftermath of a severe flooding crisis, the state government has signed an agreement with a Chinese firm, Hytera. The agreement is worth an eye-watering $60 million for a security project in the state.

What’s the project exactly?

According to the state government, the project involves the use of digital technology for real-time surveillance to prevent attacks. However, there are worries that the government plans to snoop on its residents. And if you think people are overreacting, then it’s because a Kogi State official, Abdulkareem Siyaka, said this about the project, “We’re putting the whole state on the map — real-time, virtual, audio and visual. The idea is that the moment you come into the state, we’ll see you; if you’re driving, walking or talking, we’ll be able to pick it. If you do something wrong, we’ll be able to intercept you using our field personnel on the ground.”

How’s Kogi State justifying this expense?

The Kogi government believes it needs to beef up security because it shares borders with 11 other states it has no control over. The government also expects the project to create over 685,000 jobs and attract over ₦591 billion annual investment. How it came about these figures remains a mystery.

How is Kogi funding this project?

The simple answer is debt. The state’s budget for the 2022 fiscal year was ₦145.8 billion. According to a breakdown of its security budget, ₦4,182,038,000 is marked for special security expenses, ₦9,548,000 for the purchase of security equipment, ₦90,048,000 for the purchase of security gadgets, ₦25,000,000 for federal and state security, ₦4,111,000,000 for security votes, ₦397,103,885 for security services and ₦666,429,214 in the state security trust fund.

It’s important to note that some of these funds aren’t for the benefit of everyone in the state. For example, out of the over ₦90 million allocated for security gadgets, ₦80 million of that is for high ranking members of the government.

The Hytera project costs close to ₦27 billion, when converted at the official rate, even though the state’s security allocation isn’t up to ₦10 billion. So assuming in good faith that they do spend everything in the budget allocated for security, there’s still a ₦17 billion shortfall that can only be covered by debt. And Kogi State has lots of that already with a domestic debt stock that stands at over ₦70 billion.

What have reactions been like?

Not everyone’s sold on the idea apparently.

And there’s some satire too.

Ultimately though, the Kogi State governor is answerable to the Kogi people. If they’re fine with this project, all we can do is observe and hope that it delivers on its fantastic promises.

If you’re a fan of the unifier, now’s the time to look away. The last time we brought you Atiku Abubakar-related gist, we answered the question of where he was and what he’s been up to. This time, the presidential candidate of the Peoples Democratic Party (PDP) is in a new situation: inside hot soup.

What’s the gist?

Well, Atiku had a week-long trip to the United States where he continued his campaign. The public reactions were mixed, ranging from satire to applause from his supporters who said his trip neutralised any rumours that he can’t set foot in the U.S. due to a corruption indictment.

If you think H.E Atiku Abubakar's visit to the US was a total miss and not a political master-stroke then you're a political neophyte. Peter Obi toured Europe & the United States here is a breakdown of how both men fared and what it means for the 2023 elections.

But that’s just the appetiser. The real gist is that Atiku may have accumulated an unpaid debt of $5.9 million for the US visa.

According to The Nation, Legacy Logistics LLC Limited, the firm that reportedly secured Atiku’s visa, is yet to be paid. The candidate’s legal adviser, Prof. Maxwell Gidado (SAN), has said the company is lying and trying to extort Atiku..

If Atiku really needed to prove to us he could set his foot on US soil without being arrested, it appears the cost may have been way too steep.

How has Atiku responded?

For now, it appears the unifier is keeping his mouth shut on the matter. He hasn’t yet issued any statements addressing the report, and his spokespersons are unlooking.

While people online drag him for being an onigbese, he remains focused on his presidential campaign and is expected to be in Katsina on November 5, 2022. Maybe he’d have a response for us by then.

In September 2022, the Debt Management Office (DMO) released its report on Nigeria’s total public debt stock. It had risen to ₦42.84 trillion ($103.31 billion) at the end of June 2022.

If you do the math, you’d notice that the exchange rate used is the ojoro one — the Central Bank of Nigeria’s (CBN) exchange rate. This stood around ₦414 to the dollar at the time. By October 19, 2022, the rate had depreciated to ₦436 to the dollar. Don’t even get us started on the black market rate. That’s when the true extent of Nigeria’s debt will leave you in tears.

On October 19, Oluseun Onigbinde, the director of BudgIT, a civic organisation that tracks public expenditure, raised the alarm in a tweet. He said that ₦20 trillion of Nigeria’s domestic debt would be spread over 40 years at an “unrealistic” 9% coupon rate, meaning that our debt servicing would amount to ₦1.8 trillion annually.

If all this sounds like I’m speaking Greek, let me break it down for you.

The debt profile problem

Nigeria’s debt profile can broadly be grouped into two: external and internal (domestic) debts. The external debt can further be broken down into various categories. Multilateral debt, which is the type we owe to the IMF, World Bank and AfDB, bilateral debt, which is the type we owe to foreign countries, especially China, and others like commercial debts and promissory notes.

The ₦20 trillion that Mr Onigbinde was lamenting about is our domestic debt, which is composed of different kinds of bonds and treasury bills, financed mostly by the CBN. Most of it came through Ways and Means advance, which ordinarily is something that’s used when the federal government has a budget deficit, that is, when money the government spends in a given year is more than than the revenue it receives.

In Nigeria, CBN’s statutes allow it to finance the government’s deficit at a limit of no more than 5% of the previous year’s revenue. But trust the CBN to flout its own laws by financing the deficit by as high as 80% of revenue. In the CBN’s defense, it claims it’s the Federal Government that “frustrates” it by disregarding the limits it sets.

So while Sinzu and Spending are doing their thing, our debt profile keeps mounting.

Emefiele and Buhari [Image source: Punch]

Is Nigeria’s debt sustainable?

Debt, in itself, is not a bad thing. Global debt for instance surpassed $300 trillion in 2021. Who the world is owing is a question for another day. The real question with debt is whether it’s sustainable. According to the IMF, a country’s debt is considered sustainable if the government is able to meet all its current and future payment obligations without exceptional financial assistance or going into default.

This begs the question, is Nigeria’s debt sustainable? Well, the World Bank and IMF recently said they would reassess Nigeria’s debt sustainability. In the meantime, these are the hard facts.

Nigeria is struggling with a very high unemployment rate. It’s also experiencing dwindling returns from oil, thanks to mismanagement and organised oil theft. The NLNG, another moneymaker for the economy, recently declared force majeure due to increased flooding. Even our sugar daddy, China, has stopped giving us loans.

When you add inflation, the depreciating naira, debt servicing, and an all-round struggling economy, it’s tough to imagine that we can still keep on accumulating more debt.

What’s a debt trap?

A debt trap describes a situation where a borrower is forced to take on new loans simply to repay existing ones. It occurs when debt obligations surpass one’s loan repayment capacity. Sound familiar?

Mr Onigbinde’s projection for Nigeria is that Nigeria will borrow an additional ₦10 trillion. Foreign exchange and domestic loans will stand at ₦4 trillion while the CBN prints ₦6 trillion.

By 2027, we would have acquired another ₦24 trillion in CBN debt and we would sell to the markets again, expanding debt servicing. Onigbinde calls it a “disastrous loop”, economists call it a debt trap. We should ask our elected officials many questions before we enter one.

“A Week in the Life“ is a weekly Zikoko series that explores the working-class struggles of Nigerians. It captures the very spirit of what it means to hustle in Nigeria and puts you in the shoes of the subject for a week.

For nine hours every day, 26-year-old Daisy* calls 180 loan defaulters to get them to pay up their debts. But when she’s overlooked for a promotion after two years, she starts doing the bare minimum while she figures out her next career move.

My typical day starts at 7 a.m., but I go back to sleep and wake up fully by eight most days. If I had to go to the office, I’d wake up at six and leave my house at seven. But thank God my company now lets people like me, who’ve been on the job for a long time, work from home.

I take my bath and do skin care — even though I work from home, it’s annoying that I have to use sunscreen, according to skincare experts. SMH. Then I hotspot my smartphone to my laptop and get ready to get through the day. My work is straightforward: I ask customers to pay up their gbese. I’m pretty much a call centre agent, so when a call comes to me, it’s because a customer has picked up and I’m an available agent.

I interact with customers until 6 p.m. when I log off. 5 p.m. is the official closing time, but everyone is used to working until six because, targets. If I need to take breaks, they have to be for less than 30 minutes each. But I can’t complain.

After work, I’m too tired to do anything, so I fry eggs, drink tea or order food. I don’t have time to cook a full meal because of my limited break time. I spend the rest of the night social media-ing, and catching up on texts and calls from friends, before going to bed around 11 p.m.

TUESDAY

At 8:50 a.m. when I sat at my desk to meditate before my first call today, I thought about how my target used to be 150 calls per day. It soon increased to 160. As the company continued to expand, they increased the loan collection targets till I was making 180 complete calls per day — a complete call means I dialled, the customer picked, and I introduced myself: “Hi, my name is Daisy. I’m calling you from [insert company name].”

The day flies by as I take call after call and try to keep my cool because I’m not a very patient person. Word on the gossip line is the company has struggled to raise funding recently. It seems the company’s runway is depleting, and so, there’s serious pressure to recover as much money from debtors as possible.

My company used to outsource loan collections to an agency I worked for, but during COVID, they terminated the contract, and I got laid off. Then I applied to join the company’s in-house collections team and got in. At first, I was a high performer, hitting my targets and winning departmental awards. But after personnel changes and reviews, the workplace became toxic.

The turning point was when I got passed on for a promotion. As one of the founding members, I’d been recommended by a team lead and even worked in the marketing team temporarily. I was enjoying my new role upstairs, and for three weeks, I thrived. Then HR came from nowhere and said they weren’t aware of the arrangement, and they’d already hired two people for the role. They sent me back to the loan collection team. I was devastated. Since then, I’ve been on autopilot.

They made things worse by encouraging competition to the point of toxicity. People would come to work from 7 a.m. to 6 p.m. because the more calls you make, the higher your chances of recovering money. All this just so they could meet targets and get paltry bonuses. I did it for a while and would earn an extra ₦45k here or ₦60k there. But the payment didn’t match the effort.

That’s why they’re expanding the loan collection team from the current 65 people to 100 by the end of the year. So I expect the targets to keep increasing. Things are bad, and the economic downturn in the country means people aren’t making enough to pay back their loans. This makes the work much harder for us, and we’re scared of being laid off.

WEDNESDAY

Omo. Today, I lost my shit. I understand people are struggling, but please na. I already hate when they assign me late buckets — people more than one month overdue — but this guy who’d defaulted for 35 days and counting was still doing anyhow. I’m supposed to ask why they’re delaying payments, and then, figure out a way to get them to “drop something”.

But this guy hadn’t shown any commitment, by making a part payment or even extending his loan. So I told him, “How much can we get from you today, Mister man?! Me too, I used to borrow money na. What’s all this?”

I get the late bucket customers because I’m one of the more experienced people on the team, but nobody pays me for the extra stress. Loan defaulters can be so annoying. They feel like we debt collectors can’t do anything because the company’s penalties are lenient. We only charge them a tiny percentage in late payment fees for a week, and then, we attempt to auto-debit their accounts. But these sneaky people leave their accounts empty.

What we do is flag them as credit defaulters, but most ordinary Nigerians don’t even care. Only those trying to leave the country or who need good credit scores to run businesses do. But those kinds of people rarely default on their loans.

When I’m introducing myself to customers, I have to prepare myself because, depending on their mood, conversations can go south very quickly. Sometimes, it’s difficult to stick to the script.

I’m not proud of going off on that guy today. But sometimes, when they start moving mad, I want to give it back to them hot-hot. Our calls are recorded, and my quality assurance (QA) score will surely take a hit, but we move.

THURSDAY

Today, there’s gossip going around that the company’s trying to review the bonus structure again, but I don’t even care. The base pay for my role is ₦110k monthly. Just as recently as three months ago, people got up to an extra ₦80k if they met three key performance indices (KPIs): QA score, output and recovery.

The old system was something like this: If my team calls 1m customers, we’re supposed to recover at least 70% of the debt. If I call 3k customers in a month and they were owing ₦3m, I must recover at least 70% of the money. If I hit my 70% target, and my team meets its 70%, it means I’d meet the recovery KPI.

I also need a QA score of 90%, which is measured by following the call script, being empathetic, maintaining a certain tone of voice and requesting complete or part payments. This has been my biggest issue as I usually score between 82% and 89%. I don’t care about customers’ reasons for defaulting payment. Just pay the money you owe.

Before my first short break at around 1:30 p.m., I called a debtor, and before I even finished introducing myself, she’d started shouting, “Ahn ahn! I already told you people I don’t have any money. Please please please, you people should let me rest. Your colleague called me yesterday and the day before yesterday. Why will you be calling somebody every day?”

Wait o, am I not supposed to ask them for the money they promised to pay? Shey she dey whyne me ni? Is she the only person who’s ever borrowed money? What kind of nonsense is this na? When I dropped the call, I knew I was going to score zero on QA, but God no go shame me.

Some defaulters even lie that they’ve paid and there must be something wrong with our app. Mad people.

All this stress and they’re still changing the rules. The most recent one was them introducing some kind of tier system for bonuses. Basically, even if you meet your 180 calls per day and score above 90% in QA, if you didn’t recover up to 70% of the top performer’s recovery in the team, your other two metrics have gone to waste. It’s things like these that cause unhealthy competition and working conditions.

We wouldn’t go for breaks just because we were trying to meet targets. Some people didn’t even have time to eat; they’d bring food to work and take it back home. Even me that likes to talk, my mouth was paining me.

I no longer give a fuck about the job. Imagine doing backbreaking work nine hours a day, for ₦110k a month with bonus wey no even sure. You recover millions for a company, but your money or career isn’t increasing or improving.

I’d hoped I’d grow in the role and, in two years, become a team lead or get into project management or digital marketing or something. But I’m stuck in the same role, and there’s not much room to grow, so I have to start looking out for myself.

These days, I’m just doing enough to not lose my job. I won’t do more than I’m paid for because fintech won’t kill me for my mother. All the OGs are already leaving the company. I’m just biding my time while I figure out my next move.

FRIDAY

I’m always grateful for Fridays because I’m a social butterfly. Work may weigh me down, but when I turn up? I turn up. As I turn on my laptop, all I’m looking forward to is close of work so I can go to SOUTH and unwind. I’m tired. All my body needs right now is their Long Island. The thought of it is the only thing that’ll get me through the day.

While I’m having lunch and taking a break from those annoying loan defaulters, I think about trying new things and keeping at them. In the recent past, I’ve tried project management. I finished the course, but I got bored when it was time to apply my knowledge. I’ve also tried data analysis, SQL and digital marketing, and now, I’m about to complete a course in virtual assistance. Maybe my experience in customer relations and communication would help me thrive in that role.

I often think I don’t have the grit to succeed, but maybe I’m just scared of starting over in an entry-level role. I don’t know again abeg. Too much thinking and too little time. I finish eating and get back to work.

My weekend afternoons are for the virtual assistant course I’m taking. Evenings are for “we outside”. When next Monday comes, I’ll face it bravely.

Check back for new A Week in the Life stories every first Tuesday of the month at 9 a.m. If you’d like to be featured on the series, or you know anyone interesting who fits the profile, fill out this form.

The topic of how young Nigerians navigate romantic relationships with their earnings is a minefield of hot takes. In ourLove Currency series, we get into what relationships across income brackets look like in different Nigerian cities.

For this interview, I’m speaking with Okoye*, a 29-year-old freelance writer based in Lagos. He tells me how he recovered from a gambling addiction with the help of his lover in 2021, and also how he’s managing his now two-year-old relationship with a single mother, on a ₦300k salary.

*subject’s name has been changed to protect his identity.

Total monthly income

It fluctuates. But ₦300k on average.

Occupation

Freelance writer — with a focus on finance (crypto, especially) and sports.

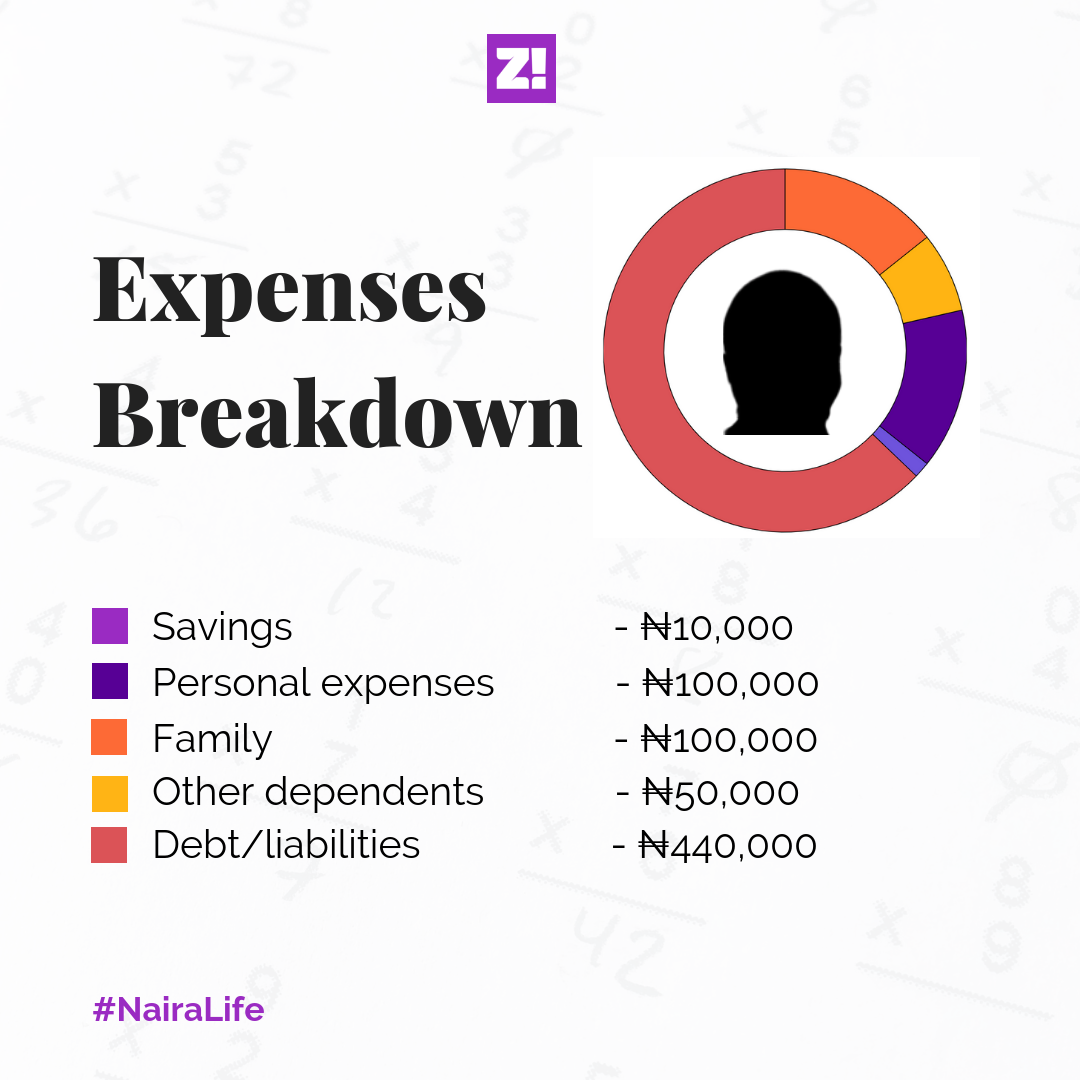

Bills and recurring expenses

I don’t pay rent because I still live with my parents. My dad, sister and mum contribute to it. Meanwhile, I’m saving up to get my family out of the trenches.

Food: ₦50k because we buy foodstuff in bulk most of the time.

Data: ₦20 – 25k.

Savings for relocating family: ₦80k in the last two months.

Black Tax: Upkeep for my parents and sisters rounds out at about ₦30k.

Miscellaneous: I pay for courses occasionally, and those take around ₦20k.

Netflix: Around ₦4k monthly.

How long have you been in a relationship?

Two years and two months.

How much does your partner earn?

She’s an online thrift vendor, so her income isn’t steady. But she makes an average of ₦80k weekly, which amounts to roughly ₦320k monthly. On some good months, she makes up to ₦400k.

How did y’all start dating?

Around February 2020, I saw her comment on a mutual friend’s post and playfully replied that I liked her but was holding myself back from sliding into her DMs. She responded, “Dey there na.”

So I quickly DMed her. But our initial conversations were stilted. She was mostly unavailable, and I struggled to reach her. She’d just left her ex and was learning to raise her two-year-old son on her own.

But in March, when the lockdown started, she had more time on her hands, so we started talking more often. By April 8, 2020, I chyked her, and she agreed.

How much were you earning then?

I was barely making ₦100k consistently, but we were on lockdown, so the pressure wasn’t much. We were OK with just calls; no need to travel (she doesn’t live in Lagos). We dated virtually until December 2020, when she visited Lagos for an event, and I booked a hotel (I live with my parents).

That was the first time we met.

With such limited income, what gave you the mind to toast a single mother?

I believe I’m an interesting person, and I’m relentless about doing better for myself. So even then, I knew it was just a matter of time, I would eventually earn more money. Also, I’d dated women higher on the social ladder before, and it didn’t freak me out.

Secondly, I really liked her personality. Once I like somebody, and I feel we might vibe well after watching them for a bit, omo, na to shoot shot o. What’s the worst that could happen?

A focused king! Okay, how did it go from there?

Funny, after December 2020, it took another seven months for us to see again, but under unpalatable circumstances. I’d been battling a gambling addiction and was in debt and I’d hidden it from everyone.

But one day, I lost a bet after borrowing money. When the creditors came to look for me, I got overwhelmed, so I left home, booked a hotel, shut my phone off and went to bed. My partner panicked when she couldn’t reach me. When I switched my phone back on the next day, I saw her barrage of messages. So I opened up to her.

I still don’t know how our relationship survived that.

Gist me

I panicked and told her I wanted to break up — I couldn’t continue with the relationship because I thought I had too much baggage. I was over ₦350k in debt from gambling — ₦150k credit from the betting house and ₦200k from loan apps. I thought no one would want to deal with my mess. But she got pissed that I was saying “nonsense”.

Tell me more

Omo. She said it was unfair that I wouldn’t even give her a chance to decide on her own. She did say we should take a break, but she wasn’t going to leave me hanging. She would keep tabs on me to make sure I was okay.

After two weeks, she asked for my account details and passwords so she could track my expenses, and then, she helped me work on a repayment plan. She also suggested I leave my environment — the betting centre was close by — and go stay with her for a while.

I was humbled by her faith in me, so I resolved to get myself out of the mess. I went to visit her and stayed there for a month. I wasn’t her favourite person during that period, but she was very supportive. But I bonded with her toddler so well, he didn’t want me to leave, and that helped.

The change of environment did wonders. I applied for and got ghostwriting gigs that brought in the much-needed cash. My partner had my account details, so she monitored my expenses and ensured I didn’t relapse. I didn’t want to disappoint her again, which helped me stay focused on dealing with the addiction. After that month, I went to live with my aunty. Gradually, I paid off my debts.

It was hard to win her trust again, but by November, our situation improved.

What happened next?

We began to plan for a vacation in December (2021). She visited Lagos, and we toured the city for a few days. I visited her soon after, and we had a staycation. Those were the best two weeks of our relationship.

How much do you budget for relationship sturvs these days?

It’s as the spirit leads. For example, the last time I visited her, sales were poor that week, so I helped her stock up on groceries and provisions before I left. When she wanted a second phone to use as her business line, I gave her ₦40k — a third of the total cost. It’s the little I could do.

When I need help, she comes through as well. We buy each other gifts: ₦15 – ₦20k here, ₦40k there, depending on our finances. She gives me more physical gifts — clothes, slides, etc., while I give cash and the occasional gift.

How much do you spend on vacations?

We make calculations and split costs. We spent around ₦120k over four days on our last vacation in Lagos and split 60/40 — 60% for me, 40% for her. Our hotel room cost ₦12k per night; beach waka took like ₦25k, including cab fares. We spent the rest on bar hopping around Surulere. Food cost us around ₦25k.

Since we don’t live in the same state, we spend the most on each other when we meet. In May 2022, I carried my brokeass to her house. She practically fed me for the first two weeks of my one-month stay and sorted all the bills because I wasn’t getting writing gigs for a hot minute.

But things picked up for me, and I took over payments for the rest of my stay.

What kind of conversations do you have with your woman about money?

We’ve decided to be lovers for the long haul, so we discuss long-term plans. We want to expand her business. I’ve suggested getting a physical location and diversifying what she sells. Her thrift business fluctuates, and I’d like her to be more stable. We’re currently making progress with that.

One of the things we agreed on was to start ajo — ₦100k monthly savings. This month, she’ll pack ₦1.2m and launch the new business line.

I wasn’t business-minded before, but I’ve started to make small investments. My goal is to make an average of ₦800k – ₦1m by next year at least. I’m also learning about the stock market to improve my portfolio and build wealth, and taking courses in comprehensive digital marketing, covering Facebook ads, Google ads, etc. With this new knowledge, I’ll run better ads and boost sales for my woman. I plan to learn about drop shipping once I’m done.

Do you have a financial safety net?

At the moment, no. I’ve spent so much in the last couple of years, I’m practically resetting my life. I don’t like the place I currently live with my family, so I’m hustling to get us out of here soonest.

My saving grace is, worst-case scenario, there are people who see me as credit-worthy. But I’m trying to double my hustle, so I can run family expenses and build a safety net while at it.

What’s the ideal financial future you want for yourself and your partner?

I want investments in real estate and stable sources of income that would see us making a collective income of at least $4,000 monthly. I’d also like an impressive stock portfolio of low-risk investments to assure our kids of a better quality of life than I’ve had.

Lending people money can be very risky. You have to be ready to fight or say bye-bye to your money for the sake of peace.

If you’ve already made the terrible mistake of giving out your hard-earned money, then you can never be too prepared for the process of getting it back. We put together this guide on how different people behave when it’s time to repay a debt, just for you.

The ones who pay back on time

These ones don’t like trouble. With them, you’re sure to get your money back five business days in advance. Yes, they exist.

The ones who come back to borrow a few days after repaying

Can you actually say they didn’t pay back? No. But you see, you’re like their rolling fund. They pay you just so they can collect it back.

The ones who ghost you

Once you lend these people money, don’t expect to hear from them again. They’ll ghost you harder than your ex.

The excuse-givers

Just days before it’s time to pay back, they’ll have issues with their bank that can only be sorted out when God interferes.

They genuinely can’t believe you have the audacity to ask them for your money. It’s such a cardinal sin to these folks. Just don’t let them catch you in the streets. You’ll explain you got the nerve to ask them for your money.

The ones you run into at the club after they say they have no money

They’ll swear they just came to drop somebody off even though you can clearly see the bottle of Azul on the table.

The ones who start acting very nice, hoping you’ll forget

These are the ones who’ll check up on you three times a day as if they’re your parent. They just want you to feel bad about asking for your money. Don’t fall for it!

The ones who act like they don’t know what’s going on

They smile at you and tell you the new hot gist about the fancy new bag they just bought. But you’re dying inside, trying to hold back tears.

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

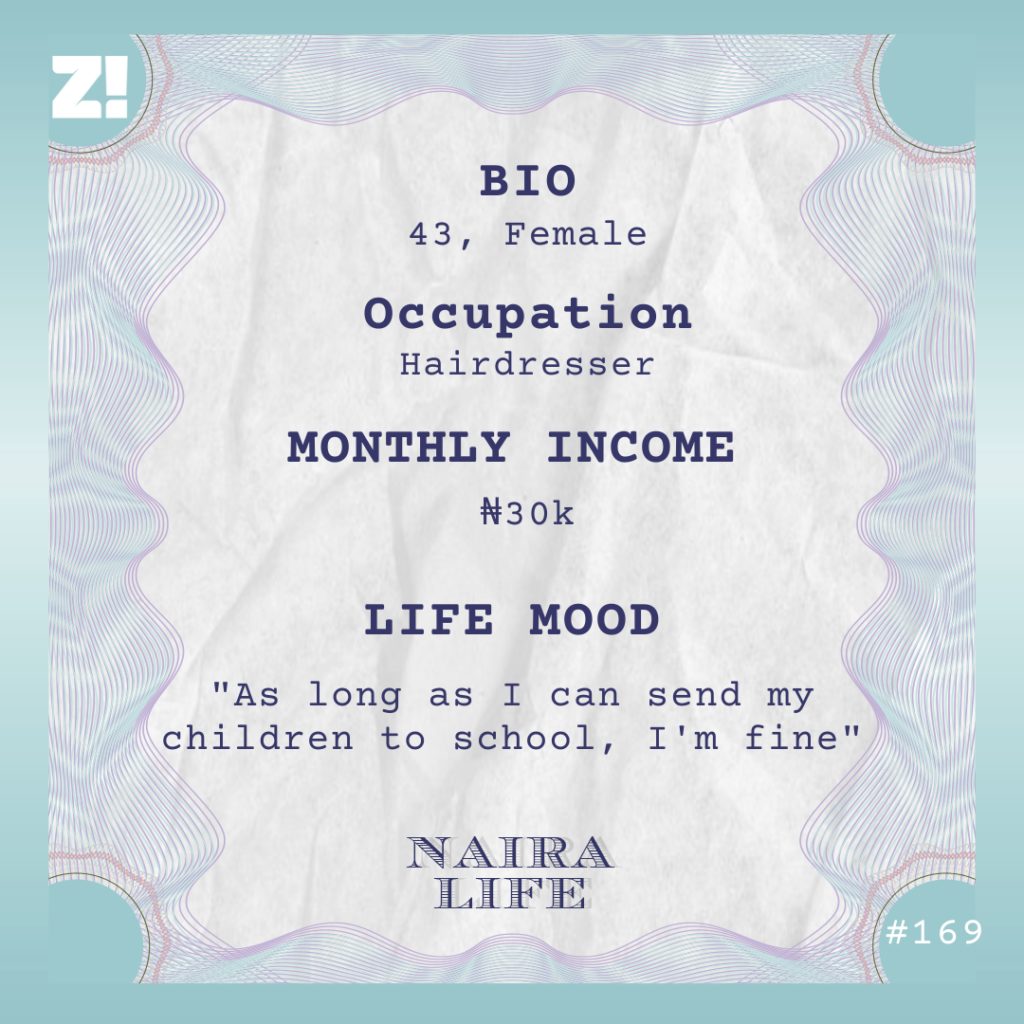

Between 1996 and 2014, today’s subject on #NairaLife worked as an auxiliary nurse. Her highest salary in that period was ₦12k. Today, she works as a hairdresser and lives on loans she repays every week.

What’s your earliest memory of money?

1995. I was 16 and decided to turn my hairdressing talent into money. My parents separated when I was two and my younger brother was 11 months. We first lived with my mum because we were kids, but my dad took us back after a few years. I only had the chance to visit my mum during the holidays after that, and it was during those visits I found out I was a natural at hairdressing. My mum had a neighbour who made hair. I used to stay at her shop watching her. Then one day, I tried to braid a friend’s hair and did a fantastic job.

By the time I turned 16, I decided to stop making people’s hair for free. I bought a poster and put it outside my mum’s palm wine shop. At that time, I charged as high as ₦100 to make people’s hair.

Sweet.

Because hairdressing brought money, I switched from going to my mum’s place only on holidays to going every weekend. My dad dropped me off on Fridays and picked me on Sundays, and by Sunday, I’d have made ₦1,000. Sometimes, my dad “borrowed” the money. Other times, I saved.

By 1996, I was in SS2, and I decided to stop and train to become an auxiliary nurse instead.

Why?

I’d loved the idea of being a nurse since I was a child. Seeing people in nurses’ uniforms brought me joy that I couldn’t explain.

How did you become an auxiliary nurse in secondary school?

I had a classmate who was also training to become an auxiliary nurse. She took me to a hospital that had a vacancy, and they took me in. I can’t remember how much, but to learn, I had to pay the hospital. My dad paid for me. On weekdays, I went to work after school, but on weekends, I worked full shifts. My job was to assist nurses, so I treated wounds, gave injections, etc.

11 months into my training, when I was in SS 3, I got pregnant, so I decided to stop. I also dropped out of school. I moved to live with my mum so she could take care of me during the pregnancy period, and I decided I still needed money to take care of my child, so I used the little money I’d saved to buy raw rice, beans and garri to resell. I made a profit and restocked multiple times, and that’s what I sold until I had my child in 1997. When the child was six months old, I decided to go back to auxiliary nursing. This time, at a different hospital.

Why?

I wanted to start afresh somewhere I could learn comprehensively. The auxiliary nurse training is a three-year programme, and I’d only done 11 months at the first place. Starting afresh was an opportunity to refresh my memory of what I’d learned before. I started in 1998 and graduated in 2001. During that period, I survived only on pocket money from my mum and hawking medicine.

Hawking medicine?

By 2000, one of the doctors at our hospital asked me to work at his pharmacy from time to time. Being there made me realise people were always buying medicines, so I gathered all the money I could find — ₦8k — and bought medicines to start hawking. Because I didn’t have a license, I only sold painkillers and common vitamins, but the market moved well.

What happened after you graduated?

The hospital hired me. My first salary was ₦8,000. Every month, I invested a bulk of the money into my business. So whenever I was off work, I was on the streets selling medicines. As time went on, my business grew, but I had to stop hawking in 2002 because I was pregnant. This time, with a different man — my husband.

When did you get married?

That same year.

Where was your first child in all of this?

Mainly with my mum. I was always at work, so, she just helped me take care of the child. By the time I got married and moved in with my husband, the child didn’t come with me because she preferred being with my mum, so I left her there.

A few months after I gave birth, I started hawking again to complement my salary, which was now about ₦10k. My husband was an okada rider and didn’t make too much money too, so I had to keep making as much money as I could to keep the family fed.

By 2008, I left my job for another hospital. This one paid ₦12k. We pretty much lived hand to mouth with nothing to spare until 2013 when my husband passed away.

I’m so sorry.

Apparently, he was poisoned. Oh, by the way, my mum had died somewhere along the line too, and my daughter was now living with me, so I was a widow with two children to care for. It was difficult to do with my ₦12k salary. At some point shortly after he died, our rent expired, and I couldn’t afford it, so my two children and I had to move to stay in our church.

How long did you stay there?

Two years. So I went to work in the morning, hawked medicine in my free time, and then, started making people’s hair in front of the church building. That’s how we survived those years. I still managed to put my children to school through that period. When they weren’t in school, they were in the church waiting for me to get back.

By 2015, I met a new man who I was sure I wanted to settle with, and we got pregnant. We decided to move in together, but housing in the area where I stayed was too expensive. We couldn’t find anything cheaper than ₦160k per year, so we moved to a different area where we found a place for ₦70k. Because of that move, I quit my job.

When did you have the baby?

That same 2015. First, we survived on the money from selling the rest of the medicine I had. When that was done, I started making hair again. This time, with more energy. I put posters all around our house, bought a stool, combs, hair creams, everything. The money I was making still wasn’t enough, so I took a ₦50k loan from a loan company when I was about to have the baby. That’s the money we used to buy baby stuff.

What does your husband do?

He runs a Baba Ijebu gambling shop. I try my best not to be the complaining wife, so I won’t push him to do illegal things for money, but he doesn’t bring anything to the table. He makes about ₦600 daily. He uses the money to eat. That’s all. It’s not like he’s not trying or he doesn’t care for the family, but I think he can do better. He gives me money only about two times a month. And when I say, “gives me money”, I mean ₦200 or ₦300.

Whoa. Let’s go back to 2015.

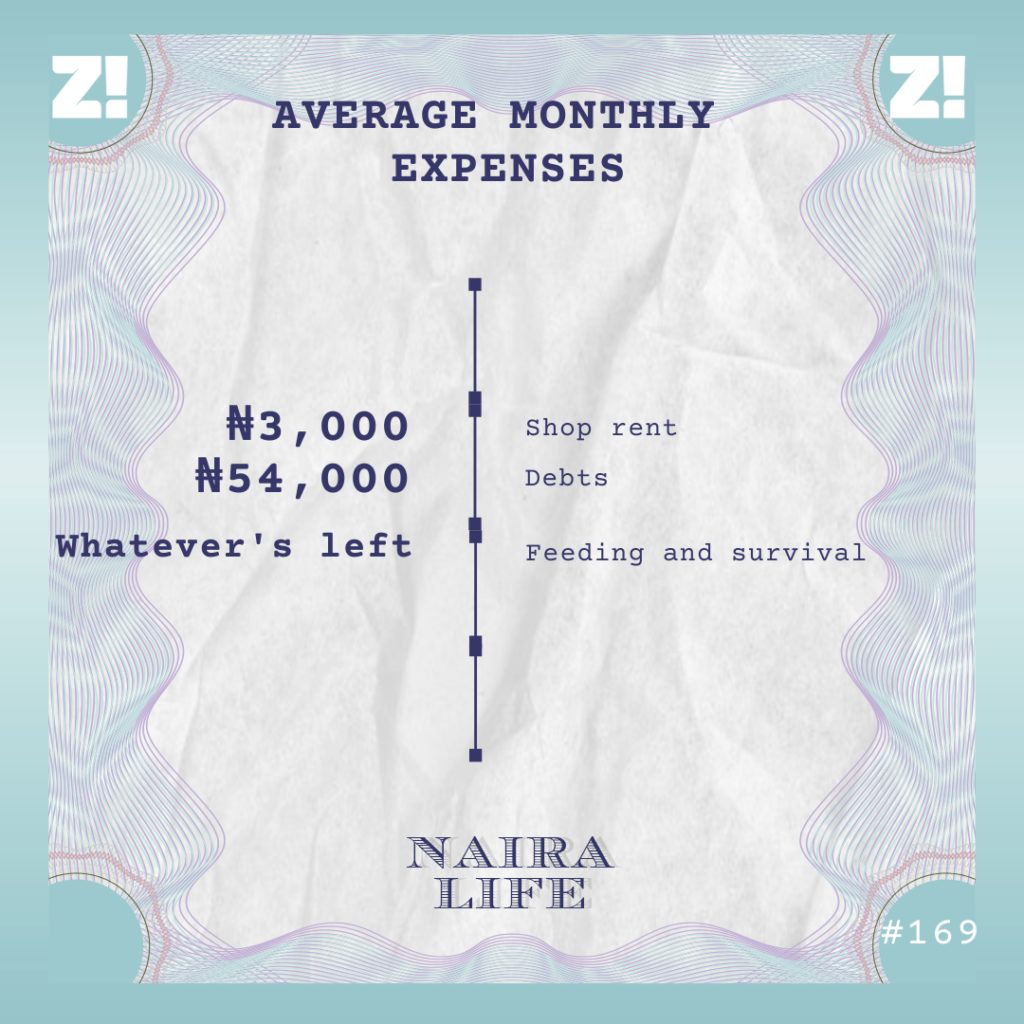

Between 2015 and now, my hairdressing business has grown very slowly. There are a lot of hairdressers in this area, and people pay much lower fees than they paid in the other area. I’ve had to supplement my hairdressing income by selling stuff. At some point, I’ve sold puff puff, but now, I sell bags of pure water and drinks. I even bought a container for ₦30k to use as a shop one time. But after some months, the owner of the land came and chased me away because they wanted to build their house, so I sold the container for ₦35k. I eventually found a shop where I pay ₦3k monthly as rent.

How much do you make on an average month?

₦30k. This is from hairdressing, and water and drinks selling.

Can you break it down into expenses?

I’ll try. Here’s what it looks like right now.

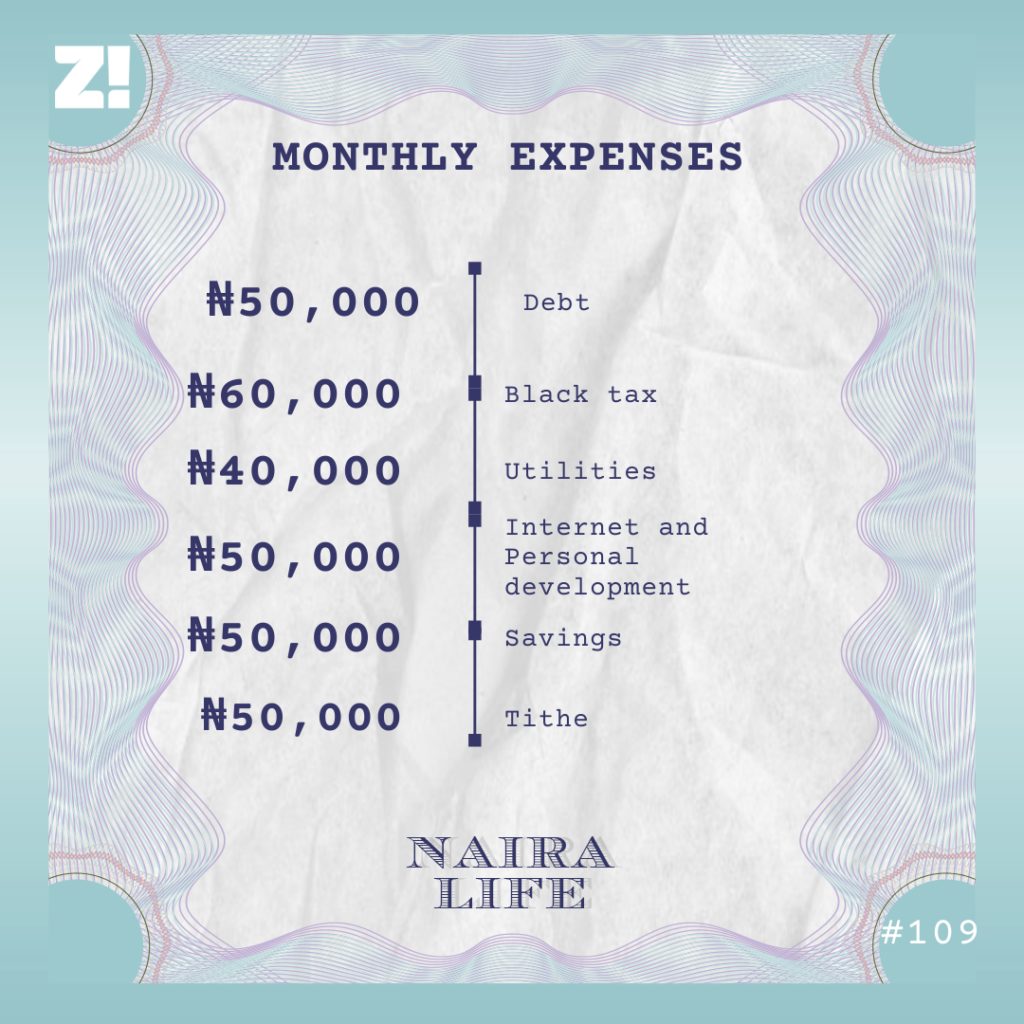

₦54k for debts?

I haven’t been able to survive on just my income for years, so I take a lot of loans. When I finish repaying, I take another loan. Between 2021 and now, my first two children have gone to polytechnic. I pay their fees and send them occasional stipends.

Right now, I’m repaying loans from two different loan companies. From one, I collected ₦100k and pay back ₦5,500 every week. From another, I collected ₦150k and pay back ₦8,000 every week.

What happens when you can’t pay back?

I borrow from people who have their shops beside me. We’re friends, so they can lend me the occasional ₦2k.

Do you have any plans to get out of this situation?

If I can repay my loans and make some bulk money to stock my shop with lots and lots of drinks, I believe I’ll be on a path to becoming comfortable. I don’t want to have to borrow to restock my shop. It’ll continue the cycle. In fact, the reason I borrow most of the time is to restock my shop, but I never get to it because other things come up and take the money. Right now, there are only two bags of pure water and 2 crates of drinks in my shop. It’s how I’ll repay my loans and get that bulk money I don’t know.

What’s something you want right now, but can’t afford?

Stocking up my shop.

And your financial happiness on a scale of 1-10?

Two. It’s bad, but I’m thankful to God for the little things I can do, like sending my children to school.

Do you remember the first time you had to borrow money? We’re not talking about urgent ₦2k o. Adulthood has a way of putting you in those tight corners that require hundreds of thousands. Borrowing money is the ghetto, and these 5 millennials share the first time adulthood had them on the streets asking for help.

1. Chike, 25

A tanked business

I was 21 when a friend and I started a business for people to invest in buying plots of farmlands in Ogun state for an interest rate at the end of the year. Six months in and I had people bringing in millions of naira to buy into the plan. It was a pretty sweet deal back in 2017. My clients cashed out on all their investments, so 2018 was even bigger for us. I even had aunties and uncles putting in money for me to grow the business. I had about ₦15 million in capital by the second quarter and I was sure I’d be making nothing less than ₦2 million by the end of the year as profit. That ₦2 million became a dream when my partner made a horrible decision that made us lose all the money. That’s how I found myself in debt for ₦15 million naira at 21. We both had to come up with half of it by December to pay people back and it was the worst experience of my life struggling through it.

2. Stephanie, 28

Hospital Bills

The first time I had to borrow a huge amount of money was in 2018 — I was 25. My parents had travelled to the US for a wedding and decided to stay back and work towards becoming citizens from the backend of things. Since the move wasn’t entirely legal, they couldn’t send money back to us in Nigeria immediately. So I had the responsibility of taking care of myself, my two brothers and my cousin. To survive, I sold everything, from shoes to electronic doors for banks to spaghetti and turkey on Saturdays, but I couldn’t save any of the money I was earning. A year later, my cousin got pregnant and had complications that required surgery. Everything cost ₦150k and I couldn’t afford that. The doctors weren’t going to operate until I made a transfer, so I had to borrow the money from Etisalat 9-credit. That was the first time I was really pressed into a corner to borrow money as an adult.

3. Sandra, 29

Abacha

It was 2020 and Valentine’s day — I didn’t expect the gbas gbos that happened that day. I went to visit my boyfriend and decided to buy a plate of Abacha from a woman across the street. The Abacha was so good, I went back for a second plate. I slept off after the second plate and woke up vomiting and stooling until my body was too weak and I passed out. I only remember waking up two days later with a bill of ₦400k for just treating food poisoning. I don’t know who sent my boyfriend to take me to a private hospital. We didn’t even have up to ₦20k to cover the bill, so I had to call some of my friends to help me. People sent me as little as they could afford at the time to meet up so I was able to sort it out. I believe that Abacha woman was a witch sha.

4. Sere, 26

Knacks and Love

I was 20, and the first time I had to borrow money was for knacks. My boyfriend asked me to take out ₦30k from a loan app to get a hotel room for us. He promised to pay back, so I didn’t mind — the knacks were too good to be bothered at the time. The next time, he asked me to lend him ₦300k to start a business while we were still in school. I loved him, so I didn’t really overthink helping him by asking around for the money. Three months later, there was no business in sight and people were on my neck to pay back. I had to beg for help to pay people back. It was so embarrassing to go through that. Never again.

5. Timmy, 31

My first apartment that never happened

I was 29 and tired of living with my friend, so I saved up ₦450k to move out after the pandemic. When I hit the streets to search for a house, the fees for agency and agreement wanted to kill me. I had to beg a friend to loan me ₦300k to cover the rest of the bill. I finally found a place, but before I paid, my friend invited me for a wedding in the US and advised me to use it as a japa plan. That’s how I used the ₦750k to get a travel agent and process my visa — everything was about ₦500k. Then I used the remaining ₦250k to buy my ticket in faith. Last last, nothing worked for me and I was denied the visa. I spent the rest of the year trying to re-sell the ticket so I could pay my guy back, but nobody was willing to buy. I ended up getting so broke, I had to move back in with my friend.

Running a country, like most things in life, requires a budget. On Thursday, October 7, 2021, the country got a presentation from Buhari on what it would cost to keep Nigeria ‘working’ in 2022.

The presentation was tagged a “Budget of Economic Growth and Sustainability.” According to the president, this budget is meant to diversify Nigeria’s economy, develop infrastructure, improve security and do so many other great things you’ve probably heard before.

But something you’ve definitely not heard is the content of this particular budget. In 2022, Nigeria plans to spend ₦16.3 trillion naira, even though it plans to make only ₦10.1 trillion.

To achieve this already suspect plan, the government will have to borrow about ₦5 trillion. Nigeria currently has a public debt of over ₦33.1 trillion.

There are so many other things in the 2022 budget, but all we’re thinking of now is how much each of us will have to pay when our debtors come to collect.

Budget breakdown

A budget usually contains how much you make and how much you plan to spend. In Nigeria’s budget, our earnings are classified as “revenue” while our spendings is called”expenditure”. The difference between how much we make and how much we earn is the “budget deficit”.

The government wants to make ₦1.8 trillion from other taxes. Dividends from the Bank of Industry (BOI) should come from ₦195 billion and ₦300 billion should come from special funds.

The government also wants to earn ₦63 billion from foreign aid and ₦710 billion will come from other sources.

Expenditure –

In 2022, Nigeria wants to spend ₦16.3 trillion. ₦6.8 trillion will be to pay for expenses like salaries while ₦4.8 trillion will be to build roads and other infrastructure. Nigeria will use ₦3.9 trillion to pay back debts while ₦768.2 billion will be used to pay for some very important things like pensions.

Deficit –

Nigeria needs ₦6.2 trillion to complete its budget. The government will borrow ₦5 trillion. ₦1.1 trillion will come from loans tied to projects and ₦90 billion will come from the sale of some assets.

Remember, this is a budget, and it is only a plan. Nigeria may not make or spend up to the amount in this budget. But anything you see, just try to take it like that.

A recent cause for this stress is the news that President Muhammadu Buhari has asked the National Assembly to approve his plan to borrow over $4 billion and €710 million from international organisations to finance projects in the 2021 budget.

The President also asked the National Assembly to allow him to seek $125 million in grants for special projects.

Buhari practically said:

The new loan request is coming just four months after the President requested that the National Assembly approve his plan to borrow over $8.3 billion and €490 million from various international organizations. This request was approved.

In March 2021, the National Assembly also approved the President’s plan to borrow $22.7 billion for “infrastructure development”.

But Exactly How Much Is Nigeria Owing?

You may want to sit down for this next part. As of March 31, 2021, Nigeria’s total public debt stood at over $87.2 billion which is about ₦33.1 trillion.

Of that debt, $43.5 billion is to be paid by the federal government while the state governments and the Federal Capital Territory owe $10.8 billion.

At the time, Nigeria also owed a total of $32.8 billion or ₦12.4 trillion foreign debts while we owed $54.3 billion or ₦20.6 trillion domestic debts.

Be honest, this is what you thought when you saw what “we” owed:

These numbers are just from March and they don’t include the recent May and September loan requests by the Federal Government or any of the new loan plans by the 36 state governments. The foreign exchange rate was also different at the time of calculation.

Who Is Nigeria Owing?

As of March 31, 2021, these are the people Nigeria owes abroad:

International Monetary Fund – $3.44 billion

International Development Association – $11.09 billion

International Bank for Reconstruction and Development – $410 million

African Development Bank – $1.59 billion

African Growing Together Fund – $210,000

African Development Fund – $942 million

Arab Bank for Economic Development in Africa – $5.88 million

European Development Fund – $51.3 million

Islamic Development Fund – $29.7 million

International Fund for Agricultural Development – $223 million

Exim Bank of China – $3.4 billion

Agence Française Development – $486 million

Japan International Cooperation Agency – $74.6 million

Exim Bank of India – $34.5 million

Kreditanstalt Fur Wiederaufbau – $183.7 million

Eurobonds – $10.3 billion

Diaspora Fund – $300 million

Promissory notes – $179.5 million

Nigeria owes a total foreign debt of $32.8 billion as of March 31, 2021.

Nigeria Can Pay This Money Back, Right??

Borrowing money is not a bad idea if you can pay it back. But Nigeria is currently swimming in so much debt, and it is not making enough money to justify taking on more debts.

This year alone, Nigeria will be paying back₦3.12 trillion in debts. On top of that, Nigeria plans to borrow another ₦5.6 trillion.

These debts are unsustainable because the government wants to spend ₦13.5 trillion yet Nigeria plans to make only ₦7.99 trillion, and we have not made more money since the ₦10 trillion we made in 2014.

South Africa, for instance, wants to spendR2 trillion in 2021, but the country makes R1.36 and will be borrowing R689 trillion. South Africa will also be paying back debts of R232 billion, but it has a very good tax system that can help it to generate revenues easily.

Economists say that Nigeria’s “debt to GDP ratio” (that is Nigeria’s total debt compared to Nigeria’s total productivity) currently stands at about 32% and apparently, that is still low and in line with the World Bank’s recommendations.

But economists also agree that Nigeria’s “debt to revenue ratio” (that is Nigeria’s total debt compared to how much Nigeria actually makes) is becoming a concern.

Nigeria must reduce its debts and start making more money if it does not want to be caught in a debt trap.

Nigeria is tough and the people who refuse to pay up their debt don’t make living here any easier. If you’ve been aired or blocked by someone you lent money to, here’s a guide on how you can legally get your money back.

The first thing you need to know is that if anyone in Nigeria owes you a debt, you have to act fast. If you try to get the money through a law court after six years, the court won’t answer you — and that’s according toSection 21(1) (a) of the Statute of Limitation Law.

Also, when trying to get back your debt, avoid sending any threatening or intimidating messages to your debtor. While we know that being owed can get you very angry, you also don’t want those threats of violence to backfire into a criminal case against you. So please, no violence.

And most importantly, do not involve the police in a debt recovery case in Nigeria as the police are meant to fight criminal issues, not issues between normal people. Involving a lawyer from the start is a better option.

Now, TimeToGet Your Money Back

Do you have an agreement in writing with the person you lent money to about the steps you can take to recover your debt if they don’t pay up, like selling a property? If yes, then good for you. You can simply follow the steps in that agreement to recover your debt.

If you don’t, that is still alright. There’s no need to escalate things. You can try sending them a message reminding them of their debt. Sometimes that’s all you need to do.

But if all else fails, here’s how you can “gently” get your money back:

Send The Person A Letter of Reminder:

You can send your debtor a “letter of reminder”. This letter should be written by your lawyer, and it should remind the person owing you that you will take the case to court if they fail to pay up your money.

Try Mediation and Arbitration:

To get back your money, you can involve third parties — if the other party is willing to discuss it with you, of course. In mediation, a third party can help you and your debtor reach an amicable settlement.

In arbitration, you and the other person must follow the final agreement reached by the arbitrator, and the decision can be enforced in court because it is legal. But there must have been an agreement that you and your debtor will use arbitration to settle matters in the original loan agreement.

Write The Person A “Letter of Demand”:

If you are getting uneasy and your debtor is still unwilling to pay up, then you can employ the services of a lawyer to draw up a “letter of demand”, warning the person of the things that will happen if they do not pay back your debt within a period.

The letter of demand usually confirms the exact money you are owed, a clear time when the debt should be paid back and the legal consequences of failure to pay back the debt.

A letter of demand usually serves as a good notice to the debtor before you take matters to court.

Try Taking Legal Action –

Finally, in the case where the debtor has failed to pay up even if you have sent them letters and tried to be reasonable with them, then you should take the matter to court.

The court will enforce a decision for your debtor to pay you back your money, after hearing the facts of the case.